Going Once, Going Twice

At first glance, the topic of this week’s blog may sound dry and like something that’s only interesting to economists or professors. But Treasury auctions have turned into quite a hot topic lately.

But why? And why do they matter to investors?

For starters, the sizes of these auctions are rather large, particularly for a period of time when we’re not in a crisis. Additionally, the appetite for newly issued Treasuries has been waning due to a few large buyers exiting the scene (more on that in a minute). That’s showing up in the auction results, and sending tremors across bond and equity markets.

An important layer to the story is the rise in interest rates over the last 12-18 months. As rates rise, so do Treasury yields and coupons on newly issued debts, which increases the expense burden on the federal government (more on that in a minute, too), and our budget shortfall persists.

To be clear, nothing bad has happened yet. And there is a school of thought that nothing ever will, because so far, although the auctions have been met with weaker demand, they’re still getting done. And the U.S. is still the most credit-worthy country in the world, so a default or material deterioration seems highly unlikely, not to mention politically unsavory.

Buyers be Bygones

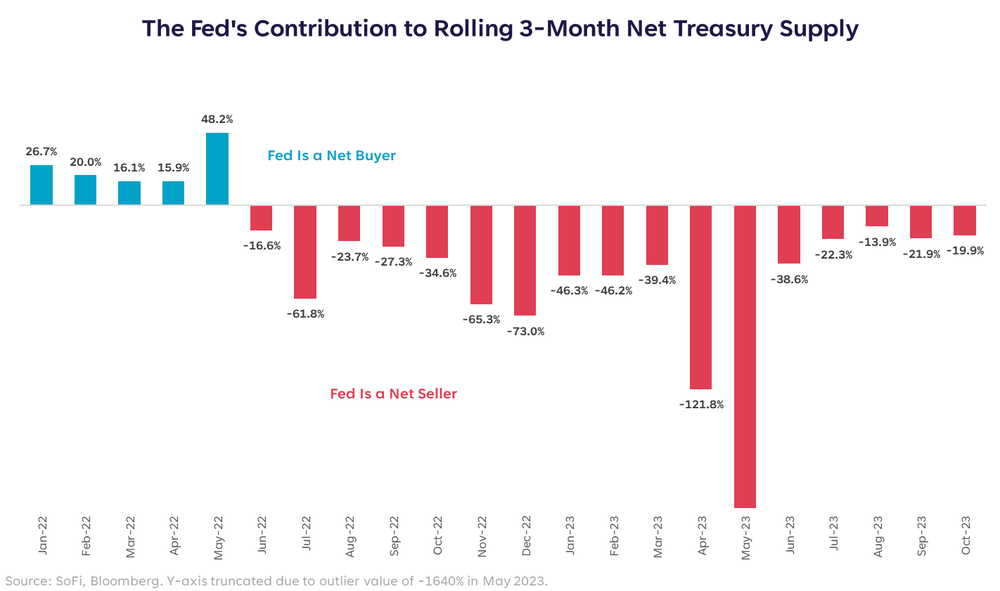

For a long time, there were three big buyers of US Treasurys: the Federal Reserve, Japan, and China. But all three of these big buyers have reduced their purchases, if not turned into net sellers of Treasuries.

We’ll focus mainly on the Fed in this piece since monetary policy is front and center. A big reason for the Fed turning into a net seller of Treasurys was its quantitative tightening program — intended to reduce the size of the Fed’s balance sheet and fight inflation — that began in mid-2022.

(Learn more: Personal Loan Calculator)

This shift had been well-telegraphed, and ended up being part of the catalyst that drove Treasury yields higher into the summer of 2022, with the 10-year yield rising to 3.47% (which, believe it or not, was eye-popping at the time). Little did we know, our eyes would completely burst the following October when it hit nearly 5.0%, but I digress.

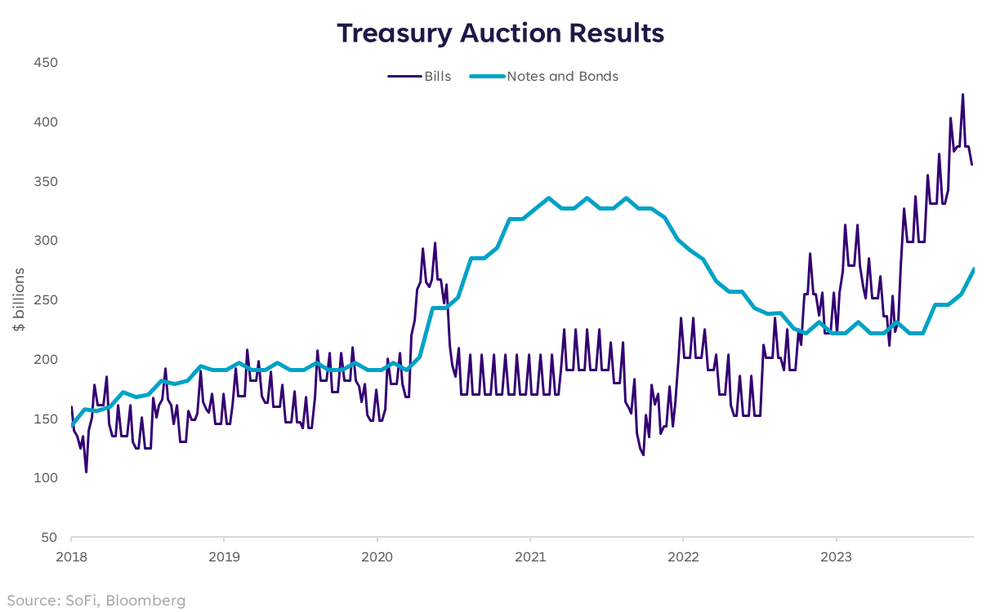

The problem with the Fed not acting as a net buyer anymore is that as big buyers stopped buying, the amount of debt we needed to issue started rising.

The chart above shows the trend of treasury issuance, divided into T-bills (maturities of one year or less), and T-notes and bonds (2 to 30-year maturities). We can see the rise in issuance in late 2020 to cover Covid-related fiscal stimulus.

Notice the rise in issuance in 2023, absent a crisis-related stimulus package. Not to mention the two times this year alone that we’ve worried about a government shutdown due to not being able to cover our obligations. Credit-worthy or not, the increasing amount of debt that needs to be absorbed without the usual suspects there to absorb it is more than mildly concerning.

Hot Potato Bonds

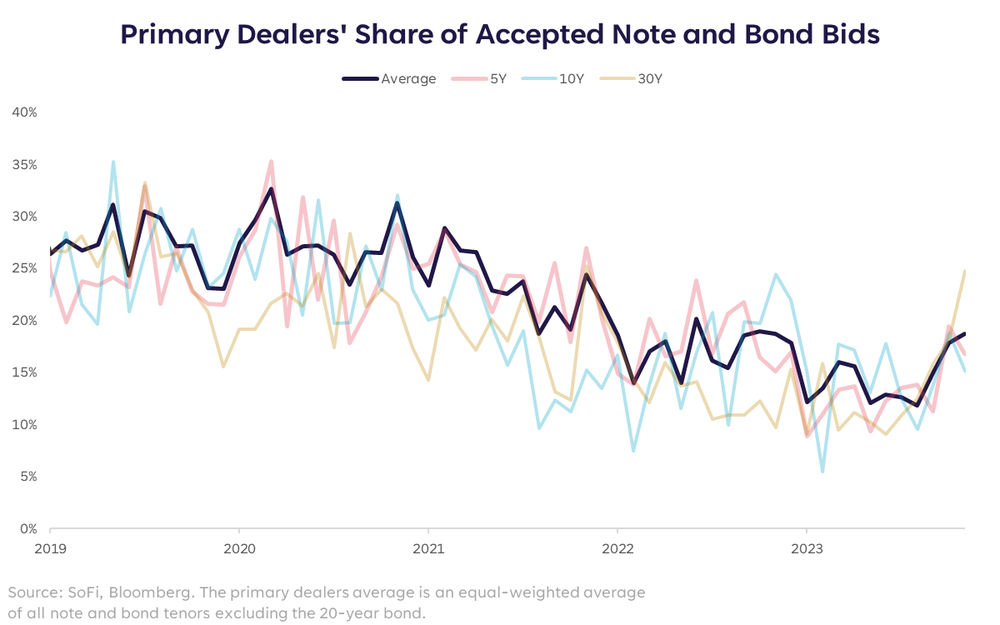

As with most things government-related, the way auctions function is not straightforward. Although it’s concerning that big buyers have reduced their buying appetite, there is a back-up plan called primary dealers . The plan is basically that whatever isn’t bought by other bidders in a Treasury auction, has to be absorbed by primary dealers.

That’s all well and good because they’re used to acting as the backup plan, and they’re active in every Treasury auction that takes place. The interesting part about the recent activity is that because there has been less demand from other buyers, the primary dealers have had to absorb an increasing amount of issuance.

It’s almost as if these auctions are becoming a game of hot potato.

Up, Up, and Away

As with any bond, if buying appetite is low, yields tend to move higher. But this is a period of falling inflation, rate cuts being priced in, and an equity rally driven largely by the swift drop in Treasury yields since mid-October.

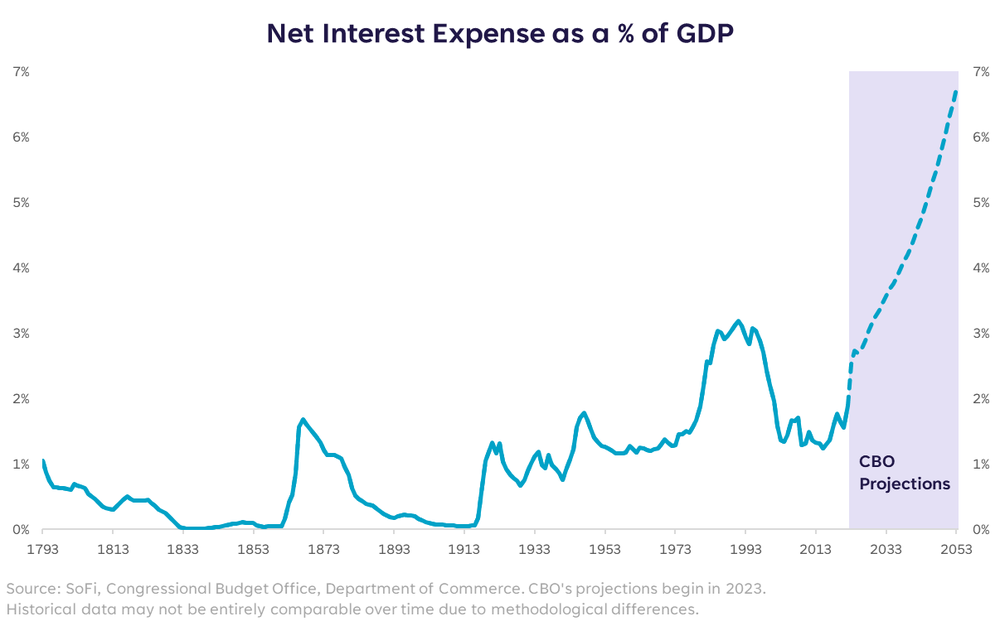

If these auctions continue to get weaker and weaker, they could serve as a catalyst for yields to rise again — creating a less friendly environment for stocks. Plus, much like the concept explained in the beginning of this piece, if yields go higher, so does the U.S. interest expense. And according to the Congressional Budget Office, net interest expense as a % of GDP is already projected to grow rapidly over the next few decades.

Needless to say, this topic has become one to pay attention to even if it feels far-removed from your financial life. It’s turned into a market mover, and one that isn’t sending signals of stability.

This article originally appeared on SoFi.com and was syndicated by MediaFeed.org.

Communication of SoFi Wealth LLC an SEC Registered Investment Adviser. Information about SoFi Wealth’s advisory operations, services, and fees is set forth in SoFi Wealth’s current Form ADV Part 2 (Brochure), a copy of which is available upon request and at adviserinfo.sec.gov. Liz Young is a Registered Representative of SoFi Securities and Investment Advisor Representative of SoFi Wealth. Her ADV 2B is available at sofi.

More from MediaFeed:

14 financial tips used by both experts & beginners alike

Nothing gets the adrenaline going like talking about, wait for it, personal finance tips! What a great discussion topic. Second only to talking politics.

Sarcasm aside… talking personal finances should be more commonplace. Maybe less of us would be in credit card debt, or using low interest savings accounts, or not investing at all, if we just opened up and talked finances once in awhile.

So I’ll start by doing my part and sharing my top 14 personal finance tips that everyone should act on today! These are the best personal finance tips out there and should be checked off by beginners and experts alike.

Here are the categories of personal finance tips that we’ll walk through, in order of what you should be tackling first:

- Budget better and set a baseline

- Save more money (and save better!)

- Make More Money

- Make your money work for you (a.k.a. investing)

DepositPhotos

Budget better and set a baseline.

Your net worth is arguably the most important financial metric for you to measure every month (or every 3 months or so). It’s your financial pulse and shows how healthy your financial situation is at any given time (and over time).

Yet, for some reason, we’re more interested in Bill Gate’s net worth than our own!

Well, that reason is his net worth is an astronomical number that’s fun to try and guess ($110 billion if you want to quiz a friend).

While guessing other’s net worth is fun, it won’t improve your financial situation. The only way to do that is to take stock of where you stand and determine your net worth today. Then, move onto tip #2!

You can learn how to calculate your net worth and get our free net worth tracking tool here.

.

SARINYAPINNGAM / istockphoto

Building a budget is no fun. I’ll admit it.

Though, it does have a ton of benefits. Mainly, the ability to save you money through:

- Providing financial clarity

- Giving your money a purpose

- Stopping frivolous spending

- Helping to prioritize saving

If you need to get a better grip on your money, you can learn how to build a budget from scratch here.

Building a budget is not for everyone. For some, it puts unnecessary restraints on spending, but if you’re seeking any of the benefits above then I’d consider giving budgeting a shot.

Depositphotos

A budget is only as good as the person managing it.

Luckily, you don’t have to keep track of it yourself!

I mean, you can if you want. I love a spread sheet as much as the next person, but I also have the whereabouts to understand that most sane humans don’t love spreadsheets and numbers as much as me.

Weird, I know.

Anyway, here are some great tools I found to help you track your spending over time:

DepositPhotos.com

Before moving on any further down the checklist of personal finance advice, it’d be smart to check your credit score. You can do so easily and for free at Credit Sesame.

If you’re net worth is the most important financial metric to check, your credit score comes in at a close second place. There are a lot of benefits associated with having a good credit score, including:

- Access to excellent credit cards

- Lower interest rates on loans

- Higher credit limits

- And much more

Knowing where your credit score stands is the first step to take in order to improve it (or to celebrate if you already have a good score!).

DepositPhotos.com

The easiest way to start saving money is to cut back on expenses. The key here is you aren’t completely cutting out expenses, you’re cutting back on them.

In other words, you’re negotiating better prices on goods and services you already use. Here are a few great resources to help you get started:

BillShark

BillShark negotiates lower prices on your monthly bills, saving you time, money, and hassle. They have an 85% success rate negotiating bills for cable TV, wireless phones, satellite TV, internet access, satellite radio, and home security.

The best part: it costs you nothing! They get paid by taking a portion of the savings they get for you. If there are no savings, then they don’t get paid. It’s a win-win.

Plus, they calculate your potential savings in less than 15 seconds. If you want to give them a shot, you can get started with BillShark here.

Gabi

Gabi is a full-service, online advisor who compares all of your home and car insurance options to find you the right policy, all in under two minutes. There is no need to spend hours shopping around yourself, Gabi does the work for you.

Read our full Gabi Insurance Review.

Arcadia Power

Arcadia Power was created to give everyone a simple, free way to choose renewable energy. Saving you money and helping the planet at the same time.

Learn more about if Arcadia Power is available where you live here.

Hack your location: Another great way to save money is through geoarbitrage.

After cutting back on expenses, it’s time to cut out expenses.

This includes cutting out things like unused subscriptions and any purchases you don’t value.

You could enlist the help of Trim (a handy app) to track down your unused subscriptions, set spending alerts, and overall be the personal finance assistant you may be looking for. I wrote a full review on Trim if you want to learn more about their service: Trim Review.

You could also go the old fashioned route, using what you learned from the net worth and budgeting exercises to revamp your spending habits. Which would include buying only things that matter to you and add value to your life.

Kenishirotie/istockphoto

Now it’s time to put your savings into overdrive.

If you’re using a traditional bank account, you could be receiving an interest rate as low as 0.01%. That’s $1 for every $10,000 you have saved with the bank.

If that’s the case, your bank is stealing from you. Point blank. Anything less than a 1% interest rate in a savings account today (as of January 2020) is unacceptable.

There is a solution to low interest savings account, and they are aptly named: high yield savings accounts. Most high yield accounts are offered by online banks and they typically offer interest rates above 1% (if not even higher).

A 1% interest on $10,000 is 100x better than most traditional banks, yielding $100 every year instead of the paltry $1 return.

If you’re looking for an online savings account, CIT Bank is a great place to start, and you check their site to get their current rates. Usually, they are very competitive.

Though, they’re not the only good option out there. You can view a full list of our favorite banks here.

DepositPhotos.com

What’s the best way to make more money?

How about getting paid more for what you already do with no extra work on your end needed.

Asking for a raise is not easy, but it’s a great way to make more money. You have to earn it and deserve it, though. The last thing you want to do is go in guns blazing demanding more money (especially if you aren’t a top performer). That’s a great way to lose a job!

Ramit Sethi has one of the best guides out there on how to ask for a raise. I suggest you check it out!

DepositPhotos.com

Ah, side hustles. The core tenant behind the new millennial dream of making passive income and then watching your bank account grow exponentially while sipping cocktails on a beach somewhere.

It’s not a bad dream. Who wouldn’t want to make money while you sleep?

It’s just not as easy as it sounds. Side hustles take a lot of work. I mean a lot.

If you have the work ethic though, they can be a great way to make some meaningful income and help you reach your personal finance goals. Here are some resources to check out if interested:

mangpor_2004 / Getty

cash")

If getting paid more for your current job or taking on a whole other one are out of the picture, don’t worry, you’re not out of luck yet.

Heck, even if you’re successful in tips 9 and 10, who isn’t always looking for a few extra bucks?

Here are two great apps to help you make some small-time cash, fast:

S’more

S’more is a lockscreen rewards app that allows you to earn points in exchange for them placing ads and content on your lockscreen.

If you don’t mind the ads, it’s a great way to earn some extra money.

Mistplay

Mistplay will pay you to play games!

That’s it, really. Play games, earn points, and then redeem them for gift cards and other monetary prizes!

sorrapong / istockphoto

Wait a minute, we’re in the make more money section still, right?

Yes, because credit cards are good for making money too! The sign-up bonuses, cash back, and rewards that credit cards offer can be a great source of income. Especially if you are using the best card for you.

Don’t leave money on the table by using the wrong credit card that under-rewards you. Here are some resources to help you find the right card that will offer you the best rewards based on your recent spending habits:

- Find the best credit card for you with our credit card tool

- View our credit card guide: How to choose the best credit card in 5 easy steps

- How to easily redeem Chase Ultimate Rewards Points

Farknot_Architect / istockphoto

Make your money work for you (a.k.a. investing)

The last level of personal finance tips is to put your money to work! Most finance experts agree, there is no better way to do that than to invest it.

With the stock market returning 7% on average every year, here’s what a $1,000 investment could look like after 40 years:

A roughly $14,000 ending value! Sign me up.

Investing is a crucial part of a wealth building strategy, and one of our most important personal finance tips. Here are some of the best resources to learn more about investing and how to set up your own long-term investing plan:

- Invest the lazy way: Set up a 3 Fund Portfolio

- Investing 101: How to Invest in Index Funds

- Invest with Betterment: See tip No. 13 on the next slide!

simonkr/istockphoto

Betterment is one of the most well-known robo-advisors, and for good reason. Investing with Betterment is easy – they are an established, modern robo-advisor that features an extremely easy-to-use platform.

At a high level, Betterment features:

- Best in class fees / expenses:

- 0.25% management fee ($25 for every $10,000 invested)

- Expenses ratios as low as 0.03% on ETFs (and as high as 0.25%)

- A wide variety of ETFs available

- An easy to use online platform

Not to mention, getting started with Betterment is easy, and we walk through exactly how to open an account. They’re a great option for beginners or anyone who wants to take a very hands off approach when it comes to investing.

If you want to learn more about Betterment before getting started, just read our full review here.

monkeybusinessimages/istockphoto

is optimized")

Your 401(k) is one of the most important investment accounts that you utilize. So why do so many of us sign up on day one of work to contribute some small percentage to it, and then never look at it again?

Honestly, it’s probably because it’s boring. We all have better things we could be doing that don’t involve planning for retirement and choosing between 401(k) account types.

That’s where Blooom comes into play. Blooom is a 401(k) robo-advisor that offers both:

- A Free 401(k) Health Check Up: Blooom can hook up to your 401(k) to review your account and provide recommendations on how to optimize your investments.

- Paid Ongoing 401(k) Management: Blooom offers ongoing 401(k) management, so you can take a more hands off approach and let them take the wheel.

You can learn more about Blooom in the full review we wrote here.

This article originally appeared on JustStartInvesting.com and was syndicated by MediaFeed.org.

DepositPhotos.com

Smart & simple ways to start saving right now

- Science says this ‘70s rock hit is the catchiest song of our time

- 20 incredible movies so disturbing we never want to see them again

Like MediaFeed’s content? Be sure to follow us.

adamkaz

Featured Image Credit: DepositPhotos.com.