Safe harbor 401(k) plans enable companies to avoid the annual IRS testing that comes with traditional 401(k) plans. With a safe harbor 401(k), an employer makes mandatory contributions to all employees’ retirement accounts, and those funds vest immediately.

Often a perk used to attract top talent, safe harbor 401(k) plans are a way for highly compensated employees, like company executives and owners, to save more than a traditional 401(k) plan would normally allow.

Keep reading to learn more about safe harbor rules, why companies use these plans, along with the benefits, drawbacks, and relevant deadlines.

What is a Safe Harbor 401(k) Plan?

A 401(k) safe harbor plan is similar to a traditional 401(k) plan — but with a twist. In both cases, eligible employees can use the plan to contribute pre-tax funds to a retirement account and employers may contribute matching funds.

But with a traditional 401(k) retirement plan, companies must submit to annual nondiscrimination regulatory testing by the IRS to ensure that the company plan doesn’t treat highly compensated employees (HCEs) — generally defined as earning at least $150,000 a year in 2023 or owning more than 5% of the business — more favorably than others. The testing process is complex and can be a burden for some companies.

An alternative is to set up a safe harbor 401(k) plan with a safe harbor match. This allows a company to skip the annual IRS testing — and avoid imposing restrictions on employee saving — by providing the same 401(k) contributions to all employees, regardless of title, salary, or even years spent at the company. And those funds must vest immediately.

This is an important benefit, because in many cases, employer contributions to traditional 401(k) plans vest over time, requiring employees to stay with the company for some years in order to get the full value of the employer match. Often, if you leave before the employer contributions or match have vested, you may forfeit them.

For smaller companies, it may be worth making the extra safe harbor match contributions in order to avoid the time and expense of the IRS’s annual nondiscrimination testing. For larger companies, giving all employees the same percentage contribution could be expensive. But the upside is that highly paid employees can then make much larger 401(k) contributions without running afoul of IRS rules, a real perk for company leaders. In addition, 401(k) safe harbor plans are typically less expensive to set up than traditional plans.

Key Takeaways

Here’s a quick overview of a safe harbor 401(k).

- Like a traditional 401(k), a safe harbor 401(k) lets employees deposit tax-deferred funds from their paychecks into a retirement savings account.

- Employers are required to contribute to employees’ safe harbor 401(k) accounts.

- Employer contributions in a safe harbor 401(k) vest immediately. There is no waiting period.

- Highly-paid employees can contribute more to a safe harbor 401(k) than a traditional 40(k)

- Safe harbor 401(k) plans allow companies to skip the annual nondiscrimination regulatory testing required by the IRS for traditional 401(k)s.

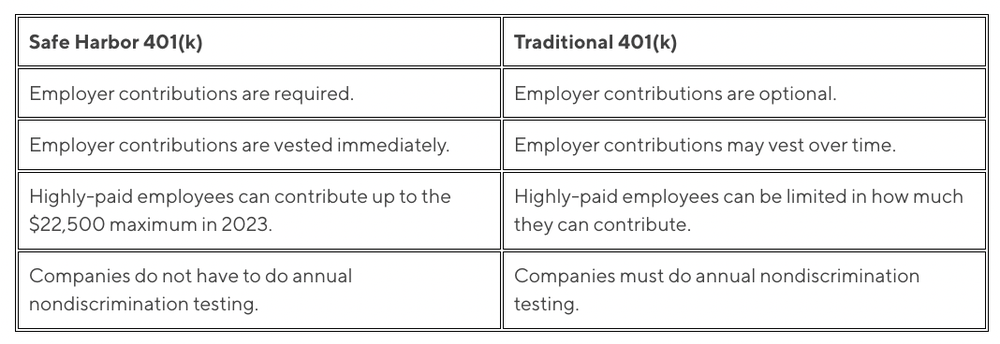

Traditional 401(k) vs. Safe Harbor 401(k) Plans

While safe harbor 401(k)s and traditional 401(k) plans are similar in many ways, there are some important differences that employers should be aware of.

For instance, with traditional 401(k) plans, contributions from highly compensated employees can’t comprise more than 2% of the average of all other employee contributions, in addition to other restrictions. However, with safe harbor 401(k) plans, those limits don’t apply.

Comparing Plan Features and Benefits

Here is a side-by-side comparison of a safe harbor 401(k) vs. a traditional 401(k)

Choosing the Right Plan for Your Business

A safe harbor plan may be beneficial for some smaller companies that can’t afford the expense of nondiscrimination testing. In addition, the plan is simpler with less administrative tasks.

A company might also choose a safe harbor 401(k) if it has some key high-earning employees that make up a large share of the workforce.

However, if your company is able to easily manage the nondiscrimination testing process, you may want to opt for a traditional 401(k). A traditional 401(k) could also be a good option for business owners who want to try to retain employees over the long-term. They could set up a vesting schedule for employer contributions that requires employees to be with the company for three years before becoming fully vested, for instance.

Setting Up a Safe Harbor 401(k) Plan

For employers interested in using a safe harbor 401(k), there are some general rules and guidelines they will need to follow.

Requirements, Contribution Formulas, and Deadlines

To fulfill the safe harbor 401(k) requirements, the employer must make qualifying 401(k) contributions (a.k.a. the safe harbor match) that vest immediately. The company contributes to employees’ retirement accounts in one of three ways:

- Non-elective: The company contributes the equivalent of 3% of each employee’s annual salary to a company 401(k) plan, regardless of whether the employee contributes.

- Basic: The company offers 100% matching for the first 3% of an employee’s 401(k) plan contributions, plus a 50% match for up to 5% of an employee’s contributions.

- Enhanced: The company offers a 100% company match for all employee 401(k) contributions, up to 4% of a staffer’s annual salary.

Companies that opt for a safe harbor 401(k) plan have to adhere to strict compliance filing deadlines. These are the dates worth knowing.

October 1: That’s the deadline for filing for a safe harbor 401(k) for the current calendar year. This deadline meets the government criteria of a company needing to have a safe harbor 401(k) in operation for at least three months in a 12 month period, for the first year operating a safe harbor plan.

December 1: By this date, all companies — whether they’re rolling out a brand new safe harbor plan or are administering an existing one — must issue a formal notice to employees that a safe harbor 401(k) will be offered to company staffers.

January 1: The date that all safe harbor 401(k) plans are activated.

For companies that currently have no 401(k) plan at all, they can roll out either a traditional 401(k) plan or a safe harbor 401(k) plan at any point in the year, for that calendar year.

Advantages of Implementing a Safe Harbor 401(k) Plan

Safe harbor 401(k)s offer some distinct upsides for business owners and employees alike.

Benefits for Employers and Employees

By creating a safe harbor 401(k) plan, a business owner can potentially attract and maintain highly skilled employees. Employees are attracted to higher retirement plan contributions and the ability to optimize retirement plan contribution amounts, ensuring more money for long-term retirement savings.

Plus, a safe harbor 401(k) plan can also help business owners save money on the compliance end of the spectrum. For example, companies save on regulatory costs by avoiding the costs of preparing for a nondiscrimination test (and the staff hours and training that goes with it).

There are some additional upsides to offering a safe harbor 401(k) retirement plan, for higher paid employees and regular staff too.

- Playing catch up. If a company owner, or high-level managers, historically haven’t stowed enough money away in a company retirement plan, a safe harbor 401(k) plan can help them catch up. The same may be true, although to a lesser degree, for regular employees.

- The spread of profit. Suppose a company has a steady and robust revenue stream and is managed efficiently. In that case, company owners may feel comfortable “spreading the wealth” with not only high-profile talent but rank-and-file employees, too.

- Encourage retirement savings. If a company is seeing weak contribution activity from its rank-and-file employees, it may feel more comfortable going the safe harbor route and at least guaranteeing minimum 401(k) contributions to employees while rewarding higher-value employees with more lucrative 401(k) plan contributions.

Disadvantages of Safe Harbor Plans

Safe harbor 401(k) plans have their downsides, too. Here are some drawbacks to consider.

Financial Implications for Employers

The matching contribution requirements for safe harbor 401(k)s can add up to a hefty expense, depending on employee salaries. And because employees are vested immediately, there’s no incentive to stay with the company for a certain period.

In addition, if a company introduces a safe harbor 401(k) plan, it must commit to it for one calendar year, no matter how the plan is performing internally. Even after a year, 401(k) plan providers (which administer and manage the retirement plans) may charge a termination fee if a company decides to pull the plug on its safe harbor plan after one year.

Safe Harbor 401(k) Contribution Limits and Match Types

There are some different rules for employer contribution limits and matching with a safe harbor 401(k) vs. a traditional 401(k).

Understanding Contribution Limits

Just like traditional 401(k) plans, the maximum employee contribution limit for a safe harbor plan is $22,500 in 2023 and $23,000 in 2024. If you are over 50, you would be eligible for an additional $7,500 catch-up contribution, if your plan allows it.

But in a safe harbor plan, a company owner can reserve the maximum $22,500 (in 2023) for their plan contribution and also boost contribution payments to valued team members up to an individual profit-sharing maximum amount of 100% of their compensation, or $66,000 in 2023 ($73,500 for those over age 50) — whichever is less.

Regular employees are allowed the standard maximum contribution limit of $22,500 in 2023, plus anyone over age 50 can contribute an extra “catch-up” amount of $7,500. Those are the same maximum contribution ceilings as regular 401(k) plans.

Different Types of Employer Matching Contributions

As mentioned earlier, with a safe harbor 401(k), an employer must make qualifying 401(k) contributions that vest immediately in one of these ways:

- Non-elective: The company contributes the equivalent of 3% of each employee’s annual salary to a company 401(k) plan.

- Basic: The company matches 100% for the first 3% of an employee’s 401(k) plan contributions, plus a 50% match for the following 2% of their contributions.

- Enhanced: The company provides a 100% company match for all employee 401(k) contributions, up to 4% of a staffer’s annual salary.

IRS Compliance Testing and Safe Harbor Provisions

To help understand the benefit of safe harbor plans, it helps to see what employers with traditional 401(k) plans face in terms of following IRS rules and submitting to the annual nondiscrimination tests.

Navigating Non-Discrimination Testing

Each year, a company must conduct Actual Deferral Percentage (ADP), Actual Contribution Percentage (ACP), and Top Heavy tests to confirm there is no compensation discrimination.

If the company fails one of the tests, it could mean considerable administrative hassle, plus the expense of making corrections, and potentially even refunding 401(k) contributions.

Before explaining the details of each test, here’s a refresher on how the IRS defines highly compensated employees (HCEs) and non-highly compensated employees (NHCEs).

To be a HCE:

- The employee must own more than 5% of the company at any time during the current or preceding year (directly or through family attribution).

- The employee is paid over $150,000 in compensation from the employer for 2023. The plan can limit these employees to the top 20% of employees who make the most money.

Employees who don’t fit these criteria are considered non-highly compensated. The nondiscrimination tests are designed to assess whether top employees are saving substantially more than the rank-and-file staffers.

- The Actual Deferral Percentage (ADP) test measures how much income highly paid employees contribute to their 401(k), versus staff employees.

- The Actual Contribution Percentage (ACP) test compares employer retirement contributions to HCEs versus the contributions to everyone else.

According to the IRS, the terms of the ADP test — which compares the amounts different employees are saving in their 401(k)s — are met if the ADP for highly compensated employees (HCE) doesn’t exceed the greater of:

- 125% of the deferral percentage for ordinary, i.e., non-highly compensated employees (NHCEs)

Or the lesser of:

- 200% of the deferral percentage for the NHCEs

- or the deferral percentage for the NHCEs plus 2%.

The ACP test is met if the deferral percentage for highly compensated employees doesn’t exceed the greater of:

- 125% of the deferral percentage for the NHCEs,

Or the lesser of:

- 200% of the deferral percentage for the group of NHCEs

- or the deferral percentage for the NHCEs plus 2%.

Last, the top-heavy test measures the value of the assets in all company 401(k) accounts, total. If the 401(k) balances of “key employees” account for more than 60% of total plan assets, the 401(k) would fail the top heavy test. The IRS defines key employees somewhat differently than highly compensated employees, although both groups are similar in that they earn more than ordinary staff.

As you can see, maintaining a traditional 401(k) plan, and meeting these requirements each year, can be a burden for some companies. Fortunately, by setting up a safe harbor 401(k) plan, a company can avoid the annual nondiscrimination tests and still provide a 401(k) savings plan for employees.

The Takeaway

Companies that don’t want the regulatory obligations of a traditional 401(k) plan, and would like to prioritize talent acquisition and employee retention may want to consider safe harbor 401(k) plans.

However, a business owner needs to weigh the pros and cons of a safe harbor 401(k) plan because, in some cases, it can be expensive for a company to maintain.

But no matter what type of 401(k) an employer decides to go with, having a retirement plan in place, with different savings and investment options, can help employees — and business owners themselves — save for the future.

This article originally appeared on SoFi.com and was syndicated by MediaFeed.org.

Third-Party Brand Mentions: No brands, products, or companies mentioned are affiliated with SoFi, nor do they endorse or sponsor this article. Third-party trademarks referenced herein are property of their respective owners.

Tax Information: This article provides general background information only and is not intended to serve as legal or tax advice or as a substitute for legal counsel. You should consult your own attorney and/or tax advisor if you have a question requiring legal or tax advice.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

SoFi Invest®

SoFi Invest refers to the two investment and trading platforms operated by Social Finance, Inc. and its affiliates (described below). Individual customer accounts may be subject to the terms applicable to one or more of the platforms below.

1) Automated Investing and advisory services are provided by SoFi Wealth LLC, an SEC-registered investment adviser (“SoFi Wealth“). Brokerage services are provided to SoFi Wealth LLC by SoFi Securities LLC.

2) Active Investing and brokerage services are provided by SoFi Securities LLC, Member FINRA(www.finra.org)/SIPC(www.sipc.org). Clearing and custody of all securities are provided by APEX Clearing Corporation.

For additional disclosures related to the SoFi Invest platforms described above, including state licensure of SoFi Digital Assets, LLC, please visit SoFi.com/legal.

Neither the Investment Advisor Representatives of SoFi Wealth, nor the Registered Representatives of SoFi Securities are compensated for the sale of any product or service sold through any SoFi Invest platform. Information related to lending products contained herein should not be construed as an offer or pre-qualification for any loan product offered by SoFi Bank, N.A.

More from MediaFeed:

Are Americans ready to have a holly, jolly consumer Christmas?

As competition for consumers increases with an ever-expanding market, small businesses need to be smart and strategic about attracting customers and closing sales—particularly around the holidays. Data shows that up to 65% of small businesses’ annual revenue was generated during the holidays last year. With that much money on the line, holidays mean big business for small businesses.

But when the busy season of the holidays nears, limited resources and high demand can stretch small businesses to the limit and leave them unsure where to put their time and money. A new Intuit QuickBooks-commissioned survey of 6,500 adults in the US reveals how small businesses can unwrap success this holiday season.

This year, small businesses can look forward to a 42%increase in consumer spending over the holiday season, increasing from $88 billion to an estimated $125 billion. This averages approximately $485 towards what each consumer may have earmarked to shop small this year. Despite economic volatility and a climate where inflation and interest rates continue to fluctuate, shopping small is holding strong with consumers.

What’s driving the increase in small business spending? Work bonuses and savings. More than a third of respondents (34%) expect a bonus this holiday season and of these, more than two-thirds (69%) say this will allow them to spend more money at small businesses. Further, 7 in 10 consumers (70%) shared that they began saving for their holiday gift shopping in September of this year or earlier.

QuickBooks

The spirit of gift-giving is alive and well this holiday season. More than 9 in 10 (94%) consumers plan to buy gifts this holiday season with most buying gifts for children (58%), a spouse (41%), or a parent (40%). On average, consumers will be shopping for gifts for 13 people this year.

And while gifting experiences is a trend that comes and goes, small businesses need not feel that pressure this holiday season. As more time passes from the start of the pandemic, 2 in 5 (43%) consumers say they do not have a preference between presents and experiences and a majority (55%) prefer to gift presents over experiences.

Kerkez/istockphoto

The early kick-off to holiday shopping is still in effect this year. Nearly 1 in 5 (19%) consumers say they’re planning to start shopping before October. Small businesses don’t want to be unprepared for early shoppers and can stay ahead by making sure inventory is available before the busy season and well stocked in November. Two in 5 (41%) consumers say they plan to start shopping in November this year and almost half (48%) of consumers indicate they do most of their shopping in November. Among those planning to shop small this year, Small Business Saturday (November 25) is the most popular day (46%) with Black Friday (November 24) as a close second (43%).

QuickBooks

Bridging the gap between an online and in-person shopping experience could boost sales for small businesses this season—and remembering to advertise sales online. Now more than ever, consumers have a sea of options at their fingertips. And with the peak of the pandemic firmly in the rearview mirror, the appeal of in-person shopping is growing. Data shows that consumer interest in balancing the digital and in-person experience will have a surge this holiday season. Most consumers (43%) plan to shop equally online and in-person for the holidays this year (compared with only 28% who say they plan to shop primarily in-person and 29% who say they plan to shop primarily online). Behind this push? Three in 5 (61%) consumers say they find the best small business deals in-person. When it comes to customer service, consumers are clear: 73% say the option to buy online and pick up in store and home delivery options are more likely to get them to buy from small businesses.

Dragos Condrea/istockphoto

Respondents: 5,905 US adults, age 18+

QuickBooks

Small businesses selling in-person this season should be mindful of keeping crowds from becoming too overwhelming. While holiday cheer should be in the air, many consumers are drained by the shopping demands of the season. Excitement could be waning because a majority of consumers find holiday shopping to be a stressful experience. More than 1 in 2 (57%) consumers say shopping for the holidays is stressful and the biggest contributor to this stress iscrowded stores (67%).

Consumers looking to avoid the stressors of holiday shopping are favoring small businesses. Nearly 3 in 5 (59%) consumers say shopping at small businesses is less stressful than shopping at big retailers. Among these consumers, almost half (49%) expect to spend more at small businesses this holiday season.

QuickBooks

A major factor in supporting crowd control is offering a seamless and fast checkout experience. As shown above, almost two-thirds (63%) of consumers say they’re more likely to buy from small businesses with a physical store if they offer contactless or mobile payments. Digitizing the checkout experience as much as possible and integrating payment solutions that allow consumers to pay the way they want with online invoicing, mobile payment apps, and in-person card readers is good for business.

Adam Yee/istockphoto

Bring in Buy Now, Pay Later for a boost

Small online retailers, particularly those with younger customers, should offer Buy Now, Pay Later (BNPL) for a boost in sales. Providing flexibility and the appeal of no interest rates for shorter terms, BNPL has the potential to attract new customers and retain loyal ones. Three in 5 (60%) consumers plan to use BNPL for holiday shopping this year. Demand for BNPL is higher among younger consumers with 70% aged 18-24 planning to use it for the holidays.

Discounts can make a sale

Small businesses hoping for a successful holiday season can offer discounts and sales as a strategic move. For small businesses with a store, remember to offer discounts both in-store and online. Consumers are doing their research with holiday deals and shipping options top of mind. Almost all (94%) consumers say they compare prices between small businesses and big retailers during the holiday season. Among those who compare prices, 50% say they do so always or often. But most importantly, 51% of consumers say finding a better deal at a bigger retailer or better shipping options (44%) would make them not buy from a small business. Small businesses can leverage an updated website, email marketing, and social media to advertise too-good-to-pass-up deals during this busy season.

Venture into video

Product-based small businesses that sell directly from a website can capitalize on the rise of video. Video has become increasingly important. With small businesses hoping to find new customers and keep current customers coming back, video is an important tool. Search engines, particularly Google, and social media love videos—and so do consumers. Seven in 10 (71%) consumers say they’re more likely to buy a product from a small business’s website during the holiday season if there’s a video showcasing it.

sturti/istockphoto

With a long list of social media apps, it can be hard for small businesses to know where to focus their energies. And while TikTok’s popularity is solidly in place among Gen Z, Facebook is still a major player overall. One third (36%) of consumers say they look to Facebook for gift inspiration, making it top the list of social media platforms for holiday inspiration. This holds true for millennial consumers aged 25-44 as well with almost half (49%) saying they turn to Facebook for gift inspiration.

When it comes to sales, consumers planning to buy from social media rank Facebook (62%) as the top app they’re most likely to purchase from. Instagram (55%) is a close second.

Partner with influencers for more sway with younger customers

The power of the influencer is redefining marketing. For small businesses with a larger base of young customers, partnering with influencers to promote their products and services during the holiday season can have a large return on investment. While 1 in 3 (33%) consumers agree that they’re more likely to buy from a small business if an influencer promotes their products, services, or experiences, among Gen Z consumers aged 18-24, this jumps to 43%. For consumers persuaded by the pull of influencers, 57% said they trust influencers with up to 1 million followers the most.

QuickBooks

Just as data showed last holiday season, customers are eager to support local small businesses this holiday season. For small businesses, leaning into their location and building a community of loyal shoppers could be the key to holiday success. Three in 5 (62%) consumers say they’re more likely to buy from a small business if it’s local. And 2 in 3(68%) consumers say already being part of a small business’s rewards or loyalty program is more likely to make them shop there this holiday season. Donating small business proceeds to charity (38%) is the second biggest pull among consumers.

This article originally appeared on the QuickBooks Resource Center and was syndicated by MediaFeed.org.

QuickBooks

Nuttawan Jayawan/istockphoto

Featured Image Credit: PeopleImages/istockphoto.