Can’t Hurry Doves

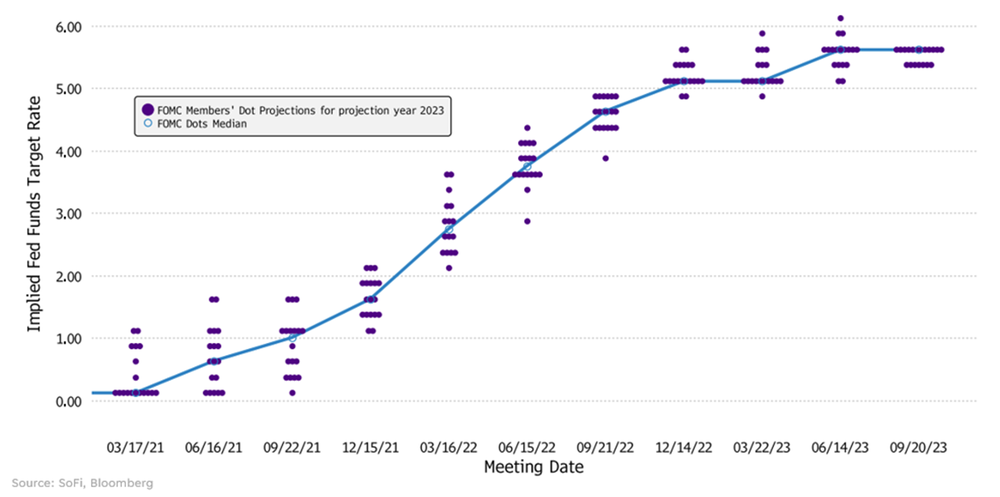

Before this Fed meeting, the market had priced in a zero percent chance of an interest rate hike in September, and the market was right, rates remained unchanged. This was also one of the quarterly meetings when we get an update on the dot plot (a chart of all FOMC committee members’ projections for the fed funds rate, below), and a new summary of economic projections.

This is the dot plot for 2023 showing the change in expectations from prior meetings, and the current median expectation for a fed funds rate of 5.6% by year end. That suggests one more hike in either November or December. Not shown is the dot plot for 2024, which indicates a median fed funds rate of 5.1% by year end, thus suggesting two cuts at some point next year.

Both the 2023 and 2024 dot plot charts show a similar pattern of rising dramatically over the last year and a half. The takeaways I have from these data sets are: 1) inflation was and remains high, and troublesome, 2) the dot plot is not very good at predicting where rates will be, 3) the Fed is not going to forecast a recession in its rate predictions.

Where does that leave us as investors? Just as data-dependent as the Fed is, and with the knowledge that the onus for risk-management in our portfolios is on us, not them. One of the biggest risks I think we’re exposed to as investors is the conditioning that the Fed will save us from severe drawdowns.

(Learn more: Personal Loan Calculator)

Hurry Up and Wait

There’s so much anticipation for these meetings, especially when we have a month break in between. Often the actual announcement is anticlimactic, and recently the commentary has been rather boilerplate, which leaves us digging for signals in things like the tone of Powell’s voice or the color of his tie.

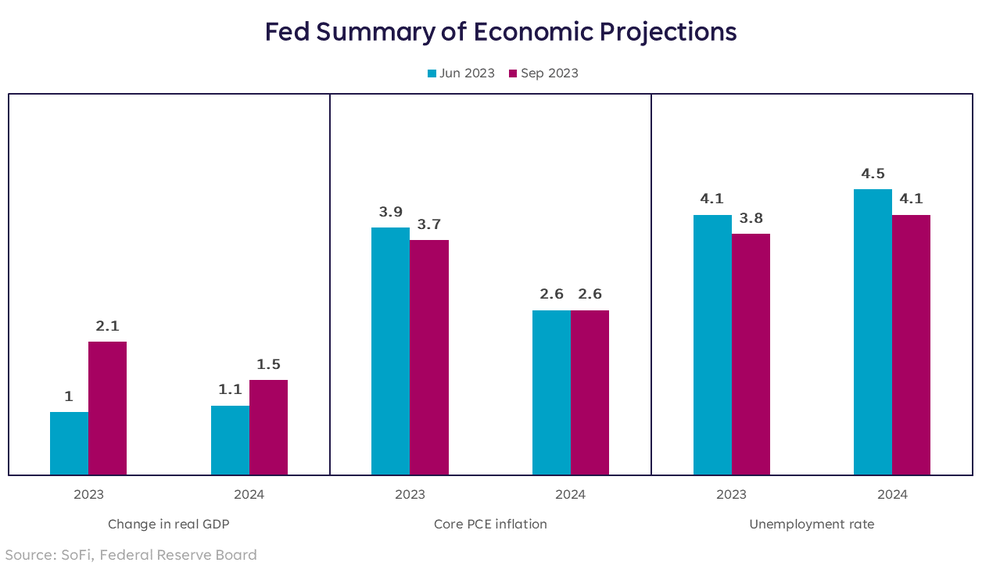

The quarterly gift we receive in the form of updated economic projections can be much more interesting. Well, interesting relative to the color of his tie, which is usually purple. This quarter, the projections moved slightly, as illustrated below. The Fed now expects stronger growth and lower unemployment both this year and next, and slightly cooler inflation this year with steady inflation next year as compared to the prior projections.

We can look at this and interpret it as positive — economy stronger than expected and inflation cooler or as expected. My concern is whether these projections are consistent with the current environment.

Meaning, if the goal is to get inflation back down to 2% — a goal that was reiterated multiple times today by Chairman Powell — we will very likely need to see a period of below-trend growth. In that case, margins are likely to be compressed further, putting pressure on company spending, and in turn, labor costs.

Take that concept even further, and if companies have to start cutting labor costs, consumers may stop feeling as confident and pull back on their spending. And so on, and so forth. That’s only one perspective based on growth expectations, but I still don’t think we’ve seen all of the effects of rate hikes. I know I keep saying that, but only because I keep believing it.

(Learn more Are You Addicted to Money?)

The Carrot Is Further Away

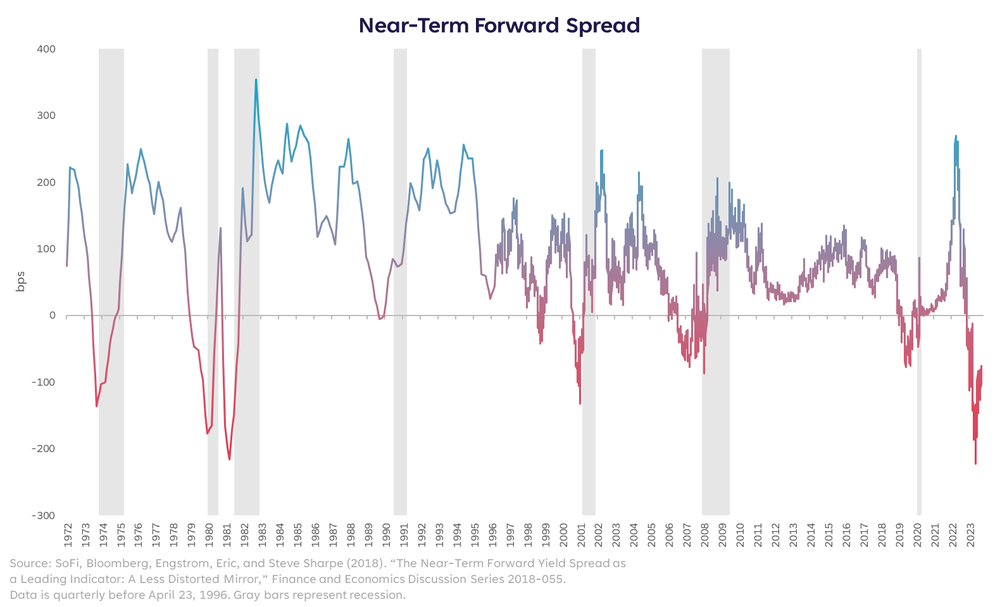

…but it’s still a carrot. I don’t know if this cycle really is longer, or if we are just more impatient. In either case, there are some signals that are indisputable. One of those signals is the Fed’s preferred yield curve spread, called the near-term forward spread (NTFS). The NTFS measures the difference between the expected 3-month interest rate 18 months from now and the current 3-month yield. When this measure is inverted, it serves as a reasonably reliable recessionary signal, as illustrated in the chart below.

The NTFS isn’t the only troubling indicator, but it’s an important one. It’s in decidedly worrisome territory, and has been since November 2022.

A stronger economy can fend off some of these restrictive measures for a while, but at some point a victor will emerge, and there’s still no telling whether the stronger-than-expected economy or the restrictive environment will come out on top. We’re all rooting for the economy to win the fight, but warning signals and what history suggests about aggressive tightening are putting up a heckuva fight.

This article originally appeared on SoFi.com and was syndicated by MediaFeed.org.

Communication of SoFi Wealth LLC an SEC Registered Investment Adviser. Information about SoFi Wealth’s advisory operations, services, and fees is set forth in SoFi Wealth’s current Form ADV Part 2 (Brochure), a copy of which is available upon request and at SEC. Liz Young is a Registered Representative of SoFi Securities and Investment Advisor Representative of SoFi Wealth. Her ADV 2B is available at SoFi.

More from MediaFeed

Credit card debt is out of control in these states

Millions of Americans continue to struggle with credit card debt. The average credit card debt in America is $6,039 as of August 2023, according to a new report from TransUnion®.

Out of the 50 states, Alaska has the highest average credit card debt ($7,248), while Wisconsin has the lowest average ($4,853), data show.

More than 6 million cardholders are at least 30 days past due on a minimum payment, according to TransUnion’s credit card delinquency data.

Your credit card balance is your credit card debt. Making transactions on your credit card is a liability that eventually needs to be repaid. Below we highlight the average credit card debt in all 50 states and explain why making minimum payments each billing cycle may not be right for you.

Consumer credit card debt in the United States exceeds $1 trillion as of the second quarter (Q2) of 2023, according to the Federal Reserve Bank of New York.

The average American credit card debt increased to $6,039 in August 2023 (it was $5,982 in July 2023 and $5,416 in August 2022), according to TransUnion, a nationwide credit bureau.

Credit card debt can be costly if you’re paying interest charges. The average interest rate on credit cards is 22.16% as of Q2 2023, according to Federal Reserve data on credit card accounts assessed interest.

Atstock Productions/istockphoto

Consumer credit card debt in the United States exceeds $1 trillion as of the second quarter (Q2) of 2023, according to the Federal Reserve Bank of New York.

The average American credit card debt increased to $6,039 in August 2023 (it was $5,982 in July 2023 and $5,416 in August 2022), according to TransUnion, a nationwide credit bureau.

Credit card debt can be costly if you’re paying interest charges. The average interest rate on credit cards is 22.16% as of Q2 2023, according to Federal Reserve data on credit card accounts assessed interest.

damircudic/istockphoto

TransUnion publishes U.S. credit card debt data every month in all 50 states and the District of Columbia. We’re tracking the data as it becomes available and then ranking the average credit card debt by state in descending order using TransUnion’s recent industry snapshot (August 2023):

District of Columbia

The nation’s capital is not a state, but the District of Columbia has one of the highest average credit card debt balances in the United States. The average credit card debt in Washington, D.C., stands at $7,070 per consumer as of August.

(Learn more atPersonal Loan Calculator)

Milton Rodriguez/istockphoto

Alaska is the largest state in the country in terms of its geographical boundaries (586,412 square miles). It also leads all 50 states with the highest average credit card debt in the nation. Cardholders in Alaska have an average credit card balance of $7,248 as of August.

chaolik/istockphoto

Maryland sits south of the Mason-Dixon line. This Old Line State has a relatively high credit card debt in the USA. The average credit card debt in Maryland stands at $6,783 per consumer as of August.

ferrantraite/istockphoto

Nevada may have some issues with gambling debt. This predominantly desert and semiarid state also ranks high in credit card debt. The average credit card debt in Nevada is $6,619 per consumer as of August.

4kodiak/istockphoto

New Jersey is the most densely populated state in the United States. The Garden State also has a high average credit card debt. Cardholders in New Jersey have an average credit card balance of $6,565 as of August.

Ultima_Gaina/istockphoto

Hawaii sports tropical climate and active volcanoes. This state of islands in the Pacific is also known for its relatively high average credit card debt. Consumers in the Aloha State have an average credit card balance of $6,547 as of August.

Art Wager/istockphoto

Virginia enjoys close proximity to the nation’s capital in a region locally nicknamed DMV (District of Columbia, Maryland, and Virginia). Similar to Maryland and Washington, D.C., consumers in the Old Dominion state carry a relatively high average credit card debt in America. Virginia’s average credit card debt stands at $6,535 per consumer as of August.

ferrantraite/istockphoto

Nicknamed the Constitution State, Connecticut has the highest average credit card debt in New England. What is the average credit card debt in Connecticut? It’s $6,499 per consumer as of August.

DenisTangneyJr/istockphoto

Texas is one of the largest states in the nation in terms of its geographical boundaries and population. The Lone Star State also has a relatively high average credit card debt in the U.S. The average credit card debt in Texas is $6,499 per consumer as of August.

dszc/istockphoto

Colorado hosts a large stretch of the Rocky Mountains. The Centennial State also hosts a large amount of credit card debt per consumer. The average credit card debt in Colorado is $6,425 per cardholder as of August.

milehightraveler/istockphoto

Florida is one of the largest states in the nation in terms of population and economic activity. The Sunshine State has more than 22 million residents and a gross domestic product (GDP) of nearly $1.4 trillion as of 2022. The average credit card debt in Florida is $6,423 per consumer as of August.

Kasra Keighobady/istockphoto

California is the most populous state in the nation with more than 38.9 million people as of Jan. 1, 2023. The Golden State also has one of the highest amounts of credit card debt per consumer. The average credit card debt in California is $6,418 per cardholder as of August.

Spondylolithesis/istockphoto

Georgia produces tons of agricultural goods, but the Peach State also has a relatively high level of credit card debt. The average credit card debt in Georgia is $6,357 per consumer as of August.

SeanPavonePhoto/istockphoto

Washington state borders the Canadian province of British Columbia and carries a relatively high amount of credit card debt per consumer. The average credit card debt in Washington is $6,317 per cardholder as of August.

400tmax/istockphoto

New York remains one of the largest states in the nation despite its recent decline in population. The average credit card debt in New York is $6,313 per consumer as of August.

TomasSereda/istockphoto

Arizona welcomes domestic and international tourism with its Grand Canyon natural landmark and desert climate. The average credit card debt in Arizona is $6,129 per consumer as of August.

Davel5957/istockphoto

Wyoming has the smallest population in the nation (fewer than 600,000 people). But this Mountain West state has a relatively high amount of credit card debt per consumer. The average credit card debt in Wyoming is $6,081 per cardholder as of August.

DenisTangneyJr/istockphoto

Delaware is a relatively small state in terms of its geographical boundaries and population. The First State, however, is one of the bigger states in terms of average credit card debt. The average credit card debt in Delaware is $6,046 per consumer as of August.

DenisTangneyJr/istockphoto

Massachusetts rests in the heart of New England. The Bay State also has a relatively high amount of credit card debt per consumer. The average credit card debt in Massachusetts is $6,021 per cardholder as of August.

ivanastar/istockphoto

Illinois enjoys its reputation as the Land of Lincoln. This Midwestern state also has a relatively high amount of credit card debt per consumer. The average credit card debt in Illinois is $6,015 per cardholder as of August.

Shelly Bychowski/istockphoto

Utah has the Great Salt Lake and a smaller average credit card debt than most of the states it borders. The average credit card debt in Utah is $5,957 per consumer as of August.

4kodiak/istockphoto

Oklahoma is located in the middle of the 48 contiguous states. The Sooner State is also near the middle of the pack regarding average credit card debt in America. The average credit card debt in Oklahoma is $5,920 per consumer as of August.

Tiago_Fernandez/istockphoto

Rhode Island is the smallest state in the country in terms of its geographical area (1,214 square miles). The average credit card debt in Rhode Island is $5,903 per consumer as of August.

DenisTangneyJr/istockphoto

New Hampshire represents one of the smaller states but has a high amount of credit card debt per consumer. The average credit card balance in New Hampshire is $5,875 per cardholder as of August.

DenisTangneyJr/istockphoto

South Carolina is known for its coastline and beaches. The Palmetto State shares a border with Georgia but has a much smaller scale of credit card debt on average. The average credit card debt in South Carolina is $5,839 per consumer as of August.

SeanPavonePhoto/istockphoto

Oregon carries a lower level of credit card debt per consumer than most of the states it borders. The average credit card debt in Oregon is $5,831 per cardholder as of August.

BruceBlock/istockphoto

North Carolina is known for its colleges, universities, and military bases, among other things. (The Tar Heel State has several state-based student loan forgiveness programs.) The average credit card debt in North Carolina is $5,779 per consumer as of August.

Mark Howard/istockphoto

Louisiana sits along the Gulf Coast in the South. The Pelican State is also known as the Creole State and the Sugar State. The average credit card debt in Louisiana is $5,721 per consumer as of August.

ghornephoto/istockphoto

Nicknamed the Keystone State, Pennsylvania has a lower amount of credit card debt per consumer compared with its Mid-Atlantic neighbors of New York and New Jersey. The average credit card debt in Pennsylvania is $5,638 per cardholder as of August.

Sean Pavone/istockphoto

Well-known for its country music scene, Tennessee has a lower credit card debt per consumer than most of the 50 states. The average credit card balance in Tennessee is $5,596 per cardholder as of August.

benedek/istockphoto

Idaho is nicknamed the Gem State and is known for its potatoes. Average credit card debt per consumer in Idaho is one of the lowest in the Mountain West region. The average credit card balance in Idaho is $5,586 per cardholder as of August.

Sean Pavone/istockphoto

New Mexico has a lower credit card debt per consumer than each of the neighboring states surrounding it. The average credit card debt in New Mexico is $5,548 per cardholder as of August.

Sean Pavone/istockphoto

Missouri is not just any state — it’s the Show Me State. The average credit card debt in Missouri is $5,521 per consumer as of August.

Art Wager/istockphoto

Alabama enjoys a coastline along the Gulf Coast. Known as the Cotton State, Alabama is also known for peanuts. The average credit card debt in Alabama is $5,520 per consumer as of August.

Art Wager/istockphoto

Minnesota became the North Star State because of its geographical location in the country’s heartland. The average credit card debt in Minnesota is $5,507 per consumer as of August.

Davel5957/istockphoto

Montana is known as America’s Treasure State and Big Sky Country. Montana also has the lowest average credit card debt in the Mountain West region. The average credit card balance in Montana hovers at $5,501 per cardholder as of August.

powerofforever/istockphoto

North Dakota has multiple nicknames, including the Flickertail State, Sioux State, and the Peace Garden State. The average credit card debt in North Dakota is $5,465 per consumer as of August.

Wirestock/istockphoto

Kansas markets itself as the Sunflower State. The average credit card balance in Kansas is $5,415 per consumer as of August.

TriggerPhoto/istockphoto

Maine has relatively low credit card debt per consumer compared with other New England states. The Pine Tree State also has among the lowest credit card debt per consumer along the East Coast. The average credit card balance in Maine is $5,387 per cardholder as of August.

Sean Pavone/istockphoto

Mississippi is one of the poorest states in the nation, but the cost of living in the Magnolia State is also among the lowest nationwide. The average credit card debt in Mississippi is $5,373 per consumer as of August.

SeanPavonePhoto/istockphoto

Vermont is known as the Green Mountain State. The average credit card debt in Vermont is $5,362 per consumer as of August.

Sean Pavone/istockphoto

Nebraska produces 81.6% of the nation’s great northern beans as of 2022, according to federal data. The average credit card debt balance in Nebraska is $5,356 per consumer as of August.

wellesenterprises/istockphoto

Michigan hosts several manufacturers of popular car makes and models. It’s also known as the Wolverine State and the Great Lake State. The average credit card debt in Michigan is $5,344 per consumer as of August.

pawel.gaul/istockphoto

Arkansas — dubbed the Natural State because of its wildlife, bodies of water, and preserved open space — is a Southern state with a relatively low level of credit card debt per consumer. The average credit card debt in Arkansas is $5,297 per cardholder as of August.

Sean Pavone/istockphoto

Ohio serves 11.8 million residents as of 2022, making Ohio one of the most populous states in the nation. The Buckeye State also has among the lowest credit card debt per consumer in the United States. The average credit card debt in Ohio is $5,297 per cardholder as of August.

Sean Pavone/istockphoto

South Dakota hosts the famous Mount Rushmore National Memorial. The average credit card debt in South Dakota is $5,264 per consumer as of August.

DenisTangneyJr/istockphoto

West Virginia remains one of the few states that may pay you to move there if you work from home. The average credit card debt in West Virginia is $5,217 per consumer as of August.

Wirestock/istockphoto

Indiana is America’s Hoosier State. The average credit card debt in Indiana is $5,216 per consumer as of August — one of the lowest in the nation.

Ultima_Gaina/istockphoto

Kentucky has a relatively low level of credit card debt per consumer. The average credit card debt in Kentucky is $5,041 per cardholder as of August.

alexeys/istockphoto

Iowa ranks first in the nation in the production of corn for grain. The average credit card debt in Iowa is $4,976 per consumer as of August.

DS70/istockphoto

Wisconsin remains the largest cheese producer in the nation, and consumers in America’s Dairyland have the lowest average credit card balances nationwide. The average credit card debt in Wisconsin is $4,853 per cardholder as of August.

csfotoimages/istockphoto

")

You can find out your credit card balance by reading your credit card statement. Your credit card balance matters because it’s your unpaid credit card debt that you are expected to repay as fast or as slow as you wish.

The slowest way to pay down credit card debt is to make minimum payments each billing cycle. The fastest way to pay down credit card debt is to pay the full statement balance each billing cycle.

Cardholders with a credit card grace period may avoid interest charges on new purchases by paying the statement balance in full each billing cycle.The annual percentage rate (APR) on a credit card can be quite high compared with other consumer lending products. If you make minimum payments each billing cycle, it could take years to pay off the debt and the interest charges could be costly in particular.

How much credit card debt does the average American have? The average American credit card balance is $6,039 per consumer as of August 2023, according to TransUnion data.

Delmaine Donson/istockphoto

In general, leaving a small balance on your credit card is not the best idea if your goal is to build credit without incurring interest charges.

Carrying a small balance may not be right for you if you can afford to pay off your statement balance each billing cycle. Unless you have a 0% introductory APR, you may face interest charges if you pay less than the statement balance.

staticnak1983/istockphoto

If your credit card has a grace period, you may avoid credit card interest charges by paying your statement balance in full each billing cycle. You may also want to avoid credit card cash advance transactions if you’re trying to avoid credit card interest charges.

fizkes/istockphoto

The average American credit card debt balance increased 11.5% year-over-year from August 2022 to August 2023, according to TransUnion, one of the big three credit bureaus. It identified inflation as a key driver behind balance growth.

You can calculate the national credit card debt average by taking the total balance across all credit card accounts ($1.03 trillion in Q2 2023) and dividing it by the number of U.S. consumers with a credit card account balance (165.3 million).

TransUnion uses a different methodology — a stratified random sample of 5 million consumers — to calculate average credit card debt by state. The $6,039 average credit card balance in August 2023 is a measurement of credit card debt under TransUnion’s calculation method. Cardholders who pay their credit card balance in full each billing cycle may avoid interest charges on new purchases.

jacoblund/istockphoto

Consumers in all risk tiers use credit cards to buy goods and services. The below table highlights the average American credit card balance by risk tier, according to TransUnion data:

Average credit card balance per consumer in August 2023 by Risk Tier:

- Super prime (781-850): $3,868

- Prime plus (721-780): $7,396

- Prime (661-720): $8,721

- Near prime (601-660): $8,699

- Suprime (300-600): $5,034

Credit card debt exists across all risk scores, but cardholders with bad credit are more likely to experience serious delinquency.According to TransUnion’s credit card debt data by risk tier (August 2023):

- 19.14% of subprime cardholders fell 90+ days past due

- 1.20% of near prime cardholders fell 90+ days past due

- 0.20% of prime cardholders fell 90+ days past due

- 0.01% of prime plus cardholders fell 90+ days past due

- 0% of super prime cardholders fell 90+ days past due

tolgart/istockphoto

While it’s interesting to learn the average credit card debt in the U.S., it doesn’t help you much when you’re struggling to pay down your own credit card debt.

Most credit cards are unsecured without collateral. This means credit card account holders typically are not required to make a security deposit. Failing to pay and defaulting on your credit card bills can severely damage your credit.

When you make transactions on a credit card, the transaction activity represents an unpaid debt that you’ll eventually have to repay as fast or as slow as you wish. If you’re facing credit card debt challenges, below we highlight some ways you may manage your debt.

JulPo/istockphoto

Here are three tips that may help you reduce credit card debt:

1. Using Balance Transfer Credit Cards

Some credit card issuers offer new applicants 0% introductory APR financing on balance transfers. This enables you to transfer existing credit card debt to a new card and gives you a break from incurring interest charges. And when you transfer balances from multiple cards, you’re consolidating your debt as well, which can make it easier to stay on top of payments since you’ll have just one instead of multiple.

Promotional APR offers last a minimum of six months and can extend up to 21 months. Just note that you may incur a balance transfer fee, which is typically 3% to 5% of the amount transferred. With the way credit cards work usually, the balance transfer fee is added to the balance of the new account.

The key to utilizing a balance transfer credit card is to pay a portion of your remaining balance each month before you resume swiping at places accepting credit card payments. This ensures that you have the entire balance paid off by the time the promotional rate expires and the standard rate resumes.

2. Getting a Personal Loan to Consolidate Debt

Another option to pay off credit card debt is to use a personal loan to consolidate debt. Personal loans are typically installment loans with fixed monthly payments and a fixed repayment schedule. Approval typically is based on your personal credit history and credit score.

If you have good or excellent credit (661+ VantageScore® 4.0), you might be able to qualify for a loan with a lower interest rate than your current credit cards have. When you receive funding from a personal loan, you can use it to pay off your credit card debt, which may have higher interest rates — especially if your APR is above the average credit card interest rate.

3. Receiving Credit Counseling

You could also look for a credit counseling service that can offer advice on how to manage your credit card debt and pay it off. There are nonprofit credit counselors who can help you to choose from one of many possible solutions, such as credit card debt forgiveness.

Credit counseling can also offer general financial education, such as explanations of important credit card definitions and tips on budgeting. Counseling can take place in person, online, or over the phone. You may be able to find nonprofit credit counseling services through a university, military base, credit union, or housing authority.

Beware that some vendors may not be legitimate credit counselors. The U.S. Department of Justice maintains a list of approved credit counseling agencies by state. Most of the reputable credit counseling agencies are nonprofit organizations that offer services at local offices, online, or on the phone, according to the Federal Trade Commission.

mixetto/istockphoto

Whether you have a large or small amount of credit card debt, paying that balance off as soon as possible may reduce or eliminate your interest costs. When choosing a credit card, consider the card’s standard interest rate, as well as any promotional financing offered on new purchases, balance transfers, or both.

This article originally appeared on SoFi.com and was syndicated by MediaFeed.org.

Lantern By

SoFiSoFi receives compensation in the event you obtain a loan, financial product, or service through the Lantern marketplace. This Lantern website is owned by SoFi Lending Corp., a lender licensed by the Department of Financial Protection and Innovation under the California Financing Law, license number 6054612; NMLS number 1121636. (www.nmlsconsumeraccess.org). This site is NOT owned and operated by SoFi Bank. Loans, financial products, and services may not be available in all states.

All rates, fees, and terms are presented without guarantee and are subject to change pursuant to each provider’s discretion. There is no guarantee you will be approved or qualify for the advertised rates, fees, or terms presented. The actual terms you may receive depends on the things like benefits requested, your credit score, usage, history and other factors.

*Check your rate: To check the rates and terms you may qualify for, Lantern and/or its network lenders conducts a soft credit pull that will not affect your credit score. However, if you choose a product and continue your application, the lender(s) you choose will request your full credit report from one or more consumer reporting agencies, which is considered a hard credit pull and may affect your credit.

All loan terms, including interest rate, and Annual Percentage Rate (APR), and monthly payments shown on this website are from lenders and are estimates based upon the limited information you provided and are for information purposes only. Estimated APR includes all applicable fees as required under the Truth in Lending Act. The actual loan terms you receive, including APR, will depend on the lender you select, their underwriting criteria, and your personal financial factors. The loan terms and rates presented are provided by the lenders and not by SoFi Lending Corp. or Lantern. Please review each lender’s Terms and Conditions for additional details.

Many factors affect your credit scores and the interest rates you may receive. SoFi is not a Credit Repair Organization as defined under federal or state law, including the Credit Repair Organizations Act. SoFi does not provide “credit repair” services or advice or assistance regarding “rebuilding” or “improving” your credit record, credit history, or credit rating. For details, see the FTC’s website on credit (consumer.ftc.gov)

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.¹

SoFi’s Insights tool offers users the ability to connect both SoFi accounts and external accounts using Plaid, Inc.’s service. When you use the service to connect an account, you authorize SoFi to obtain account information from any external accounts as set forth in SoFi’s Terms of Use. SoFi assumes no responsibility for the timeliness, accuracy, deletion, non-delivery or failure to store any user data, loss of user data, communications, or personalization settings. You shall confirm the accuracy of Plaid data through sources independent of SoFi. The credit score provided to you is a VantageScore® based on TransUnion® (the “Processing Agent”) data.

Personal Loan

SoFi Lending Corp. (“SoFi”) operates this Personal Loan product in cooperation with Engine by MoneyLion. If you submit a loan inquiry, SoFi will deliver your information to Engine by MoneyLion, and Engine by MoneyLion will deliver to its network of lenders/partners to review to determine if you are eligible for pre-qualified or pre-approved offers. The lenders/partners receiving your information will also obtain your credit information from a credit reporting agency. If you meet one or more lender’s and/or partner’s conditions for eligibility, pre-qualified and pre-approved offers from one or more lenders/partners will be presented to you here on the Lantern website. More information about Engine by MoneyLion, the process, and its lenders/partners is described on the loan inquiry form you will reach by visiting our Personal Loans page as well as our Student Loan Refinance page. Click to learn more about Engine’s Licenses and Disclosures, Terms of Service, and Privacy Policy.Personal loan offers provided to customers on Lantern do not exceed 35.99% APR. An example of total amount paid on a personal loan of $10,000 for a term of 36 months at a rate of 10% would be equivalent to $11,616.12 over the 36 month life of the loan.

Student Loan RefinanceSoFi Lending Corp. (“SoFi”) operates this Student Loan Refinance product in cooperation with Engine by MoneyLion. If you submit a loan inquiry, SoFi will deliver your information to Engine by MoneyLion, and Engine by MoneyLion will deliver to its network of lenders/partners to review to determine if you are eligible for pre-qualified or pre-approved offers. The lenders receiving your information will also obtain your credit information from a credit reporting agency. If you meet one or more lender’s and/or partner’s conditions for eligibility, pre-qualified and pre-approved offers from one or more lenders/partners will be presented to you here on the Lantern website. More information about Engine by MoneyLion, the process, and its lenders/partners is described on the loan inquiry form you will reach by visiting our Personal Loans page as well as our Student Loan Refinance page. Click to learn more about Engine’s Licenses and Disclosures, Terms of Service, and Privacy Policy.

NOTICE: The debt ceiling legislation passed on June 2, 2023, codifies into law that federal student loan borrowers will be reentering repayment. The US Department of Education or your student loan servicer, or lender if you have FFEL loans, will notify you directly when your payments will resume For more information, please go to https://docs.house.gov/billsthisweek/20230529/BILLS-118hrPIH-fiscalresponsibility.pdf https://studentaid.gov/announcements-events/covid-19

If you are a federal student loan borrower considering refinancing, you should take into account the new income-driven payment plan, SAVE, which replaces REPAYE, seeks to make monthly payments more affordable, and offers forgiveness of balances that were originally $12,000 or lower after 120 payments, among other improvements. Also, please note that once you refinance federal student loans you will no longer be eligible for current or future flexible payment options available to federal loan borrowers, including but not limited to income-based repayment plans, such as SAVE, or extended repayment plans.

Auto Loan RefinanceAutomobile refinancing loan information presented on this Lantern website is from Caribou, AUTOPAY, Engine by MoneyLion, and each of Engine’s partners (along with their affiliated companies). Caribou, AUTOPAY, and Engine by MoneyLion pay SoFi compensation for marketing their products and services on the Lantern site.

Auto loan refinance information presented on this Lantern site is indicative and subject to you fulfilling the lender’s requirements, including but not limited to: credit standards, loan size, vehicle condition, and odometer reading. Loan rates and terms as presented on this Lantern site are subject to change when you reach the lender and may depend on your creditworthiness, consult with the lender for more details. Additional terms and conditions may apply and all terms may vary by your state of residence.

Secured Lending DisclosureTerms, conditions, state restrictions, and minimum loan amounts apply. Before you apply for a secured loan, we encourage you to carefully consider whether this loan type is the right choice for you. If you can’t make your payments on a secured personal loan, you could end up losing the assets you provided for collateral. Not all applicants will qualify for larger loan amounts or most favorable loan terms. Loan approval and actual loan terms depend on the ability to meet underwriting requirements (including, but not limited to, a responsible credit history, sufficient income after monthly expenses, and availability of collateral) that will vary by lender.

BankingSoFi Lending Corp. (“SoFi”) operates this website in cooperation with Engine by MoneyLion presenting promotions for products and services offered by other banks, lenders, and financial institutions. If you select a promotion above, you will be connected to the website of the company offering the product. The promotions presented on this site are from companies that pay SoFi and Engine by MoneyLion compensation for marketing their products and services. This may affect whether a provider is featured on this site and could affect the order of presentation. Lantern and Engine by MoneyLion do not include all providers in the market or all of their available offerings. Click to learn more about Engine’s Licenses and Disclosures, Terms of Service, and Privacy Policy.

miniseries/istockphoto

Tinpixels/istockphoto

Featured Image Credit: gorodenkoff/ iStock.