This or That?

That’s how the lyrics of a 1991 hip hop song called, “The Choice is Yours” start off — and although the rest of the song has no relation to investing, the words frame this blog post perfectly. Apropos of absolutely nothing, the 90s still hold the gold medal for the best hip hop ever made, IMO.

In any event, I thought I’d take a detour from my typical macro-driven blog posts and write one that aligns more with executable trade ideas. But these trade ideas are all a choice of either-or, with each option diametrically opposed to the other.

Why take this approach? Partially because it seems to fit the tone of today’s market and the pressure to choose sides. Partially because comparisons of opposing assets are a way to use the “tape” as our guide, without getting too locked in on one set of securities that simply proves our own point (aka, confirmation bias). And partially because it exaggerates the point, only to prove that exaggeration is actually the enemy.

So let’s explore some choices in the land of “this or that?”

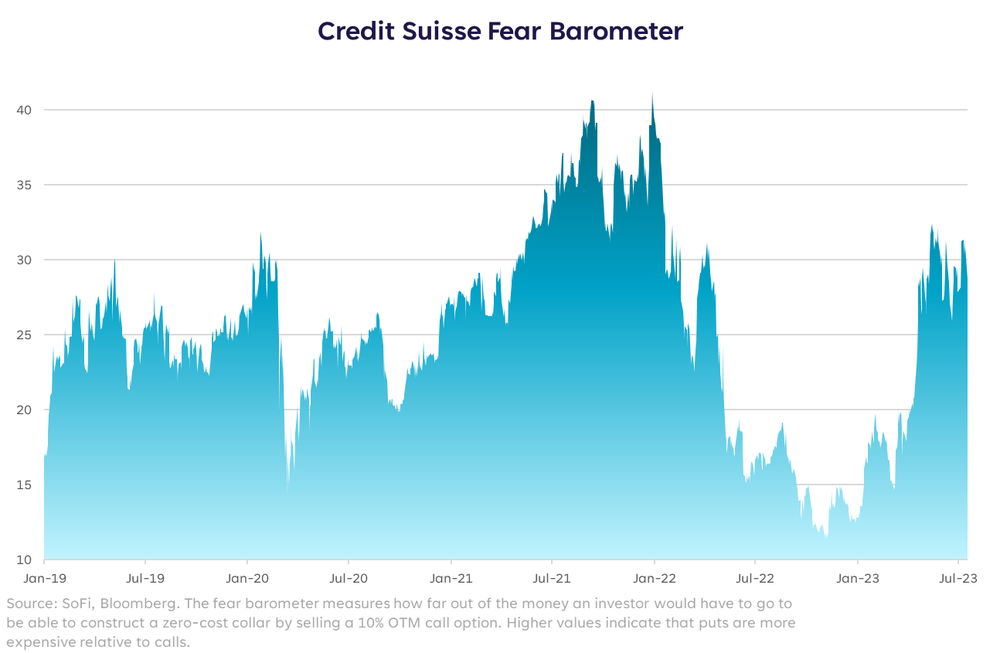

My Fear or Your Fortune?

The first choice is between puts or calls on the S&P 500, with puts representing those who are betting that the market will fall (i.e., purchasing downside protection, or the option to sell at a certain price), and calls representing those who are betting the market will rise (purchasing the option to buy at a certain price).

We start by looking at current market conditions using the Credit Suisse Fear Barometer as our guide. The price of puts and calls works like any other asset—the more demand there is, the more the price rises, and vice versa. This index measures them together, by taking the cost of puts (downside protection) relative to the cost of out-of-the-money calls (upside expectation). The result is a measure of how much people have to pay for protection at any given moment.

Naturally, the higher the cost of protection, the more “fear” is embedded in the market.

The cost of protection has been on a steady increase for most of 2023, with the most recent months in a range of what I’ll call “medium-high to high,” and marking the most demand for puts since early 2022, when the S&P hit its cycle peak.

The question I’ll come back to then is, this or that? Puts or calls? On one hand, puts are pricey and calls are cheap. Valuations alone would tell you there’s less risk in calls. But options aren’t just about valuations, they’re about getting the direction right, or at least allowing you to sleep at night.

At these levels, and judging by what usually happened on this chart after a spike in “fear,” I’d choose puts here even though they cost more. But that doesn’t make me right and call buyers wrong. It’s simply a choice given my expectations.

That’s what markets are, after all. A collection of investor choices on any given day, and in order for markets to function, those choices are often in opposition to one another. Let’s keep going.

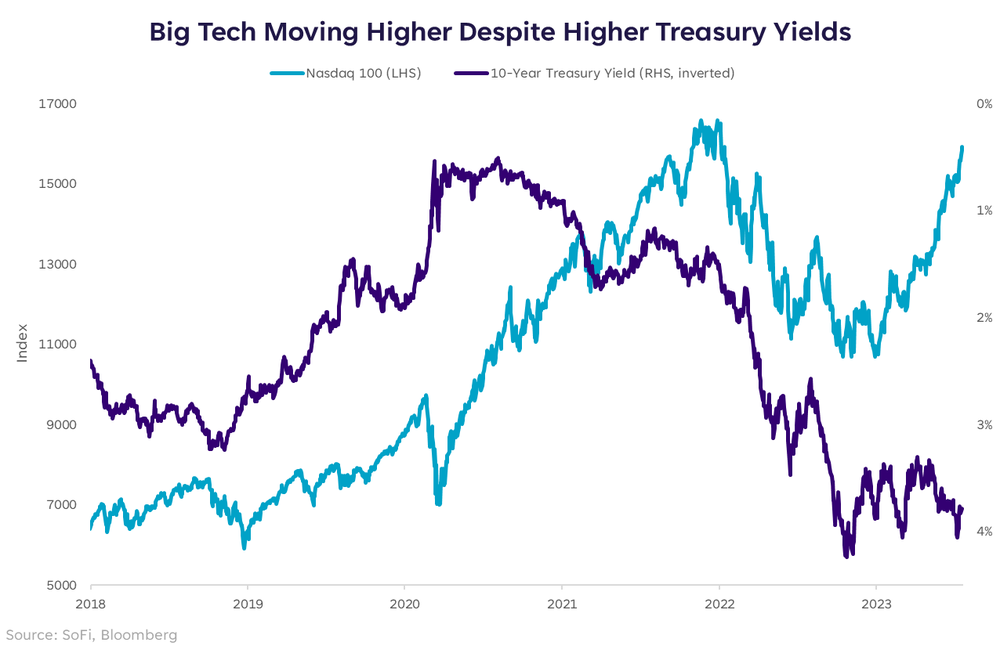

New Age or Old Hat?

This trade choice is about as diametrically opposed as it gets in today’s market. Technology stocks or Treasury bonds?

It’s no secret that Tech stocks have staged a major comeback so far in 2023, with the Nasdaq 100 up over 45% YTD. Treasurys (as measured by the 10-year yield, inverted below) have been more volatile and are actually down 0.2% YTD, while seeing three swings of 70-75 basis points in yield so far this year. Regardless, tech stocks climbed higher in an almost perfectly straight line.

Since rising yields mean falling prices, we’ve inverted the Treasury yield on this chart to illustrate a corresponding drop in value of the security.

I ask the question again, this or that? Tech or Treasurys? Much like the previous comparison, this decision is ultimately a reflection of an investor’s opinion on market direction. Tech may have more room to run up, that’s the beauty of stocks — they have no upper limit. Similarly, Treasurys may have more room to fall — especially if the Fed becomes more hawkish or inflation proves more stubborn.

There is no right or wrong, only opinions. My opinion from looking at this chart is that each line has seen a meaningful move, and one that appears extreme compared to the last 5+ years. In that case, I’d choose the trade that looks closer to the bottom of its range than the top — and for me, Treasurys it is.

(Learn more at Personal Loan Calculator).

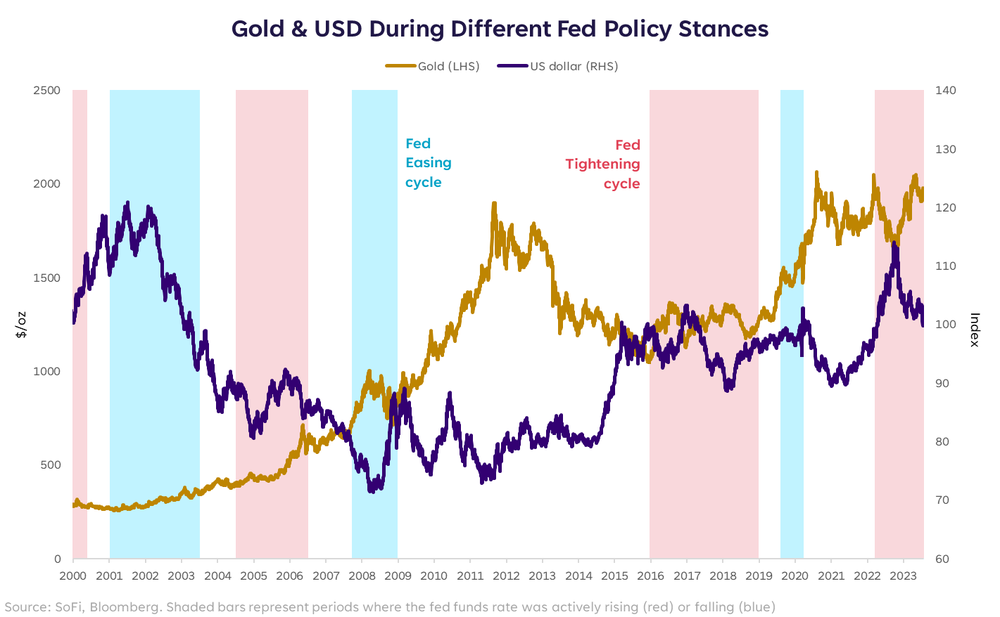

Shine Like Gold or Lead Like Washington?

Last, but certainly not least, is the choice between the US dollar and Gold. This one is, perhaps, the most difficult to choose between by simply looking at a chart and trying to discern a takeaway, but it’s not for lack of trying (believe me, I tried).

The conversation lately has been more dollar-centric as the Fed nears the end of its tightening cycle and the dollar has lost value by the pure nature of interest rate expectations and differentials around the globe.

Gold, on the other hand, has seen a nice rise this year…but that rise is impossible to detach from the fall in the dollar since these tend to move at least loosely, in opposite directions.

We tried to distinguish a clear direction in either by looking at historical tightening and easing cycles. Unfortunately, any determination I would try to make based on that would be unconvincing at best.

Which means we’re left with a choice that may need to be made based more on theory than recent price moves. And theories are just that…theoretical. But in any event, we still must choose for purposes of this game I’ve forced us into.

Currencies are one of the trickiest asset classes to analyze, because they’re affected by so many moving pieces at once. Not the least of which is what every other country is doing with theirs. One of the most important drivers, however, is the corresponding country’s level and direction of interest rates. Since we are quite confident that the Fed is nearing the end of its hiking cycle, the direction of rates in the US is likely to be interpreted by markets as sideways-to-down over the next 12 months. As such, the US dollar has fallen for a reason, and it would seem even more reasonable for it to remain at these levels or fall further.

On the contrary, to the extent that investors still view Gold as a store of value, it has, and could continue to, benefit from a weaker dollar, elevated global inflation, and an uncertain path for crypto assets.

If I were making a pros and cons list, Gold wins this one. But to be clear, in the case of an economic downturn, both of these assets may experience an upward bump.

Eeny, Meeny, Miny, Moe

Markets are made of choices, not teams. Opinions, not face-offs. Although this post outlines choices between three sets of options that are seen as opposites in many investors’ eyes, the main point at the end is that it doesn’t always have to be one or the other and a zero-sum game.

I’ve outlined which trades I would favor in each of these scenarios, but that doesn’t mean I can’t own both. There is a difference between being overweight and underweight, vs. being all-in or all-out. In this environment perhaps more than most, the nuanced gray area is where investors may come out best in the end. Don’t we all have the same goal anyway? To make money. With that in mind, everyone is actually on the same team.

This article originally appeared on SoFi.com and was syndicated by MediaFeed.org.

Please understand that this information provided is general in nature and shouldn’t be construed as a recommendation or solicitation of any products offered by SoFi’s affiliates and subsidiaries. In addition, this information is by no means meant to provide investment or financial advice, nor is it intended to serve as the basis for any investment decision or recommendation to buy or sell any asset. Keep in mind that investing involves risk, and past performance of an asset never guarantees future results or returns. It’s important for investors to consider their specific financial needs, goals, and risk profile before making an investment decision.

No brands or products mentioned are affiliated with SoFi, nor do they endorse or sponsor this content.

Communication of SoFi Wealth LLC an SEC Registered Investment Advisor

SoFi isn’t recommending and is not affiliated with the brands or companies displayed. Brands displayed neither endorse or sponsor this article. Third party trademarks and service marks referenced are property of their respective owners.

Communication of SoFi Wealth LLC an SEC Registered Investment Adviser. Information about SoFi Wealth’s advisory operations, services, and fees is set forth in SoFi Wealth’s current Form ADV Part 2 (Brochure), a copy of which is available upon request and at here. Liz Young is a Registered Representative of SoFi Securities and Investment Advisor Representative of SoFi Wealth. Her ADV 2B is available at here.

Americans waste money every day on these things

https://www.msn.com/en-us/money/personalfinance/americans-waste-money-every-day-on-these-things/ss-AA1d0wBP

No one sets out to waste money. But sometimes, it can feel as if you have thrown your hard-earned cash right down the drain.

How you spend your cash is, of course, up to you. Some may allot cash towards restaurants or Pilates classes, and that’s okay. As long as it’s a healthy spending habit and it falls within the predetermined budget, who’s to say it’s a bad idea?

But, that said, you may feel you want to cut back a bit on your outflow of funds. How to do so? Not everyone is a budget brainiac. Many people could use some help analyzing where their cash is going and whether that’s a good use of their funds.

So here are some common spending habits where you may be wasting money without even realizing it. Take a closer look, and you may find ways to save.

izzetugutmen/istockphoto

Set it and forget it is great when it comes to automating your personal finances, but it’s less than ideal when it comes to subscription services. 84% of American homes have at least one streaming service subscription, and the average US subscriber has signed up for four services.

On top of streaming entertainment services, plenty of American consumers subscribe to a box service, like Dollar Shave Club, Hello Fresh, or FabFitFun. Whether a person is ready to ditch some monthly services or not, they can try tracking their monthly recurring spending on a spreadsheet, using their bank’s app, or enrolling in a free service, like Trim or Hiatus, to catch those monthly bills.

From there, subscribers can decide what stays and what goes. What might be worth the cost based on frequency, or what is worth canceling because they didn’t even realize they were signed up. For instance, you might decide to save on streaming services and reduce the number of subscriptions you have on that front. (Learn more at Guide to Prime Loans).

Stock photo and footage/istockphoto

Buying groceries is an essential part of budgeting, but it’s one everyone should keep an eye on. Purchasing too many groceries, or creating food waste can be a big wasted expense. The average American throws away 219 pounds of food a year, and the average U.S. family of four will throw away $1,500 worth of food in a year. Meal planning and buying only what’s needed can help spend less on food and reduce waste, too.

But, groceries aren’t the only area where money is wasted on food. The average home in America spends nearly plenty on food away from home, which includes home delivery.

Dining out is great for special occasions, and, yes, ordering in makes sense sometimes, too. But eating even a few more meals at home a week can lead to some serious long-term savings.

LordHenriVoton/istockphoto

When a purchase is one click away, buying things on impulse becomes almost automatic. It makes ordering new pens or purchasing a latte on the way to work easy, and many of us rationalize the purchase because it’s only a dollar or two.

But a dollar or two adds up faster than most of us think. According to one recent survey, the average American can spend as much as $300 a month on impulse purchases.

Impulse spending ranges dramatically from shopper to shopper, but curbing it can look the same across the board. Try implementing the 30-day rule on most purchases. That means letting something sit in a digital shopping cart for 30 days before determining if it’s worth purchasing.

Slowing down the buying cycle can help separate want from need and prevent purchases that are forgotten moments after the transaction.

oatawa/istockphoto

Some of us leave cash sitting on the floor of our closets. Ordering clothing and other items online has become fast and seamless, but when something doesn’t meet our expectations, returning it becomes a chore. So we let it sit.

Obviously, summoning your energy to deal with unwanted items and return them is one solution. But here’s another: Buyers with a closet full of unworn clothes (some of which are probably just sitting there because you got tired of them) can try to recoup some of the money spent by finding places to sell your stuff. These can range from local consignment shops to online marketplaces like Poshmark or Depop. (Learn more at Home Affordability Calculator).

Bet_Noire/istockphoto

Transportation costs are a necessity in budgeting. But, many of us don’t account for the true cost of transportation, whether that’s fees associated with parking, or the occasional Uber ride.

Owning a car comes with additional expenses, such as gas, insurance, and maintenance, not to mention parking expenses, which can add up quickly.

Moves to make include figuring out how to save on gas, DIY-ing some simple car maintenance jobs, and opting for public transportation when possible.

monkeybusinessimages/istockphoto

Many Ameicans might not even realize how much they’re being charged simply for accessing their money. The average bank overdraft fee is around $35. If a person isn’t paying attention, they could overdraw multiple times before realizing what they’ve done and end up with a negative balance.

Some banks will even charge customers just for holding an account with them. The cost of these service fees vary, but average to more than $5 per month.

Finally, ATM fees can take a chunk out of a customer’s account in moments. When someone chooses to use an ATM outside of their bank’s network, they’ll pay $4.66, on average, each time they withdraw money.

mladenbalinovac/istockphoto

There are ways to reduce the amount of money you may be wasting, from finding a better budget to cutting down on food and car costs, to lowering the bank fees you are paying.

This article originally appeared on SoFi.com and was syndicated by MediaFeed.org.

Please understand that this information provided is general in nature and shouldn’t be construed as a recommendation or solicitation of any products offered by SoFi’s affiliates and subsidiaries. In addition, this information is by no means meant to provide investment or financial advice, nor is it intended to serve as the basis for any investment decision or recommendation to buy or sell any asset. Keep in mind that investing involves risk, and past performance of an asset never guarantees future results or returns. It’s important for investors to consider their specific financial needs, goals, and risk profile before making an investment decision.

The information and analysis provided through hyperlinks to third party websites, while believed to be accurate, cannot be guaranteed by SoFi. These links are provided for informational purposes and should not be viewed as an endorsement. No brands or products mentioned are affiliated with SoFi, nor do they endorse or sponsor this content.

Communication of SoFi Wealth LLC an SEC Registered Investment Advisor

SoFi isn’t recommending and is not affiliated with the brands or companies displayed. Brands displayed neither endorse or sponsor this article. Third party trademarks and service marks referenced are property of their respective owners.

Communication of SoFi Wealth LLC an SEC Registered Investment Adviser. Information about SoFi Wealth’s advisory operations, services, and fees is set forth in SoFi Wealth’s current Form ADV Part 2 (Brochure), a copy of which is available upon request and at here. Liz Young is a Registered Representative of SoFi Securities and Investment Advisor Representative of SoFi Wealth. Her ADV 2B is available at here.

Torjrtrx/istockphoto

ljubaphoto/istockphoto

Featured Image Credit: tdub303/istockphoto.