Splitsville

This may be one of the more short-term oriented posts I’ll write, but we’re in an era of short attention spans and a market walk that is measured in weeks, not quarters. Gotta give the people what they want.

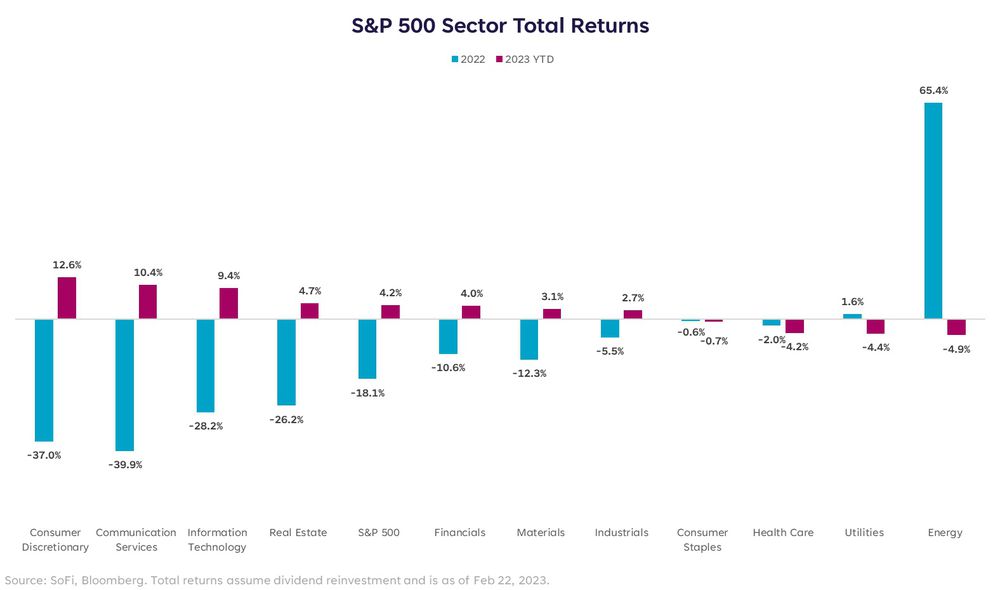

The rip-your-face-off rally that started in January was one that saw high beta and high growth stocks (in other words, everything that didn’t work in 2022) bounce back in spectacular fashion. The chart below shows the dispersion in returns among sectors YTD vs. their 2022 performance. The trends split apart quite starkly with last year’s biggest losers becoming this year’s biggest winners.

There are a number of different ways this move has been explained. Some say it’s the beginning of a new bull market and the drawdown of 2022 was the repricing we needed to digest higher rates and tighter financial conditions. Some say this is a rotation back into parts of the market that were hit disproportionately hard by economic growth fears and are rebounding because things aren’t as bad as expected. Lastly, some say this rally was due to Treasury yields falling and financial conditions easing, which allowed investors to pile back into risky assets.

My thoughts align with the last group, and I’ll add that although our economy is much more dependent on technology and services today, cyclical indicators still matter and the rally didn’t quiet those warning bells.

Up, Up and…No Way

I’m not one to disagree with the market all the time. We’ve heard the argument “don’t fight the tape” a lot lately, and I recognize that it’s a thing. However, it can be very instructive to slice and dice market action into pieces and study the behaviors among certain asset classes.

One relationship we look at is that between cyclical stocks and the 10-year Treasury yield. We used the Goldman Sachs cyclicals vs. defensives index, which splits the S&P 500 into stocks that are more sensitive to GDP growth (cyclical) or less sensitive (defensive) to gauge market direction. As the line moves up, cyclicals are performing better. As it moves down, defensives are performing better.

The other line on this chart is the 10-year Treasury yield. Oftentimes, if the 10-year Treasury yield is rising, it indicates less fear in the market and an expectation for stronger GDP growth in quarters to come. On the contrary, if it’s falling it generally means investors are worried about growth and are buying protection in the form of long-term Treasuries.

This relationship has tracked pretty tightly for decades. In periods where yields fell, growth was underwhelming, and cyclicals trended downward. The most interesting part of the chart is what’s happened since the end of 2021: the relationship completely decoupled. The two entered splitsville as if to say, “it’s not you, it’s me,” “I think we should see other lines,” “you’ve changed.”

But why, and what does it mean? To me, it means despite a meteoric rise in 10-year yields, the cyclical parts of the market know that rates aren’t up because growth prospects are up. They’re up because inflation is up, the Fed is in fight not flight, and that at some point this may not end well.

Here is where I won’t fight the market at all. I think that blue line is right as rain and sniffing out that a short-term rally does not change the fact that economic growth could have a tough road ahead.

We Are on a Break

The key to any successful relationship is compromise, some form of meeting in the middle. These indicators that have entered splitsville likely need to find some common ground in the months ahead. What I think we’ve just witnessed was the high-beta parts of the market on a bender, out in life and wildin’ to exercise their freedom. The difficult part is knowing which side needs to give more back. And that’s where we sit right now, on the precipice of some retracement — either in yields, or in stock multiples — because while this relationship is likely on a break, it’s not breaking up for good.

Learn More:

This article originally appeared on SoFi.com and was syndicated by MediaFeed.org.

Please understand that this information provided is general in nature and shouldn’t be construed as a recommendation or solicitation of any products offered by SoFi’s affiliates and subsidiaries. In addition, this information is by no means meant to provide investment or financial advice, nor is it intended to serve as the basis for any investment decision or recommendation to buy or sell any asset. Keep in mind that investing involves risk, and past performance of an asset never guarantees future results or returns. It’s important for investors to consider their specific financial needs, goals, and risk profile before making an investment decision.

The information and analysis provided through hyperlinks to third party websites, while believed to be accurate, cannot be guaranteed by SoFi. These links are provided for informational purposes and should not be viewed as an endorsement. No brands or products mentioned are affiliated with SoFi, nor do they endorse or sponsor this content.

Communication of SoFi Wealth LLC an SEC Registered Investment Advisor

SoFi isn’t recommending and is not affiliated with the brands or companies displayed. Brands displayed neither endorse or sponsor this article. Third party trademarks and service marks referenced are property of their respective owners.

Communication of SoFi Wealth LLC an SEC Registered Investment Adviser. Information about SoFi Wealth’s advisory operations, services, and fees is set forth in SoFi Wealth’s current Form ADV Part 2 (Brochure), a copy of which is available upon request and at www.adviserinfo.sec.gov. Liz Young is a Registered Representative of SoFi Securities and Investment Advisor Representative of SoFi Wealth. Her ADV 2B is available at www.sofi.com/legal/adv.

More from MediaFeed:

9 smart investments to hedge against inflation

It’s no secret that inflation has arrived and is here to stay. To protect yourself from the adverse effects of inflation, it’s essential to invest your money in smart ways.

fizkes / iStock

A few things can cause inflation, but the most common is when the government prints more money than there is demand for. Printing more money causes the value of each dollar to go down, and it becomes more expensive to buy goods and services.

CasPhotography/istock

Inflation can have a lot of adverse effects on the economy. When the value of money goes down, people tend to hold onto their cash instead of spending it.

Not spending money can lead to a decrease in demand, which can cause businesses to lay off workers or even go out of business.

Yingko/istock

Inflation can also affect asset values. A decrease in the value of money can lead to a decrease in the value of these assets. For example, when the value of money goes down, it can be more expensive to buy stocks and other investments.

marchmeena29 / istockphoto

There are a few things you can do to protect yourself from inflation. One is to invest your money in assets that will maintain their value over time. Another is to keep up with current events and make sure you know how inflation affects the economy. Finally, make sure you’re not taking on too much debt, as inflation affects this.

Here are nine investments that can help you protect your savings from inflation.

fotopoly/istock

TIPS, or Treasury Inflation-Protected Securities, are a type of bond issued by the U.S. government. The value of these bonds increases as inflation rises, so they can be a great way to protect your money from the harmful effects of inflation.

The downside of investing in TIPS is that they tend to have a low yield, so that you won’t earn a lot of money on your investment. However, the security of knowing your investment is protected from inflation makes them a wise choice for anyone looking to shield their money from rising prices.

Depositphotos

Bonds are another investment that can help you protect yourself from inflation.

Bonds can be a great way to make sure your money is safe and will maintain its value even if inflation rises. When you buy a bond, you’re lending money to a government or company in exchange for regular interest payments over a set period of time.

The downside of investing in bonds is that they can be risky if the company or government you’ve lent money to goes bankrupt. So, it’s essential to do your research before investing in bonds and know exactly to whom you’re lending money.

DepositPhotos.com

Gold is a popular investment during times of inflation, as it tends to hold its value even when the dollar falls. The preservation of its value makes gold an excellent option for anyone looking to protect their money from price fluctuations.

The downside of investing in gold is that it can be expensive, and there’s no guarantee that the price will go up over time. So, it’s essential to do your research before buying gold and make sure you’re comfortable with the risks involved.

DepositPhotos.com

Real estate is another asset that often performs well during times of inflation. When prices rise, people tend to invest in real estate to earn a higher return on their investment. The earning potential can make real estate a wise choice for anyone looking to shield their money from inflation.

The downside of investing in real estate is that it can be risky, and it can take a long time to see a return on your investment. So, it’s essential to do your research before buying property and make sure you’re comfortable with the risks involved.

DepositPhotos.com

Commodities are items like gold, silver, oil and wheat used as investments during times of inflation. They are used as investments because they tend to hold their value even when the dollar falls.

The downside of investing in commodities is that they can be volatile, and it’s difficult to predict how prices will change over time. So, it’s essential to do your research before buying commodities and make sure you’re comfortable with the risks involved.

NiseriN / iStock

Mutual funds are a type of investment that allows you to invest in various assets, including stocks, bonds, and commodities. Mutual funds can be a great way to spread your risk and protect your money from the adverse effects of inflation.

The downside of investing in mutual funds is that they can be expensive, and it can take a while to see a return on your investment. So, it’s essential to do your research before buying into a mutual fund and make sure you’re comfortable with the risks involved.

DepositPhotos.com

Stocks are another option for protecting yourself from inflation. When you buy stocks, you’re investing in shares of a company. Investing in these shares means that you become part-owner of the company and stand to earn dividends if the company does well.

The downside of investing in stocks is that they can be risky, and it’s difficult to predict how prices will change over time. So, it’s essential to do your research before buying into stock and make sure you’re comfortable with the risks involved.

Pinkypills / istockphoto

Silver is a type of commodity that often performs well during times of inflation. Silver performs well because it tends to hold its value even when the dollar falls.

The downside of investing in silver is that it can be volatile, and it’s difficult to predict how prices will change over time. So, it’s essential to do your research before buying into silver and make sure you’re comfortable with the risks involved.

alexis84 / istockphoto

Floating-rate bonds are a type of bond that has a variable interest rate. Having a variable interest rate means that the interest rate will change depending on how the economy is doing.

The upside of investing in floating-rate bonds is that they offer a higher return than regular bonds and are less risky than stocks or commodities.

The downside of investing in floating-rate bonds is that they can be volatile, and it’s difficult to predict how prices will change over time. So, it’s essential to do your research before buying into a floating-rate bond and make sure you’re comfortable with the risks involved.

JJ Gouin / istockphoto

Inflation can be a severe threat to your financial security. However, by investing in the right assets, you can protect yourself from its adverse effects. So, before you invest your money, make sure you understand how inflation can impact your portfolio and choose investments that will help you stay ahead of the curve.

This article originally appeared on MaxMyMoney.org and was syndicated by MediaFeed.org.

Kerkez/istockphoto

Deposit Photos

Featured Image Credit: AndreyPopov/istockphoto.