Chutes and Ladders

With Chairman Powell’s testimony marking another message of “data dependency,” I can’t help but feel like every data point either sends the market down a chute or helps it climb a tiny rung on the ladder.

Given our careful watch on every data point, I thought it might be useful to highlight a couple of things that are new, whether because they’ve changed direction or because they’re signaling something with a louder horn than before. And when I say new, I mean within the last week.

A few of the things that have changed are: fed funds rate expectations, the depth of the 2-year/10-year yield curve inversion, and job openings in the construction sector.

Red Light, Green Light

I remember playing the game red light, green light as a kid, and despite its simplicity it was always fun because of the unpredictability and suspense. You had to be quick to react — and even a second of hesitation meant you probably didn’t win.

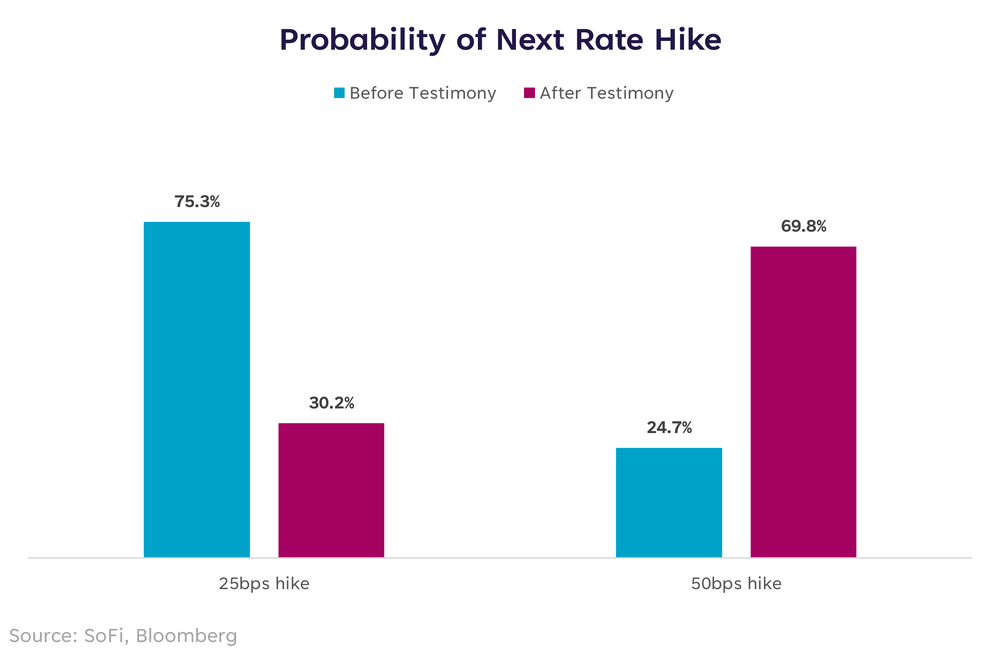

Unfortunately, we’re in a market environment where every data point feels that way. The most recent market-moving event was Fed Chair Powell’s testimony to Congress, which sent fed funds futures (the market’s expectation for where the fed funds rate will be) up in quick fashion. Red light.

We thought we had downshifted to only 25 basis point hikes from here on out, signaling not only that the Fed had a grasp on the pace and size of tightening, but also that it was working to bring inflation down and cool off overheated parts of the economy.

The message we got instead was that hikes may now increase back to 50 basis points — if warranted by hot econ data. What ensued (so far) has been a market sell-off as investors digested a possible jagged rate path.

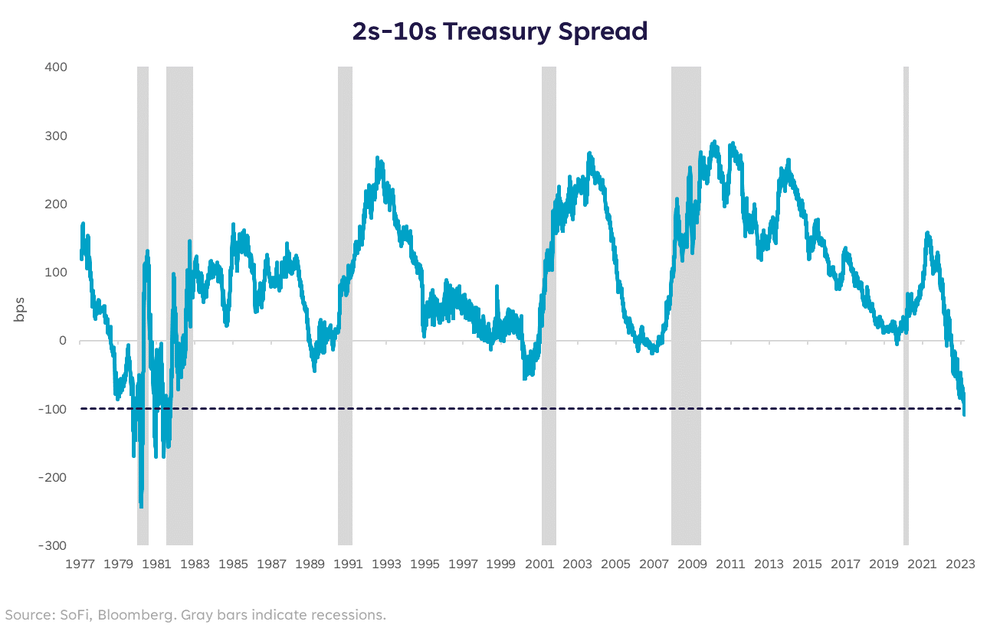

Moreover, the news pushed the 2-year Treasury yield up over 5% and caused an erratic reaction in the 10-year Treasury yield. The result was an inversion between the 2s/10s of more than 100 bps, a level we haven’t seen since the early 1980s. There are differing views on how predictive yield curve inversions are, and I can understand their muted importance as a signal at shallow and brief inversions, but crossing over the 100 basis point level is a pretty loud alarm, IMO. Red light.

Operation

I did not like the game of operation because it left so little margin for error. The good news was even if you got buzzed, you still got another chance. This data point is more of a buzz along the way, but one we should watch closely.

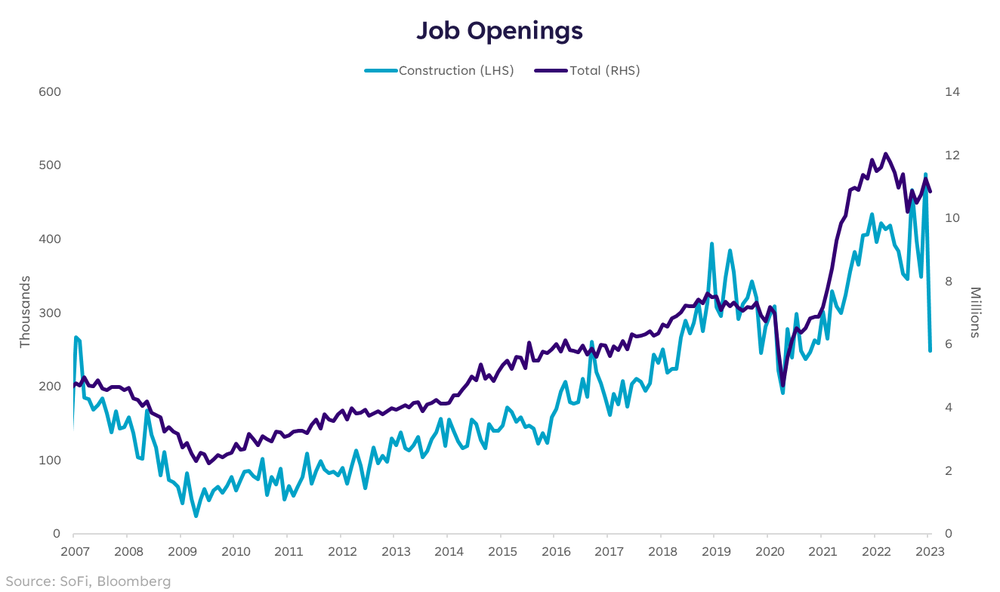

The JOLTS data (a.k.a. Job Openings) came in slightly weaker than last month (10.8 mil vs. 11.2 mil), but remained high and indicates the labor market is still tight. To be specific, the gap between unemployed people and jobs open is still 5.1 million. Digging deeper into the data though, the sector in January’s report that sticks out like a sore thumb is construction job openings.

Month-over-month, job openings in construction are down 49%. They’ve been erratic in recent months, but this move is bigger than the ones before. Much of this is likely due to softening in the housing market and less backlog of homes being built. Although the weaker housing market isn’t new news, the reason construction employment is important to watch is because it tends to be a decent leading indicator for the broad labor market.

Nothing more than a warning zap? Perhaps. For now, it’s simply a notable shift that I don’t want to overlook. But when we add it to recent announcements of commercial real estate defaults, and knowing that the residential real estate market is in somewhat of a holding pattern, it feels like a yellow light, at least.

In closing, although none of these data points in isolation directly signal impending doom, they do add to the list of things that keep me up at night. Despite my cautious tone, I won’t entirely count out a positive surprise and some sort of “drawdown averted” scenario. I just continue to see more evidence against it.

Learn More:

This article originally appeared on SoFi.com and was syndicated by MediaFeed.org.

Please understand that this information provided is general in nature and shouldn’t be construed as a recommendation or solicitation of any products offered by SoFi’s affiliates and subsidiaries. In addition, this information is by no means meant to provide investment or financial advice, nor is it intended to serve as the basis for any investment decision or recommendation to buy or sell any asset. Keep in mind that investing involves risk, and past performance of an asset never guarantees future results or returns. It’s important for investors to consider their specific financial needs, goals, and risk profile before making an investment decision.

The information and analysis provided through hyperlinks to third party websites, while believed to be accurate, cannot be guaranteed by SoFi. These links are provided for informational purposes and should not be viewed as an endorsement. No brands or products mentioned are affiliated with SoFi, nor do they endorse or sponsor this content.

Communication of SoFi Wealth LLC an SEC Registered Investment Advisor

SoFi isn’t recommending and is not affiliated with the brands or companies displayed. Brands displayed neither endorse or sponsor this article. Third party trademarks and service marks referenced are property of their respective owners.

Communication of SoFi Wealth LLC an SEC Registered Investment Adviser. Information about SoFi Wealth’s advisory operations, services, and fees is set forth in SoFi Wealth’s current Form ADV Part 2 (Brochure), a copy of which is available upon request and at www.adviserinfo.sec.gov. Liz Young is a Registered Representative of SoFi Securities and Investment Advisor Representative of SoFi Wealth. Her ADV 2B is available at www.sofi.com/legal/adv.

More from MediaFeed:

The best practices for investing in stocks

To make money in the stock market, you need to give your investments time to compound interest and appreciate in value, as well as make sure to diversify your holdings and invest on a regular cadence.

This article covers everything you need to know about how money is earned by purchasing stock market holdings, and what you can do to maximize the gains you make.

Related:

DepositPhotos.com

The way the stock market works — and works for you — is as simple as a high school economics class. It’s all about supply and demand, and the way those factors affect value. Investors purchase market assets like stocks (shares of companies), which increase in value when the company does well. As the company in question makes financial progress, more investors want a piece of the action, and they’re willing to pay more for an individual share.

That means that the share you paid for has now increased in price, thanks to higher demand — which in turn means you can earn something when it comes time to sell it. (Of course, it’s also possible for stocks and other market holdings to decrease in value, which is why there’s no such thing as a risk-free investment.) Historically, the average rate or return for the stock market has hovered around 10%.

Along with the profit you can make by selling stocks, you can also earn shareholder dividends, or portions of the company’s earnings. Cash dividends are usually paid on a quarterly basis, but you might also earn dividends in the form of additional shares of stock.

You likely won’t see serious growth without heeding some basic market principles and best practices. Here’s how to ensure your portfolio will do as much work for you as possible.

DepositPhotos.com

Although it’s possible to make money on the stock market in the short term, the real earning potential comes from the compound interest you earn on long-term holdings. As your assets increase in value, the total amount of money in your account grows, making room for even more capital gains. That’s how stock market earnings increase over time exponentially.

But in order to best take advantage of that exponential growth, you need to start building your portfolio as early as possible. Ideally, you’ll want to start investing as soon as you’re earning an income — perhaps by taking advantage of a company-sponsored 401(k) plan.

To see exactly how much time can affect your nest egg, let’s look at an example.

Say you stashed $1,000 in your retirement account at age 20, with plans to hang up your working hat at age 70. Even if you put nothing else into the account, you’d have over $18,000 to look forward to after 50 years of growth, assuming a relatively modest 6% rate of return. But if you waited until you were 60 to make that initial deposit, you’d earn less than $800 through compounding — which is why it’s so much harder to save for retirement if you don’t start early. Plus, all that extra cash comes at no additional effort on your part.

nortonrsx

Time is an important component of your overall portfolio growth. But even decades of compounding returns can only do so much if you don’t continue to save.

Let’s go back to our retirement example above — only this time, instead of making a $1,000 deposit and forgetting about it, let’s say you contributed $1,000 a year (this comes out to less than $20 per week).

If you started making those annual contributions at age 20, you’d have saved about $325,000 by the time you celebrated your 70th birthday. Even if you waited until 60 to start saving, you’d wind up with about $15,000 — a far cry from the measly $1,800 you’d take out if you only made the initial deposit.

Making regular contributions doesn’t have to take much effort; you can easily automate the process through your 401(k) or brokerage account, depositing a set amount each week or pay period.

1989_s/ istockphoto

If you’re looking to see healthy returns on your stock market investments, just remember — you’re playing the long game.

For one thing, short-term trading lacks the tax benefits you can glean from holding onto your investments for longer. If you sell a stock before owning it for a full year, you’ll pay a higher tax rate than you would on long-term capital gains — that is, stocks you’ve held for more than a year.

While there are certain situations that do call for taking a look at your holdings, for the most part, even serious market dips reverse themselves in time. In fact, these bearish blips are regular, expected events, according to Malik S. Lee, certified financial planner and founder of Atlanta-based Felton & Peel Wealth Management.

So-called market corrections are healthy, he said, not that “it shows that the market is alive and well.” And even taking major recessions into account, the market’s performance has had an overall upward trend over the past hundred years.

ipopba/ istockphoto

All investing carries risk — it’s possible for some of the companies you invest in to underperform, or even fold entirely. But if you diversify your portfolio, you’ll be safeguarded against losing all of your assets when investments don’t go as planned.

By ensuring you’re invested in many different types of securities, you’ll be better prepared to weather stock market corrections. It’s unlikely that all industries and companies will suffer equally or succeed at the same level, so you can hedge your bets by buying some of everything.

utah778/ istockphoto

Although the internet makes it relatively easy to create a well-researched DIY stock portfolio, if you’re still hesitant to put your money in the market, hiring an investment advisor can help. Even though the use of a professional can’t mitigate all risk of losses, you might feel more comfortable knowing you have an expert in your corner.

If you’re looking for an expert to specifically help with your investments, it could be worth considering a financial advisor. Financial advisors focus on providing personalized advice on your investment portfolio, typically for a fee based on a percentage of assets under management.

Another lower-cost way to get a little guidance on investing is to use a robo-advisor. This can help you build a diversified portfolio and rebalance it when needed, often for a lower fee than a traditional financial advisor — though, of course, this service is digitally based, rather than provided through a human relationship.

Kerkez/istockphoto

DepositPhotos.com

One of the most common mistakes that investors make is letting their emotions derail their long-term plans, by buying or selling stock based on movement in the market. However, as we noted earlier, investing in the stock market is a marathon, not a sprint. While it might be hard to sit tight when the market is plummeting, keep in mind that the stock market has always recovered from downturns.

Acting on emotion and buying or selling stock based on movement in the market — or trying to time the market — is not a solid investing strategy. Instead, try dollar-cost-averaging, which is when you invest your money evenly and routinely over a longer period of time.

DepositPhotos.com

Snapping up the buzziest new IPO might be tempting, and it can certainly make investing feel exciting. However, experts generally recommend against picking and choosing individual stocks to invest in — not to mention you should generally try to leave your emotions out of the equation.

As we mentioned earlier in this article, you should maintain a diversified portfolio, and that doesn’t include just the latest and greatest new stocks. To do this, a better bet might be to consider index funds, which are made up of a well-diversified mix of stocks and bonds that replicate the makeup of an underlying index.

This can be a simple and low-cost way to invest in a diversified mix of assets, as opposed to just cherry-picking individual stocks. This will ensure that you’re not overexposing yourself to any one area, and thus taking on too much risk.

gopixa / istockphoto

Another major mistake that new investors can make is not respecting their risk tolerance, and either taking on too much or too little risk. Your risk tolerance is based on an array of factors, like your time horizon and personal comfort level, and it should be the basis for the asset allocation of your portfolio.

If you take on too much risk, you can face big losses or be forced to cash out of the market too soon. On the other hand, play it too safe, and you can miss out on compounding gains. A key to making money from the stock market is figuring out your risk tolerance, and then abiding by it.

This article originally appeared on MagnifyMoney.com and was syndicated by MediaFeed.org.

Fokusiert/ istockphoto

Featured Image Credit: ArtistGNDphotography/istockphoto.