The Future Is Further Away

Recently in a CNBC interview, I admitted what I’ve gotten wrong so far in 2023 is that I thought it would be more obvious by now that an economic contraction was imminent. Persistently strong labor data continues to roll in, baffling the bond market and bringing expectations for higher rates more in line with what the Fed is signaling for the rest of the year. I am as baffled as the bond market by some of the data.

Just two weeks ago, the market was expecting two rate cuts before the end of the year, which flew in the face of what the Fed was telling us they’d do. After hearing Jay Powell speak twice in less than a week, markets finally believed the message more and not only increased their expectations of the terminal (i.e., highest) rate, but pushed out the expectation for the first cut from November into December of this year.

The future is further away.

Jerome Powell reiterated in a speech on Tuesday that inflation is deflating, but the job is far from over. Markets cheered the interview, with both a risk-on rally in stocks and a dip in Treasury yields. Soft landing hopes and expectations remained in the spotlight, and there hasn’t been much new news to refute them.

As we await the rate level that the Fed deems “sufficiently restrictive,” the debate over the timing of this cycle is perhaps the topic that will test conviction the most. The fastest and most aggressive rate hike cycle in 40 years seems to have resulted in the calmest and slowest effect on the economy.

Again, the future is further away.

The Fed Funds rate above the 2-Yr Treasury yield suggests rates are already quite restrictive and should be having an effect on demand and activity in the economy.

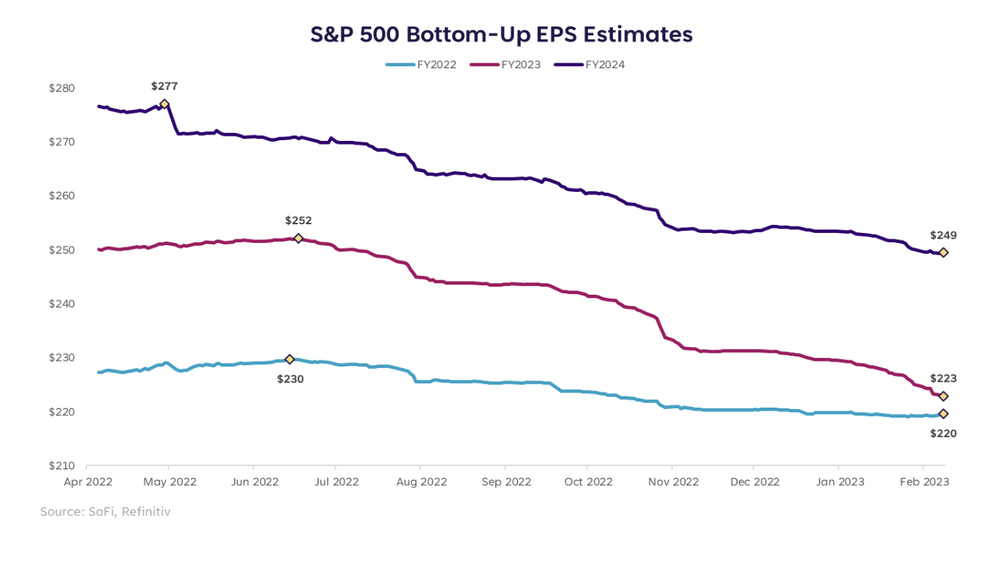

Meanwhile, a structurally tight labor market keeps companies in the hiring game and wages at an elevated level. But somehow, with higher wage costs and lower revenue projections, company earnings are still expected to grow in 2023 and 2024.

Everyone’s a Contrarian and Someone’s Wrong

Over the last 12 months we’ve experienced multiple short-term rallies and multiple bottoms afterward, with sentiment swinging wildly throughout.

After strong price action over the last 4 to 5 weeks, the contrarian view is now held by those who are cautious, and the increasingly popular view is soft landing or no recession at all. Just a couple of short months ago, that was reversed.

Regardless of your view, you could fall into the consensus and contrarian camps in the span of a few short weeks without shifting your opinion at all.

These quick reversals in sentiment and jumpy consensus views are exactly why calling inflection points in markets is so difficult. You’re on the right side of the call until you’re not, and if you change your investment allocation every time sentiment moves, the only thing consistently increasing in your portfolio is probably trading costs.

It Feels Too Easy

If the lows are in and we’re well on our way to happily ever after, most of the traditional indicators are wrong. There’s also the complication that Quantitative Easing has turned into Quantitative Tightening, and profit margins are contracting — albeit from very elevated levels.

Neither of those forces bode well for a clean and lasting bounce, but the muted effect so far supports equity market optimism.

Still, I think it feels too easy to be in the midst of a V-shaped boom. It also feels too easy that equity valuations deserve multiple expansion before the Fed even pauses, and that the economy can go on relatively unaffected by the most restrictive monetary policy we’ve seen since the early 80s.

My Dad was a basketball coach for decades, and one of his favorite phrases to use during timeouts and halftime pep talks was, “If it were easy, it wouldn’t be any fun.” I’ve always loved that quote and I say it to myself often. In the case of markets however, it would be great if it were easy once in a while. The reality is that it’s not easy, and this has been one of the hardest cycles to navigate in our lifetimes. But that’s what makes us all constant students of the market — and call me nerdy, but I did always think school was fun.

Learn More:

This article originally appeared on SoFi.com and was syndicated by MediaFeed.org.

Please understand that this information provided is general in nature and shouldn’t be construed as a recommendation or solicitation of any products offered by SoFi’s affiliates and subsidiaries. In addition, this information is by no means meant to provide investment or financial advice, nor is it intended to serve as the basis for any investment decision or recommendation to buy or sell any asset. Keep in mind that investing involves risk, and past performance of an asset never guarantees future results or returns. It’s important for investors to consider their specific financial needs, goals, and risk profile before making an investment decision.

The information and analysis provided through hyperlinks to third party websites, while believed to be accurate, cannot be guaranteed by SoFi. These links are provided for informational purposes and should not be viewed as an endorsement. No brands or products mentioned are affiliated with SoFi, nor do they endorse or sponsor this content.

Communication of SoFi Wealth LLC an SEC Registered Investment Advisor

SoFi isn’t recommending and is not affiliated with the brands or companies displayed. Brands displayed neither endorse or sponsor this article. Third party trademarks and service marks referenced are property of their respective owners.

Communication of SoFi Wealth LLC an SEC Registered Investment Adviser. Information about SoFi Wealth’s advisory operations, services, and fees is set forth in SoFi Wealth’s current Form ADV Part 2 (Brochure), a copy of which is available upon request and at www.adviserinfo.sec.gov. Liz Young is a Registered Representative of SoFi Securities and Investment Advisor Representative of SoFi Wealth. Her ADV 2B is available at www.sofi.com/legal/adv.

More from MediaFeed:

Should you be saving or investing right now? Here’s how to tell

Many people use the terms saving and investing interchangeably because they go hand in hand to ensure financial stability. But saving and investing have many differences that you should know when planning for your financial future. In general, saving provides a safety net for unexpected expenses and short-term spending goals, while investing is a strategy to help build long-term wealth. Being aware of these differences can help you prepare the best financial foundation for yourself and your family.

AaronAmat / iStock

The main difference between saving and investing is the amount of risk you are willing to take to reach financial goals.

When saving, you generally want a low-risk option to build and maintain wealth. Saving is when you gradually set aside funds — maybe a portion of your paycheck — in a safe place, like a savings account or money market account. These accounts allow you to store cash that can be easily accessible and have little risk of loss of value. Saving is often intended to reach shorter-term financial goals, like creating a fund for emergencies or saving a house down payment.

Investing is when you put money at risk to make more money. When investing, you may trade stocks, mutual funds, or other assets because there’s a potential for a return on the investment, but you are also at risk of losing the value of the investment. The goal of investing is to grow your wealth over time by taking advantage of capital appreciation and compound interest. This strategy is typically used to reach long-term goals, like building wealth for retirement or saving for a child’s college fund.

SoFi

Saving and investing is not an either/or proposition. Generally, saving and investing go hand in hand to ensure financial stability. However, certain scenarios make one strategy better than the other.

DepositPhotos.com

Building up emergency savings is one of the first things to do before you start investing. An emergency fund would ideally help you following an unexpected financial event, like paying a hefty medical bill or covering expenses if you were to lose your job. It is recommended that you save the equivalent of three to six months of expenses and debt payments in an emergency savings fund.

Ivan-balvan / istockphoto

If you need money for short-term goals, like a down payment on a house or an upcoming vacation, you should choose to save. A high yield savings account or a money market account may be the best option to save for these short-term goals.

monkeybusinessimages/istockphoto

Savings accounts are highly liquid, meaning that you can access the money in your account as soon as possible. You can go to your bank, withdraw funds from a savings account, and have the cash right away.

DepositPhotos.com

Here are some tips for deciding when you should decide to invest.

nortonrsx

Paying off high-interest debt, such as a credit card balance, will likely provide you with a sound financial foundation. You’re paying off an interest rate that’s likely higher than potential investment returns. Once you pay off high-interest debt, you can look to invest money in stocks, bonds, and other assets.

Recommended: Paying Off Debt—9 Strategies to Try

travellinglight / istockphoto

There is potential for greater rewards when you invest because of a capital appreciation and compound interest. But when you invest, there is no guaranteed return on your investment, and you can lose part or all of the funds. This risk-reward calculation is best for long-term goals, because you can withstand the volatility of the financial markets. This strategy is best for building a retirement nest egg or savings for a child’s college tuition.

Tinpixels

Contributing to an employer-sponsored 401(k) or an Individual Retirement Account (IRA) should be your first step in building wealth for retirement. These retirement accounts provide tax-advantaged ways to invest your money. Once you’ve maxed out contributions to these accounts, it may be good to explore additional investment products.

Recommended: IRA vs 401(k)—What is the Difference?

DepositPhotos.com

- FDIC Insurance: You want to make sure the Federal Deposit Insurance Corporation (FDIC) insures your savings accounts. The FDIC guarantees up to $250,000 in nearly all savings account products if your bank fails.

- Interest Rate/APY: Many traditional banks pay little interest on savings account deposits, so you may want to shop around to see where you can get the best rate. Certain institutions offer higher interest rates than large, brick-and-mortar banks.

- Fees: You want to look for savings accounts with little or no fees. Many banks may waive fees if you have a large enough balance or enroll in direct deposit, while other institutions won’t charge a fee no matter what.

Prostock-Studio / istockphoto

- Diverse investment options: You want to ensure your brokerage firm offers a wide range of investment products, including stocks, bonds, options, ETFs, and mutual funds. Additionally, brokerage firms that provide individual retirement accounts (IRA) may be ideal if you’re looking to save for retirement.

- Commissions/Fees: High commissions and fees can eat away at your investments, so you want to look for brokerage firms with low investment fees.

- Account Minimums: Many brokers require that a customer deposit a minimum amount to open an account. Depending on your financial situation, you may want to look for a brokerage account with an account minimum that you can afford without straining your finances.

EmirMemedovsk

Another thing to consider when deciding between saving and investing is how inflation affects your money with each strategy. With investing, there is a potential for your investments to keep up with inflation, which may be ideal in a high inflation environment. In contrast, inflation may eat away at your savings because the money you put into your account today will be worth less a year from now.

Nonetheless, no one strategy works for everyone because financial situations differ, as do financial goals and comfort with risk levels. The real question isn’t whether you should save or invest; it’s more about how to include a combination of both to meet your financial goals.

Learn More:

This article originally appeared on SoFi.com and was syndicated by MediaFeed.org.

SoFi Invest

The information provided is not meant to provide investment or financial advice. Investment decisions should be based on an individual’s specific financial needs, goals and risk profile. SoFi can’t guarantee future financial performance. Advisory services offered through SoFi Wealth, LLC. SoFi Securities, LLC, member FINRA / SIPC . SoFi Invest refers to the three investment and trading platforms operated by Social Finance, Inc. and its affiliates (described below). Individual customer accounts may be subject to the terms applicable to one or more of the platforms below.

1) Automated Investing—The Automated Investing platform is owned by SoFi Wealth LLC, an SEC Registered Investment Advisor (“Sofi Wealth“). Brokerage services are provided to SoFi Wealth LLC by SoFi Securities LLC, an affiliated SEC registered broker dealer and member FINRA/SIPC, (“Sofi Securities).

2) Active Investing—The Active Investing platform is owned by SoFi Securities LLC. Clearing and custody of all securities are provided by APEX Clearing Corporation.

3) Cryptocurrency is offered by SoFi Digital Assets, LLC, a FinCEN registered Money Service Business.

For additional disclosures related to the SoFi Invest platforms described above, including state licensure of Sofi Digital Assets, LLC, please visit www.sofi.com/legal. Neither the Investment Advisor Representatives of SoFi Wealth, nor the Registered Representatives of SoFi Securities are compensated for the sale of any product or service sold through any SoFi Invest platform. Information related to lending products contained herein should not be construed as an offer or pre-qualification for any loan product offered by SoFi Lending Corp and/or its affiliates.

SoFi Checking and Savings is offered through SoFi Bank, N.A. 2022 SoFi Bank, N.A. All rights reserved. Member FDIC. Equal Housing Lender.

nicoletaionescu / istockphoto

DepositPhotos.com

Featured Image Credit: DepositPhotos.com.