Periods of unemployment can cause uncertainty of how you will pay your bills and how many months it might take to find another job. You may be looking for resources to keep you afloat. Family and friends may not be in a position to help, and your savings may not tide you over for long.

You’ve probably heard about personal loans, but can you get one when you’re not currently working?

Can You Get a Personal Loan While Unemployed?

Yes, you can get a personal loan when unemployed, but it’s going to be harder than if you had a steady job. To qualify for a personal loan, lenders look at three main things — your credit score, your income, and your debt-to-income ratio. If you have no income and your debt-to-income ratio is high, you’ll have a hard time getting approved.

However, if you have alternative sources of income, such as Social Security, alimony payments, or retirement, you may be able to qualify for a personal loan while unemployed.

(Learn more: Personal Loan Calculator)

Personal Loan Basics: What Are Personal Loans?

Personal loans are lump sums of money given to a borrower from a lender. They can be used to make a big purchase, consolidate high-interest debts, or help pay the bills during times of uncertainty. Personal loan interest rates are often lower than those on credit cards, and the interest rates are typically fixed.

Personal loans are often unsecured, meaning you don’t have to put up collateral to guarantee the loan. Some lenders offer secured personal loans, as well, which do require collateral. Not needing to provide collateral may be appealing, but secured loans may have more favorable interest rates than their unsecured counterparts. They also may help you land a loan if you’re currently unemployed.

Payments are typically made monthly, with terms ranging from one to seven years. Loan amounts can vary from $1,000 up to $100,000.

Can You Apply for a Personal Loan While Unemployed?

Yes, you can apply for a personal loan while unemployed. Unemployment isn’t necessarily a deal breaker for personal loan approval. If you have other sources of income, such as alimony, child support, Social Security payments, pensions or annuities, or certain disability payments, for example, you may be able to get a personal loan.

Applying for a personal loan typically begins with getting prequalified. Most lenders do a soft credit pull during this stage, so it may be worth it to apply and see if you’re prequalified. If so, you can move forward with submitting your full application.

Can You Apply for a Personal Loan as a Student?

College students can apply for a personal loan, but lack of a credit history and low (or no) income may present a hurdle to approval. Lenders may see you as a risk because there is not a long record of how you have met your financial obligations in the past.

If you’re a student seeking a personal loan, you may want to consider asking a friend or family member to cosign the loan. If they have a solid credit score and regular income, you’ll have a better chance at getting approved. This is because if you fail to make the monthly payments, the cosigner becomes liable.

Personal Loan Options When Unemployed or as a Student

While you may get a personal loan when you’re unemployed, there could be limitations.

- The lender may require you to have a cosigner.

- You may be approved for less money than you asked for.

- The term of the loan may be shorter, for instance, 24 months instead of 36 months, because a lender may see this as less of a risk.

- You may be approved at a higher interest rate than if you were employed.

How to Qualify for a Personal Loan with No Income

To qualify for a personal loan, lenders are going to look at your credit, your income, and your debt-to-income ratio. Lenders need to know that you are going to pay the loan back and that you have the funds to do so.

If you have good credit, your chances of being approved for a personal loan are higher than if you have poor credit. You’ll also qualify for better rates and terms with good credit.

Your income does not need to come from employment. Instead, you can use Social Security income, retirement income, alimony or child support, rental property income, long-term disability, and more. If you don’t have any income coming in, you may need to get a cosigner or put up collateral to back your loan. If you then fail to make the monthly payments, the lender can seize your collateral.

Your debt-to-income ratio is the amount of debt you have when compared to your income. Lenders prefer this number to be less than 36%. If this number is low, you have a better chance at being approved for the loan.

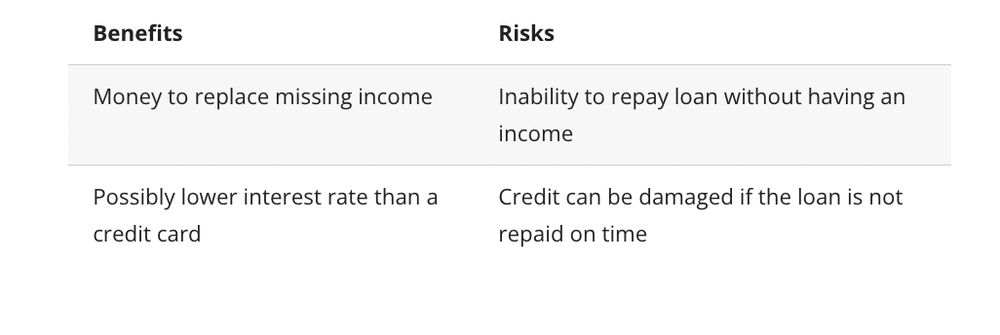

Benefits and Risks of Taking Out a Loan While Unemployed

There are pros and cons of borrowing money when you’re unemployed. Assuming you’re approved for a personal loan while unemployed, it will be nice to have funds available to pay bills. However, the loan will need to be paid back and it’s important you can meet your monthly payment obligation.

Benefits of Taking Out a Loan While Unemployed

There can be several benefits to getting a personal loan when you’re out of work, including:

- You can use the money to pay bills, keep in a savings account for an emergency, or to start your own small business.

- The interest rate on a personal loan may be less than credit cards.

- You can consolidate multiple debts with a personal loan, which can help you save money if you’re approved for a lower interest rate than you’re paying on your credit cards or other bills. It may also simplify your budget by having just one one monthly debt payment instead of several.

Risks of Taking Out a Loan While Unemployed

If you’re considering taking out a personal loan during unemployment, there are some risks, as well, including:

- If you can’t make timely payments or you miss payments altogether, the potential consequences to your credit can be significant.

- If you don’t qualify for a favorable interest rate, a loan may not be helpful in the long run and you might want to consider alternatives.

- You may not qualify without a cosigner.

Benefits and Risks of Personal Loans During Unemployment

What Are Some Alternative Options?

A personal loan is a financial tool that can be useful in some situations. However, if you are struggling to qualify, there are alternative options to consider.

Credit Cards

Using a credit card may be one option to consider. The interest rate on a credit card is likely higher than it would be with a personal loan, but credit cards can be easier to qualify for than personal loans. If you do use a credit card, make sure to come up with a strategy for how you’ll pay it off as quickly as possible.

Personal Line of Credit

A personal line of credit (LOC) may be another option to consider. Personal LOCs work similarly to credit cards, but they can offer lower interest rates. Funds from the LOC can be withdrawn, up to the approved limit, and repaid in monthly payments. Interest accrues on any unpaid balance. LOCs generally have a draw period of a certain number of years, followed by a repayment period, during which no more money can be borrowed. Monthly payments continue until the balance is paid in full.

Home Equity Line of Credit

Another option, similar to a personal LOC, is a home equity line of credit (HELOC) using your home as collateral. Because your home is collateral, interest rates tend to be lower than with other forms of financing. However, this may be the last option some people consider because you risk losing your home if you default on your loan.

Alternative Financial Relief Options for Students

Students who find themselves financially strapped can explore financial aid such as scholarships, grants, work-study programs, student loans, and emergency student aid.

- Student loans can be federal or private, each having their own approval process and pros and cons. It’s important to note that federal student loans offer repayment options and federal benefits that may not be available with private student loans.

- Federal student aid may also include grants and work-study.

- Scholarships and grants are available through community groups, nonprofit organizations, university alumni groups, professional associations, and more. Checking with your school’s financial aid office is a good first step to researching these opportunities that typically do not have to be repaid.

- Emergency student aid can help students pay for housing, food, and other essential needs.

The Takeaway

Funds from a personal loan can be beneficial when you’re unemployed or a student. Understanding the risks and benefits of taking on debt can help you determine whether a personal loan is the best solution for you.

This article originally appeared on SoFi.com and was syndicated by MediaFeed.org.

Lantern By

SoFiSoFi receives compensation in the event you obtain a loan, financial product, or service through the Lantern marketplace. This Lantern website is owned by SoFi Lending Corp., a lender licensed by the Department of Financial Protection and Innovation under the California Financing Law, license number 6054612; NMLS number 1121636. (nmlsconsumeraccess). This site is NOT owned and operated by SoFi Bank. Loans, financial products, and services may not be available in all states.

All rates, fees, and terms are presented without guarantee and are subject to change pursuant to each provider’s discretion. There is no guarantee you will be approved or qualify for the advertised rates, fees, or terms presented. The actual terms you may receive depends on the things like benefits requested, your credit score, usage, history and other factors.

*Check your rate: To check the rates and terms you may qualify for, Lantern and/or its network lenders conducts a soft credit pull that will not affect your credit score. However, if you choose a product and continue your application, the lender(s) you choose will request your full credit report from one or more consumer reporting agencies, which is considered a hard credit pull and may affect your credit.

All loan terms, including interest rate, and Annual Percentage Rate (APR), and monthly payments shown on this website are from lenders and are estimates based upon the limited information you provided and are for information purposes only. Estimated APR includes all applicable fees as required under the Truth in Lending Act. The actual loan terms you receive, including APR, will depend on the lender you select, their underwriting criteria, and your personal financial factors. The loan terms and rates presented are provided by the lenders and not by SoFi Lending Corp. or Lantern. Please review each lender’s Terms and Conditions for additional details.

Many factors affect your credit scores and the interest rates you may receive. SoFi is not a Credit Repair Organization as defined under federal or state law, including the Credit Repair Organizations Act. SoFi does not provide “credit repair” services or advice or assistance regarding “rebuilding” or “improving” your credit record, credit history, or credit rating. For details, see the FTC’s website on credit (consumer.ftc.gov)

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.¹

SoFi’s Insights tool offers users the ability to connect both SoFi accounts and external accounts using Plaid, Inc.’s service. When you use the service to connect an account, you authorize SoFi to obtain account information from any external accounts as set forth in SoFi’s Terms of Use. SoFi assumes no responsibility for the timeliness, accuracy, deletion, non-delivery or failure to store any user data, loss of user data, communications, or personalization settings. You shall confirm the accuracy of Plaid data through sources independent of SoFi. The credit score provided to you is a VantageScore® based on TransUnion® (the “Processing Agent”) data.

Personal Loan

SoFi Lending Corp. (“SoFi”) operates this Personal Loan product in cooperation with Engine by MoneyLion. If you submit a loan inquiry, SoFi will deliver your information to Engine by MoneyLion, and Engine by MoneyLion will deliver to its network of lenders/partners to review to determine if you are eligible for pre-qualified or pre-approved offers. The lenders/partners receiving your information will also obtain your credit information from a credit reporting agency. If you meet one or more lender’s and/or partner’s conditions for eligibility, pre-qualified and pre-approved offers from one or more lenders/partners will be presented to you here on the Lantern website. More information about Engine by MoneyLion, the process, and its lenders/partners is described on the loan inquiry form you will reach by visiting our Personal Loans page as well as our Student Loan Refinance page. Click to learn more about Engine’s Licenses and Disclosures, Terms of Service, and Privacy Policy.Personal loan offers provided to customers on Lantern do not exceed 35.99% APR. An example of total amount paid on a personal loan of $10,000 for a term of 36 months at a rate of 10% would be equivalent to $11,616.12 over the 36 month life of the loan.

Student Loan RefinanceSoFi Lending Corp. (“SoFi”) operates this Student Loan Refinance product in cooperation with Engine by MoneyLion. If you submit a loan inquiry, SoFi will deliver your information to Engine by MoneyLion, and Engine by MoneyLion will deliver to its network of lenders/partners to review to determine if you are eligible for pre-qualified or pre-approved offers. The lenders receiving your information will also obtain your credit information from a credit reporting agency. If you meet one or more lender’s and/or partner’s conditions for eligibility, pre-qualified and pre-approved offers from one or more lenders/partners will be presented to you here on the Lantern website. More information about Engine by MoneyLion, the process, and its lenders/partners is described on the loan inquiry form you will reach by visiting our Personal Loans page as well as our Student Loan Refinance page. Click to learn more about Engine’s Licenses and Disclosures, Terms of Service, and Privacy Policy.

NOTICE: The debt ceiling legislation passed on June 2, 2023, codifies into law that federal student loan borrowers will be reentering repayment. The US Department of Education or your student loan servicer, or lender if you have FFEL loans, will notify you directly when your payments will resume For more information, please go to https://docs.house.gov/billsthisweek/20230529/BILLS-118hrPIH-fiscalresponsibility.pdf https://studentaid.gov/announcements-events/covid-19

If you are a federal student loan borrower considering refinancing, you should take into account the new income-driven payment plan, SAVE, which replaces REPAYE, seeks to make monthly payments more affordable, and offers forgiveness of balances that were originally $12,000 or lower after 120 payments, among other improvements. Also, please note that once you refinance federal student loans you will no longer be eligible for current or future flexible payment options available to federal loan borrowers, including but not limited to income-based repayment plans, such as SAVE, or extended repayment plans.

Auto Loan RefinanceAutomobile refinancing loan information presented on this Lantern website is from Caribou, AUTOPAY, Engine by MoneyLion, and each of Engine’s partners (along with their affiliated companies). Caribou, AUTOPAY, and Engine by MoneyLion pay SoFi compensation for marketing their products and services on the Lantern site.

Auto loan refinance information presented on this Lantern site is indicative and subject to you fulfilling the lender’s requirements, including but not limited to: credit standards, loan size, vehicle condition, and odometer reading. Loan rates and terms as presented on this Lantern site are subject to change when you reach the lender and may depend on your creditworthiness, consult with the lender for more details. Additional terms and conditions may apply and all terms may vary by your state of residence.

Secured Lending DisclosureTerms, conditions, state restrictions, and minimum loan amounts apply. Before you apply for a secured loan, we encourage you to carefully consider whether this loan type is the right choice for you. If you can’t make your payments on a secured personal loan, you could end up losing the assets you provided for collateral. Not all applicants will qualify for larger loan amounts or most favorable loan terms. Loan approval and actual loan terms depend on the ability to meet underwriting requirements (including, but not limited to, a responsible credit history, sufficient income after monthly expenses, and availability of collateral) that will vary by lender.

BankingSoFi Lending Corp. (“SoFi”) operates this website in cooperation with Engine by MoneyLion presenting promotions for products and services offered by other banks, lenders, and financial institutions. If you select a promotion above, you will be connected to the website of the company offering the product. The promotions presented on this site are from companies that pay SoFi and Engine by MoneyLion compensation for marketing their products and services. This may affect whether a provider is featured on this site and could affect the order of presentation. Lantern and Engine by MoneyLion do not include all providers in the market or all of their available offerings. Click to learn more about Engine’s Licenses and Disclosures, Terms of Service, and Privacy Policy.

More from MediaFeed:

8 holly-jolly, high-paying part-time jobs for extra holiday dough

Whether you’re in college or caring for children or pursuing an unpaid passion, there are many reasons why someone would want some flexibility in their career.

But what does a flexible schedule mean exactly? According to the U.S. Department of Labor, a flexible schedule is one that allows people to work outside traditional 9 to 5 office hours. Aside from that, situations vary depending on the role and employer.

Workers may be able to choose the time they arrive at and depart work, for instance. With certain flexible work policies, employees still have to work a set number of hours per pay period or be available during a daily “core time.” So while the employee may not have to show up at 9am on the dot and leave at exactly 5pm, they may need to at least show up by 11am and stay until after 3pm. However, this type of shortened schedule could work for many people, including parents who are self-employed.

hobo_018/istockphoto

Flexible part-time jobs can be logistical, analytical, creative, or involve a skilled trade. When it comes time to search for flexible-schedule jobs, keep in mind these tips.

- Stay focused. Job applicants who know what they’re looking for and what they can offer an employer can plan a more effective job search. If someone knows they have to have a flexible part-time schedule in order to accept a job, they can save a lot of time and energy by only applying for jobs that offer that. Trying to convince an employer to change their staffing plans is an uphill battle.

- Prepare to hear No. Know that it will take a while to find the right fit, and that rejection is a normal part of any job search. Psychologically preparing yourself can help you persevere until the right job comes along.

- Don’t be a square peg. If a flexible part-time schedule is what matters most, you may need to be flexible yourself in other areas. For example, accept that you may need to compromise on title, salary, or industry. Giving up the highest-paying job for one with a more relaxed schedule can be worth it.

- Go remote. Work-from-home jobs with flexible schedules can often be easier to find than on-site jobs that have flexible schedules. When reviewing online job boards, look for flexible schedule remote jobs.

Poike/istockphoto

It can be difficult to find flexible-schedule part-time jobs because many jobs require being in a certain location at a certain time. For example, a hairstylist has to show up for work when they have appointments scheduled. A restaurant has to know they have enough servers on hand during operating hours. Even a corporate job where some work can be done remotely and independently can require being online during set times so that it’s easy to communicate with coworkers.

izusek/istockphoto

Perhaps someone wants to take on a second job to help them pay down their debt or save for a dream vacation. Whatever the reason, it’s easy to see the appeal of a part-time job with a flexible schedule.

While there are countless part-time jobs on the market that can suit a variety of workers’ desired schedules, these are some of the best flexible schedule jobs for Gen Zers and Millennials. And if you’re in college, don’t miss our list of the best on-campus jobs.

1. Landscaper and Groundskeeper

Average hourly wage: $17.39

Job description: Landscapers and groundskeepers typically set their own schedules and plan which days they’ll tend to a client’s yard, but they don’t have to tell them exactly what hour they’ll show up to do their work.

Requirements: In some areas a license may be required to use pesticides and fertilizers.

Schedule flexibility: 4

Duties:

- Mowing lawns

- Removing weeds

- Planting and maintaining flowers, bushes, and trees

SerhiiKrot/istockphoto

Average hourly wage: $22

Job description: Running a fitness or recreation class can be fun and rewarding work that is often performed on a part-time basis. Many instructors can choose when they host their classes (like when their young child is in school), but they do have to stick to those times.

Requirements: Licensing or background checks may be required.

Schedule flexibility: 4

Duties:

- Plan programming

- Run classes

- Clean up post-class

kazuma seki/istockphoto

Average hourly wage: $37

Job description: Many businesses hire freelance software developers to create computer programs and applications for business or consumer use. Some meetings during business hours may be required.

Requirements: Knowledge of select programming languages.

Schedule flexibility: 4

Duties:

- Write code

- Test code

- Meet with project stakeholders

(Learn more: Home Affordability Calculator)

monkeybusinessimages/istockphoto

Average hourly wage: $34

Job description: Plenty of professionals can’t afford or don’t need a full-time assistant. Instead, they hire virtual assistants who can tackle administrative work for a few hours a week. Virtual assistance can be a rewarding job for introverts who are conscientious and organized.

Requirements: Office skills

Schedule flexibility: 4

Duties:

• Scheduling meetings

• Managing clients’ inbox

• Helping with administrative work

Bojan89/istockphoto

Average hourly wage: $28

Job description: A writer can work with many different brands as a freelance copywriter and can choose when they want to take on new projects and what hours of the week they work on them. Working as a freelance copywriter is also a great side hustle.

Requirements: Bachelor’s degree and industry experience

Schedule flexibility: 5

Duties:

- Research

- Writing copy

- Editing copy

Tempura/istockphoto

Average hourly wage: $35

Job description: Freelance web designers work independently designing websites for a variety of clients, instead of a full-time job. Work-from-home web design can be a well-paying and fulfilling job for antisocial people.

Requirements: Knowledge of design programs, and HTML and CSS programing languages.

Schedule flexibility: 3

Duties:

- Design web pages and sites

- Code designs

- Present to clients and incorporate feedback

Tatiana Buzmakova/istockphoto

Average hourly wage: $31

Job description: Similar to copywriters, editors can work freelance for multiple clients.

Requirements: Bachelor’s degree and industry experience

Schedule flexibility: 4

Duties:

- Nurturing writers

- Editing copy

- Publishing content

(Learn more at: Personal Loan Calculator)

kupicoo/istockphoto

Average hourly wage: $37

Job description: A business consultant can offer services to multiple businesses who need support as a whole or who are looking to improve a certain area of their business, such as their marketing efforts, operations, or HR.

Requirements: Bachelor’s degree, master’s degree (more advantageous), or a certification from a business consultant association.

Schedule flexibility: 3

Duties:

- Assess potential areas of improvement

- Create improvement plans

- Find ways to cut costs

mapodile/istockphoto

There are plenty of great flexible-schedule jobs that millennials and Gen Zers can pursue to give them the time they need to attend school, start a business, or take care of young children. Some remote freelance roles can be entirely flexible — such as web designers, writers and editors — while other jobs require your presence during certain core hours.

Choose whether you prefer a more physically demanding job — such as landscaper or fitness worker — or an office job that requires a laptop (like virtual assistant). It may take time to find the right position, so be patient. It’s also a good idea to keep an eye on how your money comes and goes to ensure you’re sticking to your savings goals.

Take control of your finances with the SoFi Insights money tracker app. Connect all of your accounts in one convenient dashboard. From there, you can see your various balances, spending breakdowns, and credit score. Plus you can easily set up budgets and discover valuable financial insights — all at no cost.

This article originally appeared on SoFi.com and was syndicated by MediaFeed.org.

SoFi’s Insights tool offers users the ability to connect both in-house accounts and external accounts using Plaid, Inc’s service. When you use the service to connect an account, you authorize SoFi to obtain account information from any external accounts as set forth in SoFi’s Terms of Use. SoFi assumes no responsibility for the timeliness, accuracy, deletion, non-delivery or failure to store any user data, loss of user data, communications, or personalization settings. You shall confirm the accuracy of Plaid data through sources independent of SoFi. The credit score provided to you is a Vantage Score® based on TransUnion™ (the “Processing Agent”) data.

Non affiliation: SoFi isn’t affiliated with any of the companies highlighted in this article.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

damircudic/istockphoto

deepblue4you/istockphoto

Featured Image Credit: zamrznutitonovi/istockphoto.