It seems that tax season has a way of sneaking up on us every year. Avoid scrounging for old receipts and scrambling to reconcile your books while trying to run a business by familiarizing yourself with important tax dates and deadlines early on.

Planning for the long term can feel daunting, especially when it comes to filing taxes for your small business. But this year will be different because you’ll be ready. We’ll show you how.

The key to staying on top of it all is to start now. Planning for the interim IRS due dates can ensure you’re on track and ready to close out your year. That’s why we’ve created a 2023 tax calendar. Use it to minimize your risk of accruing unnecessary penalties and interest costs.

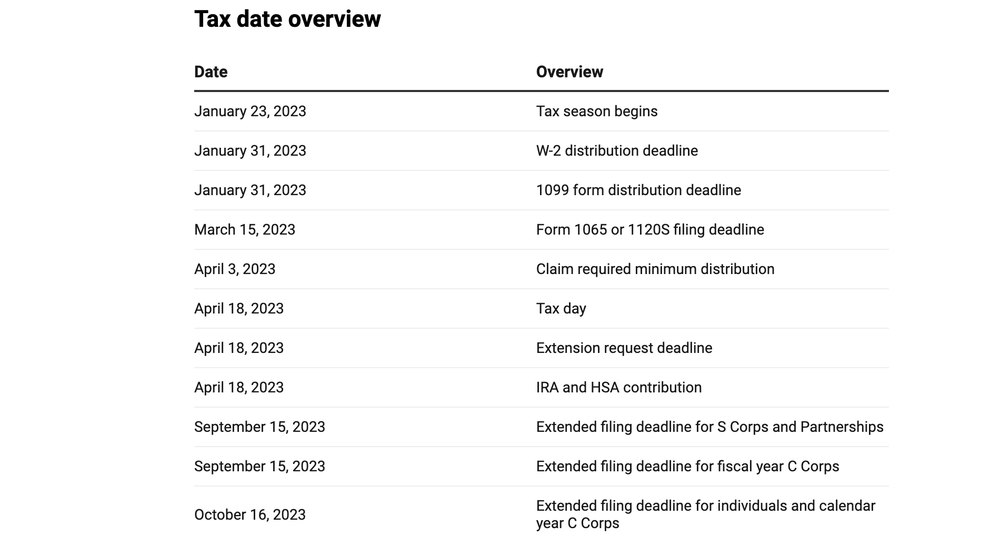

2023 tax date overview: When is tax season?

The 2023 tax season officially begins on January 23, 2023, and ends on April 18, 2023, unless you apply for an extension before the filing deadline. The exceptions to this rule include:

- Partnerships (including Multi-Member LLCs)

- S Corporations

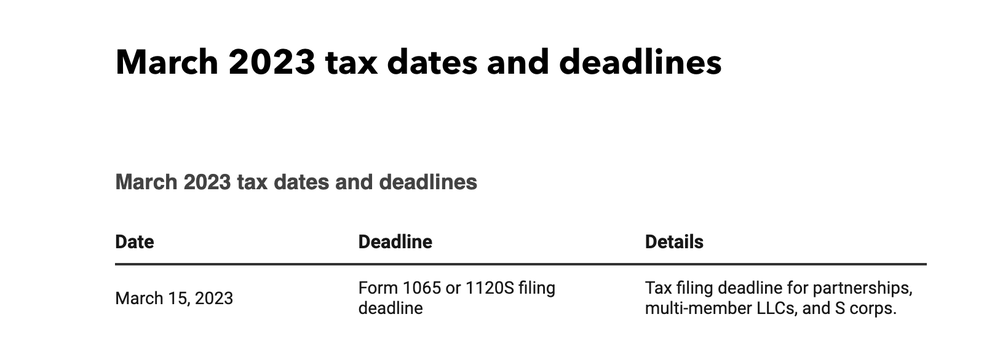

These business structures must file Form 1065 or 1120S by March 15, 2023, if they adhere to the calendar year instead of a fiscal year.

You must also adhere to additional business tax dates throughout the year, such as quarterly payments.

Take a look at our tax calendar for more information on important upcoming deadlines.

Estimated tax payment and quarterly tax dates

Small business owners, contractors, freelancers, gig workers, and anyone who operates a business where taxes aren’t automatically withheld must pay quarterly.

These payments ensure that the individual or business pays a large percentage of the estimated tax liability during the year rather than in one payment when filing the tax return.

When are business taxes due?

For Individuals and C Corporations with a calendar year-end, the 2023 business tax filing deadline is April 18, 2023. For C Corporations with a fiscal year-end, the due date is on the 15th day of the 4th month after the end of the corporation’s tax year. However, a corporation with a fiscal tax year ending June 30 must file by the fifteenth day of the 3rd month after the end of its tax year.

For S corporations and Partnerships, the 2023 business tax filing deadline is March 15, 2023. For C Corporations with a fiscal year-end, your tax return will be due on the fifteenth day of the third month following the end of your standard tax year.

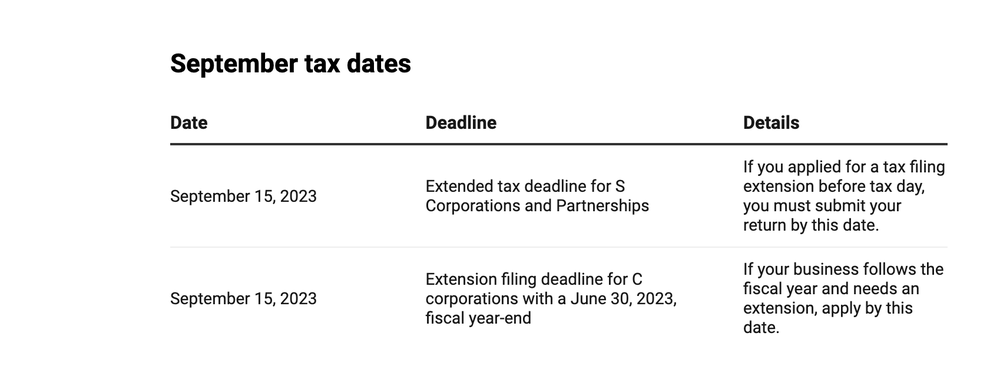

Note: Only sole proprietors and calendar year C corporations can file their taxes by Oct. 16, 2023, without paying any late fees if the IRS grants them an extension. Meanwhile, the filing deadline for S corporations and Partnerships only extends to Sept. 15, 2023.

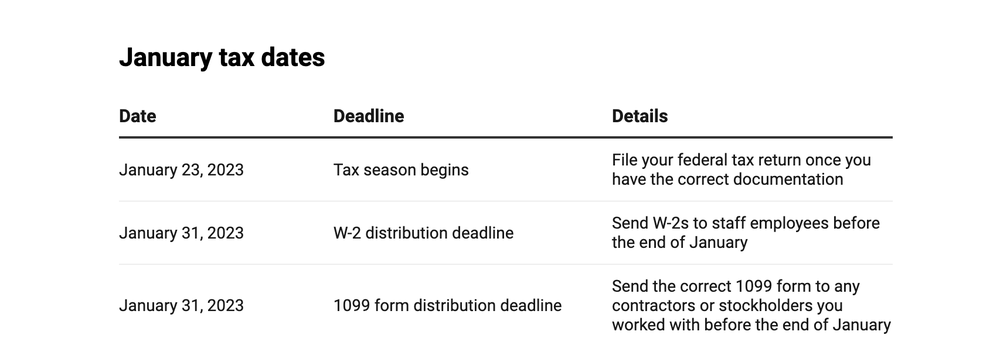

January 2023 tax dates and deadlines

March 2023 tax dates and deadlines

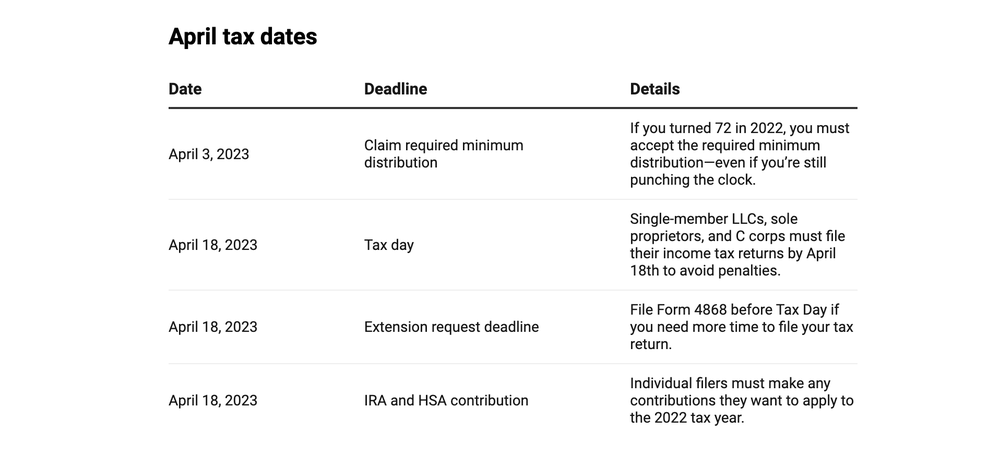

April 2023 tax dates and deadlines

September 2023 tax dates and deadlines

October 2023 tax dates and deadlines

Tax filing extension deadlines

If you need to request an individual tax extension, you must e-file or mail in your request by April 18, 2023. People experiencing the following circumstances may have special rules that don’t apply to the general public.

U.S. armed forces

If you were deployed in a combat zone in 2022, you may qualify for a tax filing extension. As a rule of thumb, you have up to 195 days following your final day of service to file any individual and business tax returns.

These special rules may vary among service members, so review the IRS’s combat zone tax filing guidelines and discuss any questions you may have with your tax advisor.

Disaster relief

Individual filers in FEMA disaster areas can mail in a request before May 15, 2023, to file their federal tax return late using Form 4868. Please review FEMA’s list of disaster situations to determine if you or your business qualify for an extension.

Tax refund dates: When will I receive my tax return?

Unless the IRS flags your business tax return for a review, you should receive any refunds in 21 days or less. Depending on when you file, your refund could appear in your bank account as soon as January. Or you can choose to receive your refund via check or to an account associated with a reloadable prepaid card.

Just keep in mind that if you file your return by mail, it may take longer to receive your refund than if you were to e-file.

If you want to keep tabs on the status of your tax refund, you can visit the IRS website to look as soon as 36 hours after you e-file.

Tax planning process

Start tax planning early to ensure you have time to meet with your tax advisor, formulate a plan to reduce your tax liability, and adhere to tax regulations. Ideally, you’d have a clear tax plan before heading into the new year.

Here are some action items to keep in mind for tax preparation:

- Meet with your CPA to discuss deadlines, deductions, and any outstanding questions about tax filing

- Gather payroll information, financial statements, and receipts for business expenses

- Organize federal (and state, if applicable) tax returns

- Prepare W-2s and 1099s

You can input new alerts into your calendar software, or write the dates in your planner.

Organize payroll and simplify your taxes

Proper tax planning requires you to submit tax documents on various due dates. Start this process by checking with your CPA to confirm the due dates and prep for the upcoming tax year.

Create a system to remind you when these dates are coming up, and include enough lead time to file the tax documents in a timely manner. You can input new alerts into your calendar software, write the dates in your planner, or download our 2023 tax calendar to stay on top of deadlines.

Related:

- Black business owners and workers face greater financial and health care challenges, according to new QuickBooks survey

- Special report: Access to funding remains a challenge for women-owned businesses

This article originally appeared on the Quickbooks Resource Center and was syndicated by MediaFeed.org.

More from MediaFeed:

5 tips for organic business growth

It’s no secret that startups have a prodigious failure rate. In fact, according to a recent Entrepreneur.com study, the four-year survival rate for a startup is just 49%.

With demoralizing stats like this in mind, entrepreneurs may be tempted to grow their profits through any means necessary, including inorganic strategies like acquisitions or mergers. However, the truth is that business owners can achieve impressive growth through organic strategies as well, allowing them to retain control of the companies they built from the ground up.

DepositPhotos.com

Also known as “true growth,” organic growth refers to the process of growing a business by reducing costs and increasing sales, either by finding more customers or enhancing output to current clients. On the other hand, inorganic growth occurs when a company merges with or is acquired by a second business. Entrepreneurs should take the time to familiarize themselves with the advantages of organic and inorganic growth, as well as some of the top strategies for execution, so they can decide which is the best choice for their business.

As a new business owner, you’ll likely want to increase profits as quickly as possible. By employing inorganic strategies like mergers and acquisitions, startups can grow their businesses more quickly while taking advantage of resources such as stronger credit lines and expanded market resources. Additionally, joining with another company lets you take advantage of its expertise and experience in the industry to develop your own brand.

DepositPhotos.com

By merging with another business, you agree to hand over some of your control and equity to another company. Not only can your initial vision become diluted, but you may also be forced to take on new business and managerial challenges before you’re truly ready. In some cases, you may have to rush to grow your staff and production capabilities to keep up with demand.

On the other hand, organic growth techniques allow you to grow your business on your own timeline. Because you aren’t sharing control with another company, you can hire employees and expand sales at your own pace. Additionally, entrepreneurs who maintain their autonomy now can sell for a larger profit later when the company is fully developed.

While retaining control of your company offers many advantages over the long haul, it can make business growth challenging in the short term. Some entrepreneurs struggle to grow beyond their current marketplace, while others find themselves cut down by the competition. Additionally, new businesses must often fight to make ends meet from month to month. Fortunately, strategies exist to help startups grow their profits without handing over control to partners or investors.

Here are just a few of those strategies to help you grow your business organically:

DepositPhotos.com

Want to grow a business that will feed your family and employees for years to come? The first step on the road to entrepreneurial success is starting the right kind of company.

With home-based and e-commerce businesses, you can avoid expenses like rent and commuting during the early, lean years of your company. As an added bonus, working out of the home lets you write off parts of your mortgage and electric bill. You can then invest these savings back into the business to help you grow in the long term.

DepositPhotos.com

A common conundrum for new business owners is whether to take your full cut of the profits or invest the money back into your company. While you may be tempted to keep some of those hard-earned dollars for yourself, you should aim to reinvest gross profits whenever possible to help your business grow. Investing your own money shows prospective clients and lenders that you are confident in your company’s long-term potential.

Not sure where to put profits? When in doubt, invest in marketing, SEO and other tactics likely to generate more business for your startup. If your income permits it, you may also want to invest in employee training and technological improvements, as these can yield large profits down the line for your company.

DepositPhotos.com

No matter how happy your current clients are with your offerings, you will have trouble growing your business organically if you don’t put effort into finding new sales channels. If you don’t currently sell your goods online, you should definitely consider starting a website to expand your reach to other regions. Additionally, you can introduce new products, cross-market services to your existing clients and expand to different markets. For example, a company that specializes in SEO may want to expand its services to include social media and search engine marketing.

Finally, business owners should employ market segmentation to customize their strategies according to the specific channels they are leveraging and the specific markets they are trying to reach. This way, you can create unique campaigns based on customer location and demographics and watch your sales rates skyrocket.

DepositPhotos.com

As a new business owner, you may feel the urge to micromanage everything that happens at your company. However, the truth is that macro-management is a far more effective way of enabling organic growth for your startup.

To keep your company moving forward, you should train top employees to take over some of your daily responsibilities. While you may be tempted to keep costs down by hiring employees who will work for less, in the long run these staff members could end up costing you more if their efforts aren’t up to par. Find people you can trust to get the job done—even when you’re not around—so you can focus on growing and developing your business in the years to come.

DepositPhotos.com

From minimizing spending, to reinvesting profits back into the business, organic growth strategies help ensure that you will retain control of the company you worked so hard to build. Do your research, and consider all the growth strategies available in order to give your business the best shot at success.

Do you know how sales taxes are impacting your bottom line? Check out our sales tax calculator.

This article originally appeared in the QuickBooks Resource Center and was syndicated by MediaFeed.org.

DepositPhotos.com

Featured Image Credit: DepositPhotos.com.