Globetrotting

There’s been a decent amount of chatter lately about international economies, markets, and all of the possible effects they could have on U.S. markets. There’s been much less chatter about whether or not international markets deserve a closer look, regardless of how U.S. markets may react to certain risks and possibilities that lie outside our borders.

A deep dive into the intricacies and geopolitical forces at play is beyond the scope of this piece, but we can take a look at some of the metrics we use to gauge the attractiveness of U.S. markets, to compare from a high level perspective.

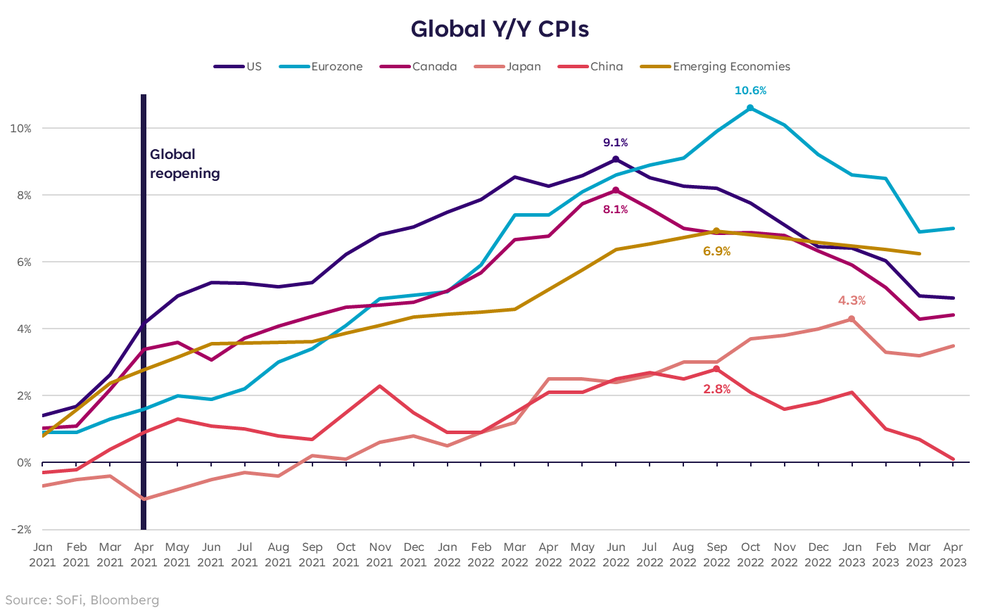

For starters, no analysis in this environment can be done without considering the state of inflation. We’re much more familiar with the Fed’s goals of 2% inflation and maximum employment, but Central Banks around the globe have similar (if not identical) targets and are grappling, in many cases, with inflation that’s even more pesky than ours.

Perhaps it’s not a surprise that everyone is dealing with an inflation problem after the Covid global supply-chain shock, and subsequent tidal wave of demand, but what’s important to take away from the chart above is that large regions like Europe are an unfortunate example of sticky and persistent inflation. Even in the face of weak growth (Euro-zone real GDP growth has been below 1% q/q since Q4 2021) and bruised demand, inflation is still 7% in aggregate.

In fact, four of the five regions on this chart have seen a recent uptick or flat move in inflation recently. We’ve certainly made meaningful progress since peak inflation last summer, but aside from China, the fight isn’t over. Which likely means either more liquidity constriction to come, or at the very least, lagged effects of monetary tightening that haven’t quite rippled through yet.

Earn Your Keep

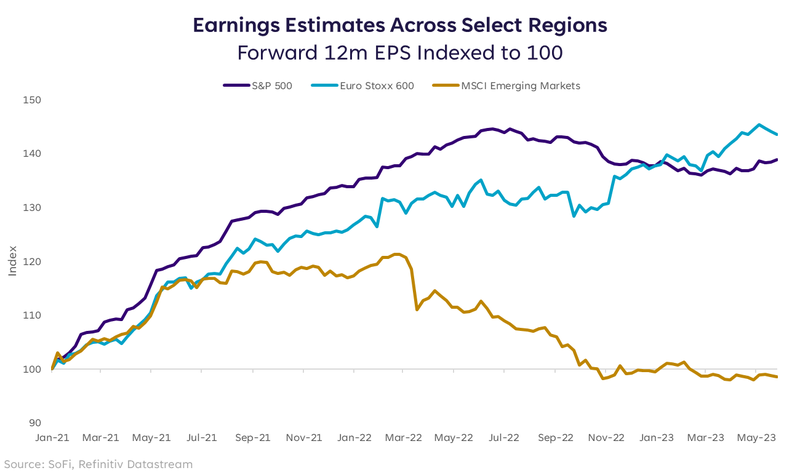

Inflation aside, what should matter to stock market direction is earnings. We know that S&P 500 forward EPS estimates have come down considerably since last summer, but companies have managed to hang in there perhaps better than expected. There’s still a risk for estimates to come down further, but they seem to have leveled out for the time being.

A read on European forward EPS actually looks attractive on a relative basis, with estimates rising over the same period, only showing a downtick recently. The difficult part of this picture is that we can’t tell whether European earnings are in fact more durable, or if the downward revisions have only just begun.

Given the stagflationary environment and persistent inflation problem, my hunch is that European earnings have room to fall. Not to mention, many European companies rely on U.S. and emerging market consumers to drive revenue, and if that consumption pattern doesn’t pick up, margins are likely to compress.

Speaking of emerging markets, earnings expectations for the broad EM index are underwhelming at best, and have seen a major downward revision cycle since spring of 2022. There are undoubtedly more risks embedded in EM countries, and more currency and market volatility, but the contrarian in me actually looks at the EM earnings line as a possibility that expectations are in a bottoming phase.

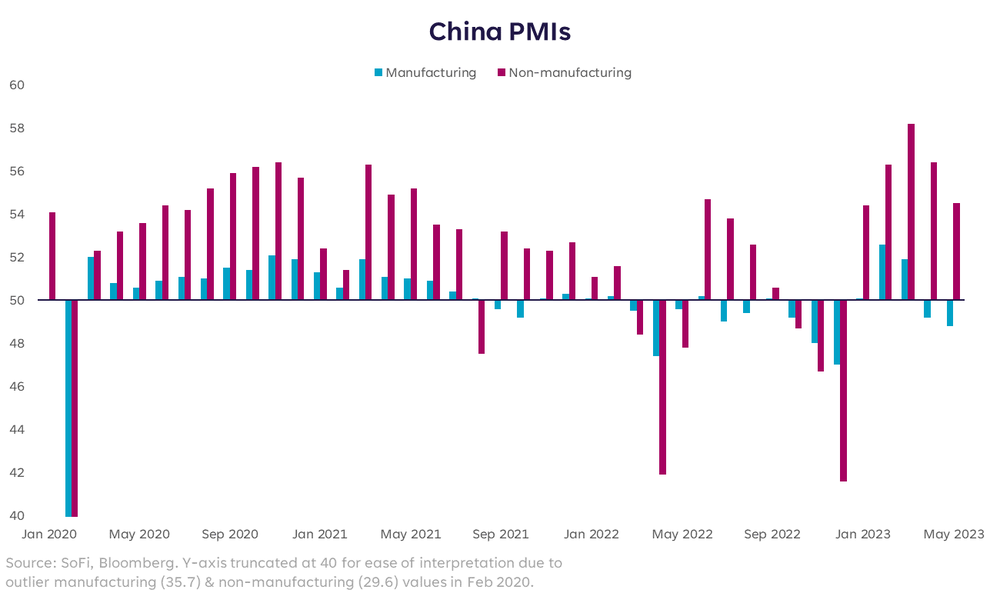

Being choosy about EM exposure remains critical. Geopolitical tensions between China and the U.S. and Taiwan should give investors pause. Additionally, China’s disappointing growth since fully reopening hasn’t proven to be the savior of a slowing consumer elsewhere. As such, a read of China’s economic activity is showing a decided contraction in the manufacturing sector, and if new lockdowns should occur, non-manufacturing sectors are likely at risk.

Needles in Haystacks

All right, maybe this read on international markets wasn’t exactly a pep talk of epic proportions. And maybe the U.S., although not without its challenges and high current valuations, still appears more attractive comparatively.

The point is that after many, many years of international indexes underperforming the U.S., it’s always worth revisiting to see if the tides could finally be shifting. Also, as a long-term investor, geographic diversification is an important element of portfolio construction.

At the current moment, international markets do not appear incredibly attractive on a broad index level, but I am starting to think about the pockets of opportunity in emerging markets. If the U.S. dollar weakens further, and if the possibility that EM earnings have bottomed becomes more of a reality, they’re probably worth a look. But be wary of too much exposure to China, which can be tricky in EM, given China’s monstrous weight in most indexes.

I’ll revisit this topic as time goes on, for now it’s probably just worth planting a seed and watching how it develops. The simple notion that there could be money to be made outside our borders is one we haven’t spent much time considering lately, but we could benefit from casting a wider net at some point in the not-too-distant future.

This article originally appeared on SoFi.com and was syndicated by MediaFeed.org.

Please understand that this information provided is general in nature and shouldn’t be construed as a recommendation or solicitation of any products offered by SoFi’s affiliates and subsidiaries. In addition, this information is by no means meant to provide investment or financial advice, nor is it intended to serve as the basis for any investment decision or recommendation to buy or sell any asset. Keep in mind that investing involves risk, and past performance of an asset never guarantees future results or returns. It’s important for investors to consider their specific financial needs, goals, and risk profile before making an investment decision.

The information and analysis provided through hyperlinks to third party websites, while believed to be accurate, cannot be guaranteed by SoFi. These links are provided for informational purposes and should not be viewed as an endorsement. No brands or products mentioned are affiliated with SoFi, nor do they endorse or sponsor this content.

Communication of SoFi Wealth LLC an SEC Registered Investment Advisor

SoFi isn’t recommending and is not affiliated with the brands or companies displayed. Brands displayed neither endorse or sponsor this article. Third party trademarks and service marks referenced are property of their respective owners.

Communication of SoFi Wealth LLC an SEC Registered Investment Adviser. Information about SoFi Wealth’s advisory operations, services, and fees is set forth in SoFi Wealth’s current Form ADV Part 2 (Brochure), a copy of which is available upon request and at www.adviserinfo.sec.gov. Liz Young is a Registered Representative of SoFi Securities and Investment Advisor Representative of SoFi Wealth. Her ADV 2B is available at www.sofi.com/legal/adv.

Help! Inflation is killing my budget. How can I fight back?

Saving money during a time of high inflation may seem like a contradiction in terms. If you’re like most people, you feel like you’re spending every dollar to meet the higher costs of groceries, gas, utilities, and just about every other expense. Savings, not surprisingly, can seem to take a back seat.

But continuing to save during times of inflation — and saving your money in places that can help protect you from inflation’s damaging effects — is more important than ever. You don’t want this culprit upending your current lifestyle or long-term goals.

The following guide can offer ways to help you with how to save money during inflation. We have come up with four strategies to help combat inflation, followed by three places to consider putting your money during this stressful period.

nicoletaionescu / iStock

Inflation is a rise in prices across the economy. It is also defined as a decline in purchasing power over time. That’s because the rise in prices, often expressed as a percentage, means your dollars buy a lot less than they did earlier. Currently, you need only look at the price of bread, milk, or a gallon of gas to see what the economists mean when they’re talking about rising prices.

In the U.S., the government and economic forecasters measure inflation by a rise in the Consumer Price Index (CPI), Producer Price Index (PPI), and the Personal Consumption Expenditures Price Index (PCE). All of these measures basically track rising prices across the economy. Prices may rise because of an increase in the cost of raw goods, supply chain problems, energy price rises, shifts in consumer spending, rapid wage growth, and a host of other reasons.

A little bit of inflation is good. Indeed, the Federal Reserve sets a 2% annual inflation rate as its goal. This is because a small amount of inflation encourages consumers to spend and invest rather than keep their money under the mattress. That said, when inflation rises too much or too quickly, consumers and the economy suffer.

For the past 25 years or so, the U.S. has had low inflation, rarely rising above 3%. That’s why when the Consumer Price Index hit 8.6% in May 2022, consumers and economists were shocked.

In November, price rises slowed a bit. As of January 2023, the inflation rate was at 6.5%. However, inflation is expected to remain a concern with consumers for 2023.

Khanchit Khirisutchalual/istockphoto

The impacts of high inflation are felt most immediately in our pocketbooks in the form of higher prices for just about everything, including daily essentials. But high inflation has several other consequences. Here’s a look:

Consumer Confidence Erodes

As mentioned above, purchasing power gets cut short when prices rise. Because much of the U.S. economy is based on consumer confidence and buying power, the economy can shrink in the face of high inflation and, depending on other factors, even hit a recession. A retrenching economy can lead to investors to lose confidence as well, causing volatility in the markets.

Interest Rates Rise

The Federal Reserve is committed to keeping a low inflation rate. The main tool it uses to battle inflation is to raise interest rates.

Rising rates mean the cost of borrowing increases, often cooling spending and the economy, bringing prices down. At the same time, rates on short-term savings such as savings accounts and certificates of deposit (CDs) often increase as financial institutions increase their interest rates in the aftermath of Fed increases. We’ll talk more about that below.

More Expensive Borrowing Costs

Rising rates mean consumers pay more in interest for mortgages, car loans, credit card bills, and other lending. This has a chilling effect on consumer spending, thus slowing the economy. Businesses hit with higher borrowing rates may be less likely to invest for the future, dampening employment and earnings growth and, in turn, consumer spending. This cooling effect on the economy is meant to help lower inflation.

With lower consumer demand for goods and services, prices usually fall. It may already be working. The Fed’s aggressive interest rate increases could be part of the reason inflation declined in December.

Erosion of Your Long-term Savings

Inflation is often talked about as the enemy of retirees. The thinking is retirees may be on a fixed income, and a higher percentage of their principal may be safely socked away in low-return but reliable investments such as bonds and cash. That works fine in the low inflation environment we’ve been experiencing for decades. But investors of all ages, including retirees, need to outpace inflation’s erosion of purchasing power now and in the future. That means they need returns on their savings and investments that beat inflation rates.

With the current 6.5% inflation rate, that’s hard to do and may entail investing in more volatile investments such as high growth stocks.

Eleganza/istockphoto

How to save money during inflation? These four strategies can help you combat inflation and protect against its damaging effects on your budget, spending power, and overall finances.

The adage “pay yourself first” is even more apt during times of high inflation. It’s tempting to stop saving to help pay for rising costs, but don’t. Even if you have to lower your savings goals, make sure you continue to budget yourself for some kind of savings every paycheck. Then be sure to automatically deposit that amount in a separate account, so it doesn’t get sucked up by ever-increasing expenses.

Suwanmanee99 / istockphoto

Higher prices for all sorts of everyday expenses can upend even the most rigorous budgets and take away from your savings. Reviewing your budget regularly during high inflation can help you understand exactly where price increases are hitting you hardest and where you can cut back.

Two areas of consumer spending that are facing the highest price increases are food and energy. These are both good places to revisit your spending patterns and see where you can find some savings.

For food, can you buy generic brands, or start using store loyalty programs that can save you money? Or maybe now’s the time to join one of the warehouse member stores so you can buy in bulk and save.

Some of those retailers also help you save on gas with price discounts for members. Along the same lines, try to use a credit card that offers high cash back rates on gas.

And now’s the time to revisit utility bills. Simple moves like dialing the thermostat down just a few degrees or making sure lights, appliances, and electronics are off when you aren’t home can help cut your energy use. And, take a look at your cable, internet provider, and cell phone bills. Have incremental services added up that could be cut back? Sometimes it’s worth a call to your providers to ask if there are better deals out there for consumers feeling strapped.

Samsclub.com

When you review your budget, take a look at discretionary spending. Can you find just 5% in cuts? Are there streaming services on your credit card bill that you never use anymore? We’ve all been excited to get back to restaurants and live entertainment in the wake of COVID, but can some of that exuberance be curbed a bit now? Entertainment and travel prices have had dramatic increases too, so it might be wise to postpone that theater subscription or European vacation until the frothiness subsides.

damircudic/istockphoto

Credit card debt has risen dramatically in recent months partly because consumers are using credit to fill the gap in their budgets caused by higher prices. This is happening just as interest rates on many credit cards are rising.

Try your best to avoid credit card debt, perhaps using some of the cost-cutting tips mentioned above. The higher balances, especially at higher interest rates may get in the way of your future savings goals once this inflationary environment calms down.

When it comes to other debt, be sure to take a close look at how much a mortgage, auto loan, or other type of loan will cost you over the long run. Payments are bound to be higher than you might expect because of today’s higher interest rates. And be sure to check your credit score and credit reports carefully. By building your credit rating, you increase your chances of getting the lowest possible rates on all types of lending.

DepositPhotos.com

Where to put money during inflation? When prices, and in turn, interest rates, are rising, some investments are better suited to fighting inflation than others. Let’s take a look.

jetcityimage/istockphoto

Many financial institutions, especially online banks, have raised the rates on their savings accounts in the aftermath of the Fed’s increases — but many have not. It may be worth it to compare rates, especially at online banks that tend to offer the highest rates with what you’re earning now. Higher returns can help your savings grow and help offset inflation.

DepositPhotos.com

Savings bonds aren’t necessarily known for high interest rates, but a Series I bond earns both a fixed rate of interest and a rate that changes with inflation. Twice a year the Treasury Department sets the inflation adjusted rate for the next 6 months. I bonds mature in 30 years, but you don’t have to hang onto them for that long. You must hold them for at least a year and if you redeem them after less than five years, you forfeit the previous three month’s interest.

You can buy I bonds through TreasuryDirect.gov for a minimum investment of $25 and an annual maximum of $10,000.

jetcityimage / iStock

When wondering where to put money during inflation, the stock market can be scary. The markets often react negatively to rising inflation, and any subsequent interest rate jumps. Long-term bond prices often decline when interest rates rise. And while stocks can often be an excellent long-term hedge against inflation, in the short term, you often see plenty of volatility.

As a result, you may want to revisit your asset allocation for long-term savings and investments to make sure your portfolio is protected against short-term volatility and the negative long-term effects of long periods of inflation. The good news: You may be able to take advantage of buying opportunities during the volatile periods, making your portfolio better positioned for any future upturns.

DepositPhotos.com

Learning how to budget during inflation, saving money during inflation, and knowing where to put your money during inflation are all challenges consumers are facing right now. Doing your best to keep at least a little bit of savings going, figuring out where you can cut spending to keep your budget intact, and understanding the best savings accounts and investments to help ward off inflation’s impacts are the key things consumers need to do to deal with high inflation.

Learn More:

This article originally appeared on SoFi.com and was syndicated by MediaFeed.org.

Please understand that this information provided is general in nature and shouldn’t be construed as a recommendation or solicitation of any products offered by SoFi’s affiliates and subsidiaries. In addition, this information is by no means meant to provide investment or financial advice, nor is it intended to serve as the basis for any investment decision or recommendation to buy or sell any asset. Keep in mind that investing involves risk, and past performance of an asset never guarantees future results or returns. It’s important for investors to consider their specific financial needs, goals, and risk profile before making an investment decision.

The information and analysis provided through hyperlinks to third party websites, while believed to be accurate, cannot be guaranteed by SoFi. These links are provided for informational purposes and should not be viewed as an endorsement. No brands or products mentioned are affiliated with SoFi, nor do they endorse or sponsor this content.

Communication of SoFi Wealth LLC an SEC Registered Investment Advisor

SoFi isn’t recommending and is not affiliated with the brands or companies displayed. Brands displayed neither endorse or sponsor this article. Third party trademarks and service marks referenced are property of their respective owners.

Communication of SoFi Wealth LLC an SEC Registered Investment Adviser. Information about SoFi Wealth’s advisory operations, services, and fees is set forth in SoFi Wealth’s current Form ADV Part 2 (Brochure), a copy of which is available upon request and at www.adviserinfo.sec.gov. Liz Young is a Registered Representative of SoFi Securities and Investment Advisor Representative of SoFi Wealth. Her ADV 2B is available at www.sofi.com/legal/adv.

Ridofranz/istockphoto

NoSystem images/istockphoto

Featured Image Credit: Igor Kutyaev/istockphoto.