If you need financing to cover a large expense or consolidate debt, taking out a $50,000 personal loan is an option you might want to explore. But there is some information you’ll want to be aware of beforehand, including the eligibility requirements for borrowing a large sum.

Read on to learn everything you need to know about getting a $50,000 personal loan, including the pros and cons of personal loans, how to apply for a $50,000 personal loan, how to find the best option for your situation, and more.

(Learn more: Personal Loan Calculator)

What Is a Personal Loan?

A personal loan is money you borrow from a bank, credit union, or online lender and pay back in regular monthly installments with interest. The money from personal loans can be used for almost any purpose. The interest rate is typically fixed, which means your payments will be the same from month to month.

A personal loan can help you with a major expense you might not be able to pay for otherwise. However, taking out a loan, especially a large amount like $50,000, can be a big responsibility. You will want to weigh your options carefully to make sure it’s the right choice for you.

As you’re exploring personal loans, you can look into the many types of personal loans on the market. The kind you choose can affect your interest rate and loan terms, so it may be helpful to see what’s available.

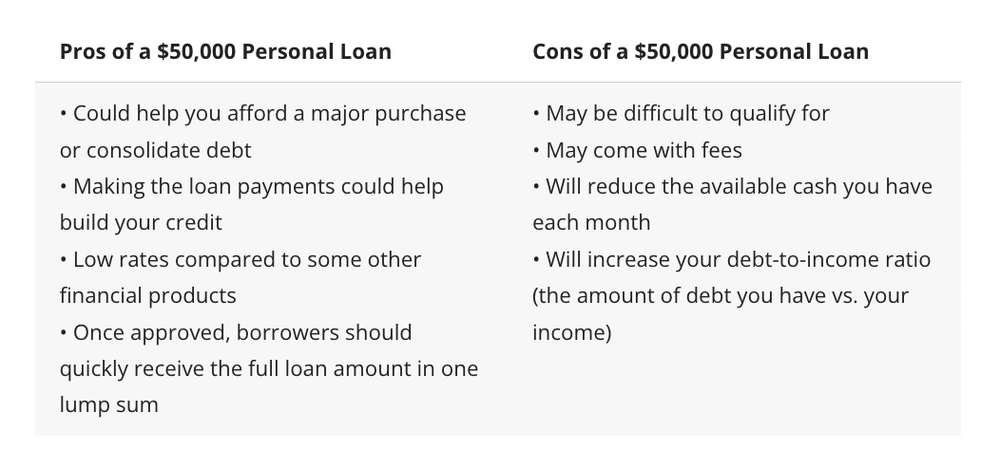

Pros and Cons of $50,000 Personal Loans

There are pros and cons of personal loans every borrower should evaluate before applying. Here are some of the benefits and drawbacks of taking out a 50k personal loan:

Considerations When Looking for $50,000 Personal Loans

As you think about taking out a large personal loan, there are many personal loan offers to explore. These are some of the factors to look into:

Type of Lender

Most borrowers go to a credit union, bank, or online lender for a $50,000 personal loan. The process for how to get large personal loans may be a little different for each lender.

For example, credit unions typically require borrowers to first become members before they can take out a loan. Often, this means paying a one-time membership fee and depositing a small amount into a savings account. If you have an account with a bank, you may want to see what rates and terms they might offer you since you already have a relationship. Online lenders may be able to give you quick funding, and oftentimes the requirements aren’t as stringent.

Interest Rates

Personal loans typically have fixed interest rates, allowing your monthly payments to be consistent. Higher interest rates will add to the cost of the loan, so you’ll want to shop around for the lowest rate.

Fees

Fees vary by lender. Types of fees you will want to compare include:

- Loan origination fees

- Prepayment penalties

- Late fees

The loan origination fee is important because it may affect the loan’s APR (annual percentage rate). It may be added to the loan’s balance instead of being paid upfront, which means you could end up paying interest on it. Alternatively, the origination fee may be deducted from the loan funds before you receive them, in which case you would receive slightly less money than you expected.

Total Repayment Cost

This is the total cost of the loan, including the principal plus interest and fees. The total repayment cost is the amount you will repay. Ask the lender or a loan officer what the total repayment cost is, and be sure to get this information in writing.

Monthly Payment Amount

A loan’s APR and loan term will affect how much you pay each month. For longer loan terms, you’ll pay less each month because the loan balance is spread out over a greater amount of time. However, you’ll pay more in interest because the interest has more time to accrue. A shorter repayment term can lower the amount of interest you’ll pay, reducing the total cost of the loan. Your monthly payments will be higher, though.

What Are the Typical Requirements for a $50k Personal Loan?

Wondering how to qualify for a $50,000 personal loan? Your approval typically depends on the following criteria:

Credit Score

Your credit score is a number that sums up your credit history. Credit score requirements vary by lender. Generally, the higher your credit score, the lower the interest rate you may be able to qualify for. For $50,000 personal loans, lenders might be looking for applicants with a good to excellent credit score.

Credit History

Your credit history includes your track record with paying bills, how much credit you have and what kind, and how much debt you have. Lenders typically want to see that you aren’t overextended with credit or have too much debt. In other words, they want to see that you are responsible in the way you use credit.

Income

Your income helps determine how much you are qualified to borrow. It needs to be enough to cover all your monthly payments — including the cost of a large $50,000 loan. Lenders typically look at your gross (pre-tax) income.

Debt-to-Income Ratio

Your debt-to-income ratio (DTI) is a comparison of the amount of monthly debt you have to your monthly gross income. Lender requirements vary, but a DTI of 36% or lower is considered ideal. You can calculate your DTI by adding your monthly debt payments (mortgage or rent payments, auto loans, student loans, and minimum credit card payments) and dividing that amount by your gross monthly income. Then, multiply the resulting number by 100.

Collateral

It is possible to get an unsecured personal loan that does not require collateral, but with a large $50,000 personal loan, a valuable asset may be needed in order for you to be approved. This is called a secured personal loan. Besides a house or a car, other assets a lender may approve include a boat, antiques, fine art, and jewelry.When you’re using collateral to secure a loan, you may need an appraisal to confirm its value.

Down Payment

If collateral is needed and you don’t have any tangible assets besides cash, the lender may require you to deposit a certain amount of money into an escrow account as a down payment, where it will remain until the loan has matured.

Length of the Loan

Personal loans generally have repayment terms that are between one and five years. With a shorter term, you’ll pay less money for the loan overall, but you’ll pay more each month. A longer term will generally make your monthly payments smaller, but you’ll pay more in interest over the life of the loan.

Cosigner

If you have poor or no credit, lenders may require you to have a cosigner on the loan. The cosigner is typically someone with good credit. Should you be unable to make your payments, the cosigner becomes responsible and will be expected to make the payments.

$50,000 Personal Loans with Bad Credit

It’s possible to get a $50,000 personal loan with bad credit, but it’s more difficult. While there are lenders who work with borrowers with low credit scores, you’ll likely be charged more in interest. Having a creditworthy cosigner could help you secure a loan — and may help you get a better interest rate, as well.

How to Apply for a $50,000 Personal Loan

To apply for a personal loan, you’ll first need to decide if you want to apply with your current bank, a credit union, or an online lender.

Take a look at the qualification requirements and make sure you meet them (or are close to meeting them) prior to applying. If your local bank requires a 700 credit score, for example, and yours is 600, you may want to inquire with a lender that accepts a lower score. You can also consider building your credit score prior to applying.

Next, you’ll want to gather the necessary paperwork, which may include your driver’s license or Social Security number, proof of income, bank account balances, bank statements, your mortgage statement, and more. Typically, lenders will not ask for this information when prequalifying you, but they will eventually want to see these documents before final approval of the loan.

It’s a good idea to prequalify with multiple lenders so you can find the best interest rate and terms for your situation. Since a prequalification does not impact your credit score, you can shop around without running the risk of lowering your score.

Finally, once you’ve made sure you’ve met the requirements, gathered the necessary documents, and comparison shopped multiple lenders, you can apply for the loan. Online lenders tend to get back to you the quickest — oftentimes within one day of submitting your application. Banks and credit unions may take longer, but you may receive a better interest rate than with an online lender.

Questions to Ask Yourself Before Taking Out a Large Personal Loan

What Is This Loan For?

With a $50,000 loan, one of the questions to ask yourself is whether the debt you’re taking on is good debt. Good debt has the potential to increase your net worth in some way. This could include home renovations that increase the value of your house, for example.

Also, consider what you are using the money for and whether a personal loan is the best choice. For instance, if you need funds for a business-related expense, you may want to explore business loans vs. personal loans to see which one makes more sense for your needs.

And while you can use a personal loan for a car purchase, an auto loan may be more advantageous for this purchase because the interest rates may be lower.

How Much Can You Afford as a Monthly Payment?

Before taking out any loan, it’s vital to determine whether you can afford the monthly payments. Considering all of your other debts and expenses, can you comfortably make the monthly payment while also saving for important things like retirement or your child’s college education?

Is the Full Loan Amount Necessary?

Do you need the full $50,000? If you can get by with taking out a smaller loan amount, you might want to consider only borrowing what you need to avoid too much debt and paying more in interest. A $40,000 personal loan, for example, might be sufficient for your needs.

How Will This Affect Your Credit?

When it comes to your credit, one of the most important factors to consider is whether you will be able to comfortably make the monthly payments. Payment history accounts for 35% of your credit score. If you’re not confident you can consistently make the payments on time without stretching your finances thin, you may want to hold off on taking out a loan.

Alternatives to $50k Personal Loans

Although a large personal loan can be helpful when you’re faced with a major expense and need financing quickly, there are other options. These include:

- Home equity line of credit (HELOC): A HELOC uses the equity you’ve built in your home as collateral for a revolving line of credit that you can repeatedly use and pay off. However, if you fail to make the payments, the lender can seize your home.

- Home equity loan: With a home equity loan, you borrow against your home’s equity. It typically has a lower interest rate and a longer repayment term than a personal loan. But again, if you default on the loan, the lender can foreclose on your house.

- Cash-out refinance: A cash-out refinance allows you to refinance your mortgage while borrowing money at the same time, based on the equity you have in your home. The cash-out refinance process entails borrowing a new mortgage for a larger amount than the existing mortgage; you then receive the difference in cash. You will pay closing costs, and you’ll need to have your home appraised. If you don’t make payments, you are at risk of losing your home.

Compare Personal Loan Rates

Taking out a $50,000 personal loan could be helpful for paying a major expense or consolidating debt. While it may be difficult to qualify, you can use the money for virtually any purpose. Just be sure that you can afford to borrow such a large amount and that you can make the monthly payments.

If you decide that a $50,000 personal loan makes sense for you, Lantern by SoFi can help you easily find an option that suits your needs. By filling out one simple form, you can conveniently compare offers from multiple lenders to find the best rates and terms for you.

This article originally appeared on SoFi.comand was syndicated by MediaFeed.org.

Lantern By SoFi

SoFi receives compensation in the event you obtain a loan, financial product, or service through the Lantern marketplace. This Lantern website is owned by SoFi Lending Corp., a lender licensed by the Department of Financial Protection and Innovation under the California Financing Law, license number 6054612; NMLS number 1121636. (nmlsconsumeraccess). This site is NOT owned and operated by SoFi Bank. Loans, financial products, and services may not be available in all states..

(nmlsconsumeraccess). This site is NOT owned and operated by SoFi Bank. Loans, financial products, and services may not be available in all states.

All rates, fees, and terms are presented without guarantee and are subject to change pursuant to each provider’s discretion. There is no guarantee you will be approved or qualify for the advertised rates, fees, or terms presented. The actual terms you may receive depends on the things like benefits requested, your credit score, usage, history and other factors.

*Check your rate: To check the rates and terms you may qualify for, Lantern and/or its network lenders conducts a soft credit pull that will not affect your credit score. However, if you choose a product and continue your application, the lender(s) you choose will request your full credit report from one or more consumer reporting agencies, which is considered a hard credit pull and may affect your credit.

All loan terms, including interest rate, and Annual Percentage Rate (APR), and monthly payments shown on this website are from lenders and are estimates based upon the limited information you provided and are for information purposes only. Estimated APR includes all applicable fees as required under the Truth in Lending Act. The actual loan terms you receive, including APR, will depend on the lender you select, their underwriting criteria, and your personal financial factors. The loan terms and rates presented are provided by the lenders and not by SoFi Lending Corp. or Lantern. Please review each lender’s Terms and Conditions for additional details.

Many factors affect your credit scores and the interest rates you may receive. SoFi is not a Credit Repair Organization as defined under federal or state law, including the Credit Repair Organizations Act. SoFi does not provide “credit repair” services or advice or assistance regarding “rebuilding” or “improving” your credit record, credit history, or credit rating. For details, see the FTC’s website on credit (consumer.ftc.gov)

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.¹

SoFi’s Insights tool offers users the ability to connect both SoFi accounts and external accounts using Plaid, Inc.’s service. When you use the service to connect an account, you authorize SoFi to obtain account information from any external accounts as set forth in SoFi’s Terms of Use. SoFi assumes no responsibility for the timeliness, accuracy, deletion, non-delivery or failure to store any user data, loss of user data, communications, or personalization settings. You shall confirm the accuracy of Plaid data through sources independent of SoFi. The credit score provided to you is a VantageScore® based on TransUnion® (the “Processing Agent”) data.

Personal Loan

SoFi Lending Corp. (“SoFi”) operates this Personal Loan product in cooperation with Engine by MoneyLion. If you submit a loan inquiry, SoFi will deliver your information to Engine by MoneyLion, and Engine by MoneyLion will deliver to its network of lenders/partners to review to determine if you are eligible for pre-qualified or pre-approved offers. The lenders/partners receiving your information will also obtain your credit information from a credit reporting agency. If you meet one or more lender’s and/or partner’s conditions for eligibility, pre-qualified and pre-approved offers from one or more lenders/partners will be presented to you here on the Lantern website. More information about Engine by MoneyLion, the process, and its lenders/partners is described on the loan inquiry form you will reach by visiting our Personal Loans page as well as our Student Loan Refinance page. Click to learn more about Engine’s Licenses and Disclosures, Terms of Service, and Privacy Policy.Personal loan offers provided to customers on Lantern do not exceed 35.99% APR. An example of total amount paid on a personal loan of $10,000 for a term of 36 months at a rate of 10% would be equivalent to $11,616.12 over the 36 month life of the loan.

Student Loan RefinanceSoFi Lending Corp. (“SoFi”) operates this Student Loan Refinance product in cooperation with Engine by MoneyLion. If you submit a loan inquiry, SoFi will deliver your information to Engine by MoneyLion, and Engine by MoneyLion will deliver to its network of lenders/partners to review to determine if you are eligible for pre-qualified or pre-approved offers. The lenders receiving your information will also obtain your credit information from a credit reporting agency. If you meet one or more lender’s and/or partner’s conditions for eligibility, pre-qualified and pre-approved offers from one or more lenders/partners will be presented to you here on the Lantern website. More information about Engine by MoneyLion, the process, and its lenders/partners is described on the loan inquiry form you will reach by visiting our Personal Loans page as well as our Student Loan Refinance page. Click to learn more about Engine’s Licenses and Disclosures, Terms of Service, and Privacy Policy.

NOTICE: The debt ceiling legislation passed on June 2, 2023, codifies into law that federal student loan borrowers will be reentering repayment. The US Department of Education or your student loan servicer, or lender if you have FFEL loans, will notify you directly when your payments will resume For more information, please go to https://docs.house.gov/billsthisweek/20230529/BILLS-118hrPIH-fiscalresponsibility.pdf https://studentaid.gov/announcements-events/covid-19

If you are a federal student loan borrower considering refinancing, you should take into account the new income-driven payment plan, SAVE, which replaces REPAYE, seeks to make monthly payments more affordable, and offers forgiveness of balances that were originally $12,000 or lower after 120 payments, among other improvements. Also, please note that once you refinance federal student loans you will no longer be eligible for current or future flexible payment options available to federal loan borrowers, including but not limited to income-based repayment plans, such as SAVE, or extended repayment plans.

Auto Loan RefinanceAutomobile refinancing loan information presented on this Lantern website is from Caribou, AUTOPAY, Engine by MoneyLion, and each of Engine’s partners (along with their affiliated companies). Caribou, AUTOPAY, and Engine by MoneyLion pay SoFi compensation for marketing their products and services on the Lantern site.

Auto loan refinance information presented on this Lantern site is indicative and subject to you fulfilling the lender’s requirements, including but not limited to: credit standards, loan size, vehicle condition, and odometer reading. Loan rates and terms as presented on this Lantern site are subject to change when you reach the lender and may depend on your creditworthiness, consult with the lender for more details. Additional terms and conditions may apply and all terms may vary by your state of residence.

Secured Lending DisclosureTerms, conditions, state restrictions, and minimum loan amounts apply. Before you apply for a secured loan, we encourage you to carefully consider whether this loan type is the right choice for you. If you can’t make your payments on a secured personal loan, you could end up losing the assets you provided for collateral. Not all applicants will qualify for larger loan amounts or most favorable loan terms. Loan approval and actual loan terms depend on the ability to meet underwriting requirements (including, but not limited to, a responsible credit history, sufficient income after monthly expenses, and availability of collateral) that will vary by lender.

BankingSoFi Lending Corp. (“SoFi”) operates this website in cooperation with Engine by MoneyLion presenting promotions for products and services offered by other banks, lenders, and financial institutions. If you select a promotion above, you will be connected to the website of the company offering the product. The promotions presented on this site are from companies that pay SoFi and Engine by MoneyLion compensation for marketing their products and services. This may affect whether a provider is featured on this site and could affect the order of presentation. Lantern and Engine by MoneyLion do not include all providers in the market or all of their available offerings. Click to learn more about Engine’s Licenses and Disclosures, Terms of Service, and Privacy Policy.

More from MediaFeed:

Holiday budget looking not-so holly jolly? Make sure to check this list of money tips twice

Paying yourself first is a personal finance strategy in which you prioritize saving money before you spend it. Doing so may mean you transfer funds into a savings or investment account before bills, such as housing and loan payments, get taken care of.

By paying yourself first, you can help build wealth and achieve money goals, whether that means accumulating the down payment on a house or being able to pay for your child’s education. It can also be a way to avoid overspending.

If this “pay yourself first” strategy sounds good, read on to learn tips for making it a reality by budgeting well and using tools such as automatic transfers.

It may help to know that plenty of financial planners believe in this approach, as it can help you build a nice nest egg. Here’s a few ways paying yourself first can help you financially.

triocean / iStock

The beauty of this approach is that it focuses on consistent, prioritized savings and investment, along with a frugal mindset, which could give you the freedom to ultimately put your money where it matters most to you.

(Learn more: Personal Loan Calculator)

staticnak1983/istockphoto

Everyone has unique savings and investment goals, and it’s helpful to be clear about your own — then you could use those goals as motivation to consistently pay yourself first.

To get started, it could help to brainstorm how much you’d like to save and what you would do with that money.

You might, for example, want to put a certain amount of money aside for things like a downpayment on a house or to help your children attend college. Or you may want to travel.

RichVintage/istockphoto

Because some of the bigger financial goals may take a while to achieve, it could help to also have shorter-term goals to stay motivated to save.

Your shorter-term goal, for example, might be to put enough away in savings to cover a month’s worth of expenses — and then three months, and then six months. Or you may want to save to buy a new car. Paying yourself first can make meeting those shorter-term goals more doable.

Doucefleur/istockphoto

If saving enough money to meet your goals seems out of reach, then it might help to take an honest look at your spending habits. Maybe you find yourself making impulse purchases when you’re feeling stressed. If so, know that you’re not alone when indulging in some retail therapy.

If you only rarely indulge in impulse shopping, and the dollar amounts are within your means, then this isn’t likely to cause significant harm. But, if this becomes a habit, crossing over into compulsive spending, then this could have a serious impact on your financial well-being. Consider the following:

- If you believe that you’re not achieving savings goals because of overspending, then it could make sense to address that issue first. It might help to identify your emotional triggers and then avoid shopping during those times.

- If you aren’t yet sure what those triggers are, track impulse purchases and reverse engineer when you’re more likely to spend too much. You may notice it happens after a long day at work or when you’re worried about something.

- As another strategy, if you’re not sure whether something fits into your budget, you could wait a couple days before making a buying decision or call a friend when you’re feeling the urge to shop.

- Another potential challenge: FOMO spending — based on the fear of missing out. Many people admit to feeling pressured by others to spend money on purchases they didn’t need, just to keep up with their friends, coworkers, or even influencers on social media.

- If that feels familiar to you, there are strategies to help conquer FOMO spending. You can brainstorm free alternatives to high-cost plans a friend might suggest. When is a local art museum, for example, offering a free community day? What movie can you get from the library and invite friends to watch with you? What about a hike in the local park system?

- If you find that FOMO kicks in when you have your credit or debit card handy, you might want to only carry cash when you go out to your favorite restaurant, bar, or shop. And if ads and posts on social media cause you to want to shop, you could reduce your time on Instagram, Facebook, Twitter, and the like.

- Another strategy: If you’re tempted to put a discretionary purchase on your credit card, you could use a credit card interest calculator to see how much interest you might really pay on that impulse buy. The amount might shock you and cause you to put the item down and walk away.

mediaphotos/istockphoto

Before you can really know how much money you can pay yourself first, you might need to be confident in your budget. Although the word “budget” can have a negative connotation, it’s really a way to take control of your money to make sure you’re saving and spending in a way that meshes with your wants and needs, dreams, and goals.

By tracking your spending for a period of time, say 30 days (or more), you might get a sense of where your money is going. You could create a list of your monthly expenses, including your rent or mortgage payment, car payment, credit card payments, student loan payments, and more.

You might also consider listing what you pay for your utilities, cell phone, groceries, and so forth, along with discretionary purchases, in order to see a more complete picture of monthly costs.

Ideally, when you add these up, you’ll be spending less than what you earn, and you could use that information to help determine how much you can potentially deduct from your paycheck and put into savings or investment accounts.

If you discover that you’re not currently living within your means, or that you aren’t able to save as much as you’d like, then one good idea is to see where you can trim expenses. You may also consider ways to grow your income, whether that means asking for a raise or picking up a side gig.

Based on this information, you can set up a monthly budget. One budget strategy is the 50-30-20 budget. In this budget, you allocate your take-home pay into three categories; needs (50% of your take-home pay), wants (30% of your take-home pay), and savings (20% of your take-home pay). Allocating your money with this budget offers flexibility so that you can save and spend on the things that are most important to you.

damircudic/istockphoto

Let’s look at a few steps you can take to make paying yourself first a priority.

Create an Emergency Savings Account

As a first step in paying yourself first, it may make sense to create an emergency savings account if you don’t already have one or if it needs an extra infusion of cash.

That way, if your car or HVAC system breaks down or you have unexpected medical bills, you’ll have cash to help address the situation without simply relying on high-interest credit cards or other forms of debt.

Conventional wisdom suggests an emergency account that contains three to six months’ worth of basic living expenses, put into an account that’s accessible at any time.

Then you could move on to saving for other short- and long-term goals, including but not limited to saving for retirement.

When trying to determine how much money you should pay yourself first in the beginning, one idea is to start with a small amount and then incrementally increase it until you reach your goals.

Or it might make sense to determine how much you’ll need for your goals and reverse engineer how much you’ll need to put away to reach them in a certain time frame.

Also, if you receive a bonus or inherit money, you could consider putting all of the additional money into a savings or investment account. You could do the same if you get a raise.

designer491/istockphoto

If you are looking to kickstart your savings and build it up fast, there are several strategies you might consider. You may choose to review your expenses and get rid of unnecessary ones.

What online subscriptions and streaming services are you paying for? Are you using them? If you review an entire month’s worth of debits from your account, how many do you see that are discretionary, ones you could live without?

Once you’ve eliminated some expenses, consider adding that combined dollar amount to the money you’re sending directly to your savings account. Even if the amounts, overall, are small, over time they can really add up.

Delmaine Donson/istockphoto

Sometimes, if you owe a monthly payment to a company, they’ll give you a discounted rate if you set up autopay and have your payment automatically deducted from your account. This could help to assure the company that the bill will be paid on the due date. Meanwhile, you could benefit from a discount and the convenience of not having to manually pay the bill each month.

This may help you avoid late fees, as well, but you might want to be cautious. If you don’t have enough money in your account on the day the bill is due to be deducted, you might be charged additional fees, such as an overdraft fee by your bank.

ipopba/istockphoto

Automating your savings can be just as useful as automating your bill pay. Ways to automate your savings include, setting up direct deposit, funneling a set amount to your savings each month, and taking advantage of employer programs like a 401(k) and any employer match offered to employees.

Thai Liang Lim/istockphoto

What about going on a spending fast? You might, for example, pick a day or two of the week when you don’t spend any money outside of what it takes you to get to and from work.

You could also consider other cost-saving ideas like packing your lunch, skipping the stop at the coffee shop, and getting your book from the library on the way home, not from the bookstore. Besides saving you money on your “fasting” days, employing these strategies may help you to pay more attention to discretionary spending on the other days.

ilona titova/istockphoto

Also, you might want to review your bank accounts. Are you getting as much interest as you can, given the wide gap between what different financial institutions pay? Could you earn more interest with your funds in an account at an online bank vs. traditional bank? What fees does your bank charge? Have you shopped around to see if you could get a better deal?

Anchiy/istockphoto

Here’s another strategy you may want to consider as a tool to help with overspending: the 30-day rule. It has two parts and, combined, the rule might help you save money more quickly. In the first half, if you’re tempted to buy anything outside of what’s necessary to meet basic needs, then you write down what you want to buy, how much it costs, where you saw it, and the date.

Then, give yourself 30 days to think about whether you really want to buy this item. If, after 30 days has gone by, you still want to make that purchase, you could price shop it and then buy the item.

As an added twist, take the amount of the item and put those dollars in your savings account. Then, when 30 days have passed, decide whether you’d be happier having more money in your savings or with making this purchase.

If it’s the former, then you have more savings built up. If you still want the item, you could withdraw the money from your savings, rather than putting it on a credit card.

MStudioImages/istockphoto

Paying yourself first is a great way to prioritize saving, especially if you find yourself tempted to make unnecessary purchases often. Taking some time to think about your financial goals, reevaluating your spending habits, and prioritizing your savings, can help you get to a more secure place financially.

Having the ability to track your spending and savings may be one key to help in creating an effective plan to pay yourself first. Reviewing your checking and savings accounts might help you determine if better options are available to boost your financial health.

This article originally appeared on SoFi.com and was syndicated by MediaFeed.org.

SoFi® Checking and Savings is offered through SoFi Bank, N.A. ©2023 SoFi Bank, N.A. All rights reserved. Member FDIC. Equal Housing Lender.

The SoFi Bank Debit Mastercard® is issued by SoFi Bank, N.A., pursuant to license by Mastercard International Incorporated and can be used everywhere Mastercard is accepted. Mastercard is a registered trademark, and the circles design is a trademark of Mastercard International Incorporated.

SoFi members with direct deposit activity can earn 4.60% annual percentage yield (APY) on savings balances (including Vaults) and 0.50% APY on checking balances. Direct Deposit means a deposit to an account holder’s SoFi Checking or Savings account, including payroll, pension, or government payments (e.g., Social Security), made by the account holder’s employer, payroll or benefits provider or government agency (“Direct Deposit”) via the Automated Clearing House (“ACH”) Network during a 30-day Evaluation Period (as defined below). Deposits that are not from an employer or government agency, including but not limited to check deposits, peer-to-peer transfers (e.g., transfers from PayPal, Venmo, etc.), merchant transactions (e.g., transactions from PayPal, Stripe, Square, etc.), and bank ACH funds transfers and wire transfers from external accounts, do not constitute Direct Deposit activity. There is no minimum Direct Deposit amount required to qualify for the stated interest rate.

SoFi members with Qualifying Deposits can earn 4.60% APY on savings balances (including Vaults) and 0.50% APY on checking balances. Qualifying Deposits means one or more deposits that, in the aggregate, are equal to or greater than $5,000 to an account holder’s SoFi Checking and Savings account (“Qualifying Deposits”) during a 30-day Evaluation Period (as defined below). Qualifying Deposits only include those deposits from the following eligible sources: (i) ACH transfers, (ii) inbound wire transfers, (iii) peer-to-peer transfers (i.e., external transfers from PayPal, Venmo, etc. and internal peer-to-peer transfers from a SoFi account belonging to another account holder), (iv) check deposits, (v) instant funding to your SoFi Bank Debit Card, (vi) push payments to your SoFi Bank Debit Card, and (vii) cash deposits. Qualifying Deposits do not include: (i) transfers between an account holder’s Checking account, Savings account, and/or Vaults; (ii) interest payments; (iii) bonuses issued by SoFi Bank or its affiliates; or (iv) credits, reversals, and refunds from SoFi Bank, N.A. (“SoFi Bank”) or from a merchant.

SoFi Bank shall, in its sole discretion, assess each account holder’s Direct Deposit activity and Qualifying Deposits throughout each 30-Day Evaluation Period to determine the applicability of rates and may request additional documentation for verification of eligibility. The 30-Day Evaluation Period refers to the “Start Date” and “End Date” set forth on the APY Details page of your account, which comprises a period of 30 calendar days (the “30-Day Evaluation Period”). You can access the APY Details page at any time by logging into your SoFi account on the SoFi mobile app or SoFi website and selecting either (i) Banking > Savings > Current APY or (ii) Banking > Checking > Current APY. Upon receiving a Direct Deposit or $5,000 in Qualifying Deposits to your account, you will begin earning 4.60% APY on savings balances (including Vaults) and 0.50% on checking balances on or before the following calendar day. You will continue to earn these APYs for (i) the remainder of the current 30-Day Evaluation Period and through the end of the subsequent 30-Day Evaluation Period and (ii) any following 30-day Evaluation Periods during which SoFi Bank determines you to have Direct Deposit activity or $5,000 in Qualifying Deposits without interruption.

SoFi Bank reserves the right to grant a grace period to account holders following a change in Direct Deposit activity or Qualifying Deposits activity before adjusting rates. If SoFi Bank grants you a grace period, the dates for such grace period will be reflected on the APY Details page of your account. If SoFi Bank determines that you did not have Direct Deposit activity or $5,000 in Qualifying Deposits during the current 30-day Evaluation Period and, if applicable, the grace period, then you will begin earning the rates earned by account holders without either Direct Deposit or Qualifying Deposits until you have Direct Deposit activity or $5,000 in Qualifying Deposits in a subsequent 30-Day Evaluation Period. For the avoidance of doubt, an account holder with both Direct Deposit activity and Qualifying Deposits will earn the rates earned by account holders with Direct Deposit.

Members without either Direct Deposit activity or Qualifying Deposits, as determined by SoFi Bank, during a 30-Day Evaluation Period and, if applicable, the grace period, will earn 1.20% APY on savings balances (including Vaults) and 0.50% APY on checking balances.

Interest rates are variable and subject to change at any time. These rates are current as of 10/24/2023. There is no minimum balance requirement. Additional information can be found at SoFi.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

SoFi® Checking and Savings is offered through SoFi Bank, N.A. ©2023 SoFi Bank, N.A. All rights reserved. Member FDIC. Equal Housing Lender.

The SoFi Bank Debit Mastercard® is issued by SoFi Bank, N.A., pursuant to license by Mastercard International Incorporated and can be used everywhere Mastercard is accepted. Mastercard is a registered trademark, and the circles design is a trademark of Mastercard International Incorporated.

SoFi members with direct deposit activity can earn 4.60% annual percentage yield (APY) on savings balances (including Vaults) and 0.50% APY on checking balances. Direct Deposit means a deposit to an account holder’s SoFi Checking or Savings account, including payroll, pension, or government payments (e.g., Social Security), made by the account holder’s employer, payroll or benefits provider or government agency (“Direct Deposit”) via the Automated Clearing House (“ACH”) Network during a 30-day Evaluation Period (as defined below). Deposits that are not from an employer or government agency, including but not limited to check deposits, peer-to-peer transfers (e.g., transfers from PayPal, Venmo, etc.), merchant transactions (e.g., transactions from PayPal, Stripe, Square, etc.), and bank ACH funds transfers and wire transfers from external accounts, do not constitute Direct Deposit activity. There is no minimum Direct Deposit amount required to qualify for the stated interest rate.

SoFi members with Qualifying Deposits can earn 4.60% APY on savings balances (including Vaults) and 0.50% APY on checking balances. Qualifying Deposits means one or more deposits that, in the aggregate, are equal to or greater than $5,000 to an account holder’s SoFi Checking and Savings account (“Qualifying Deposits”) during a 30-day Evaluation Period (as defined below). Qualifying Deposits only include those deposits from the following eligible sources: (i) ACH transfers, (ii) inbound wire transfers, (iii) peer-to-peer transfers (i.e., external transfers from PayPal, Venmo, etc. and internal peer-to-peer transfers from a SoFi account belonging to another account holder), (iv) check deposits, (v) instant funding to your SoFi Bank Debit Card, (vi) push payments to your SoFi Bank Debit Card, and (vii) cash deposits. Qualifying Deposits do not include: (i) transfers between an account holder’s Checking account, Savings account, and/or Vaults; (ii) interest payments; (iii) bonuses issued by SoFi Bank or its affiliates; or (iv) credits, reversals, and refunds from SoFi Bank, N.A. (“SoFi Bank”) or from a merchant.

SoFi Bank shall, in its sole discretion, assess each account holder’s Direct Deposit activity and Qualifying Deposits throughout each 30-Day Evaluation Period to determine the applicability of rates and may request additional documentation for verification of eligibility. The 30-Day Evaluation Period refers to the “Start Date” and “End Date” set forth on the APY Details page of your account, which comprises a period of 30 calendar days (the “30-Day Evaluation Period”). You can access the APY Details page at any time by logging into your SoFi account on the SoFi mobile app or SoFi website and selecting either (i) Banking > Savings > Current APY or (ii) Banking > Checking > Current APY. Upon receiving a Direct Deposit or $5,000 in Qualifying Deposits to your account, you will begin earning 4.60% APY on savings balances (including Vaults) and 0.50% on checking balances on or before the following calendar day. You will continue to earn these APYs for (i) the remainder of the current 30-Day Evaluation Period and through the end of the subsequent 30-Day Evaluation Period and (ii) any following 30-day Evaluation Periods during which SoFi Bank determines you to have Direct Deposit activity or $5,000 in Qualifying Deposits without interruption.

SoFi Bank reserves the right to grant a grace period to account holders following a change in Direct Deposit activity or Qualifying Deposits activity before adjusting rates. If SoFi Bank grants you a grace period, the dates for such grace period will be reflected on the APY Details page of your account. If SoFi Bank determines that you did not have Direct Deposit activity or $5,000 in Qualifying Deposits during the current 30-day Evaluation Period and, if applicable, the grace period, then you will begin earning the rates earned by account holders without either Direct Deposit or Qualifying Deposits until you have Direct Deposit activity or $5,000 in Qualifying Deposits in a subsequent 30-Day Evaluation Period. For the avoidance of doubt, an account holder with both Direct Deposit activity and Qualifying Deposits will earn the rates earned by account holders with Direct Deposit.

Members without either Direct Deposit activity or Qualifying Deposits, as determined by SoFi Bank, during a 30-Day Evaluation Period and, if applicable, the grace period, will earn 1.20% APY on savings balances (including Vaults) and 0.50% APY on checking balances.

Interest rates are variable and subject to change at any time. These rates are current as of 10/24/2023. There is no minimum balance requirement. Additional information can be found at sofi.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

SOBK0923008

SoFi® Checking and Savings is offered through SoFi Bank, N.A. ©2023 SoFi Bank, N.A. All rights reserved. Member FDIC. Equal Housing Lender.

The SoFi Bank Debit Mastercard® is issued by SoFi Bank, N.A., pursuant to license by Mastercard International Incorporated and can be used everywhere Mastercard is accepted. Mastercard is a registered trademark, and the circles design is a trademark of Mastercard International Incorporated.

SoFi members with direct deposit activity can earn 4.60% annual percentage yield (APY) on savings balances (including Vaults) and 0.50% APY on checking balances. Direct Deposit means a deposit to an account holder’s SoFi Checking or Savings account, including payroll, pension, or government payments (e.g., Social Security), made by the account holder’s employer, payroll or benefits provider or government agency (“Direct Deposit”) via the Automated Clearing House (“ACH”) Network during a 30-day Evaluation Period (as defined below). Deposits that are not from an employer or government agency, including but not limited to check deposits, peer-to-peer transfers (e.g., transfers from PayPal, Venmo, etc.), merchant transactions (e.g., transactions from PayPal, Stripe, Square, etc.), and bank ACH funds transfers and wire transfers from external accounts, do not constitute Direct Deposit activity. There is no minimum Direct Deposit amount required to qualify for the stated interest rate.

SoFi members with Qualifying Deposits can earn 4.60% APY on savings balances (including Vaults) and 0.50% APY on checking balances. Qualifying Deposits means one or more deposits that, in the aggregate, are equal to or greater than $5,000 to an account holder’s SoFi Checking and Savings account (“Qualifying Deposits”) during a 30-day Evaluation Period (as defined below). Qualifying Deposits only include those deposits from the following eligible sources: (i) ACH transfers, (ii) inbound wire transfers, (iii) peer-to-peer transfers (i.e., external transfers from PayPal, Venmo, etc. and internal peer-to-peer transfers from a SoFi account belonging to another account holder), (iv) check deposits, (v) instant funding to your SoFi Bank Debit Card, (vi) push payments to your SoFi Bank Debit Card, and (vii) cash deposits. Qualifying Deposits do not include: (i) transfers between an account holder’s Checking account, Savings account, and/or Vaults; (ii) interest payments; (iii) bonuses issued by SoFi Bank or its affiliates; or (iv) credits, reversals, and refunds from SoFi Bank, N.A. (“SoFi Bank”) or from a merchant.

SoFi Bank shall, in its sole discretion, assess each account holder’s Direct Deposit activity and Qualifying Deposits throughout each 30-Day Evaluation Period to determine the applicability of rates and may request additional documentation for verification of eligibility. The 30-Day Evaluation Period refers to the “Start Date” and “End Date” set forth on the APY Details page of your account, which comprises a period of 30 calendar days (the “30-Day Evaluation Period”). You can access the APY Details page at any time by logging into your SoFi account on the SoFi mobile app or SoFi website and selecting either (i) Banking > Savings > Current APY or (ii) Banking > Checking > Current APY. Upon receiving a Direct Deposit or $5,000 in Qualifying Deposits to your account, you will begin earning 4.60% APY on savings balances (including Vaults) and 0.50% on checking balances on or before the following calendar day. You will continue to earn these APYs for (i) the remainder of the current 30-Day Evaluation Period and through the end of the subsequent 30-Day Evaluation Period and (ii) any following 30-day Evaluation Periods during which SoFi Bank determines you to have Direct Deposit activity or $5,000 in Qualifying Deposits without interruption.

SoFi Bank reserves the right to grant a grace period to account holders following a change in Direct Deposit activity or Qualifying Deposits activity before adjusting rates. If SoFi Bank grants you a grace period, the dates for such grace period will be reflected on the APY Details page of your account. If SoFi Bank determines that you did not have Direct Deposit activity or $5,000 in Qualifying Deposits during the current 30-day Evaluation Period and, if applicable, the grace period, then you will begin earning the rates earned by account holders without either Direct Deposit or Qualifying Deposits until you have Direct Deposit activity or $5,000 in Qualifying Deposits in a subsequent 30-Day Evaluation Period. For the avoidance of doubt, an account holder with both Direct Deposit activity and Qualifying Deposits will earn the rates earned by account holders with Direct Deposit.

Members without either Direct Deposit activity or Qualifying Deposits, as determined by SoFi Bank, during a 30-Day Evaluation Period and, if applicable, the grace period, will earn 1.20% APY on savings balances (including Vaults) and 0.50% APY on checking balances.

Interest rates are variable and subject to change at any time. These rates are current as of 10/24/2023. There is no minimum balance requirement. Additional information can be found at sofi.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

SOBK0923008

shapecharge/istockphoto

FG Trade/istockphoto

Featured Image Credit: supersizer/istockphoto.