As a small business owner, it’s up to you to learn how to do payroll and select the best pay period type for your employees. From daily and monthly to biweekly and semimonthly, employee pay periods can be tailored to meet the payroll needs of your team and business.

Read our guide to learn about the types of pay periods, the seven factors to determine which one is right for your business, and what a real-world example of a salary broken down by each pay period looks like.

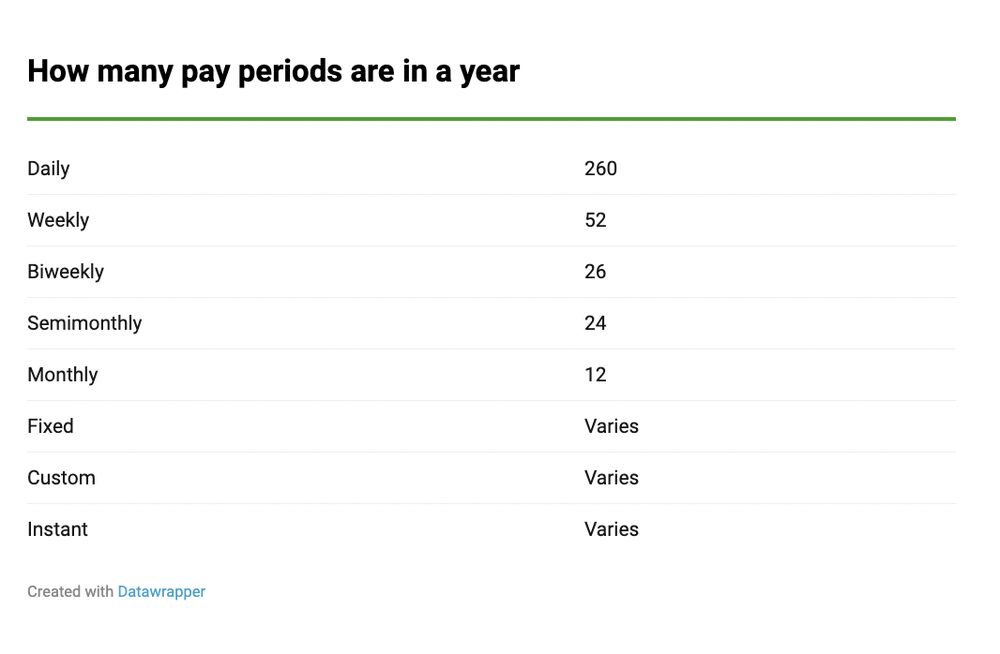

Types of pay periods

There are various types of pay periods, but the most common are weekly, biweekly, monthly, and semimonthly. Each type will have a different amount of payroll periods in a year. The number of pay periods that will work for your business will depend on the payroll schedule, the types of employees you’re paying, and whether or not they receive overtime. Let’s look at each type.

Daily pay periods

260 pay periods a year

Daily pay periods are a type of pay period that allows employees to access their earned wages on a daily basis. There are around 260 business days in a year, but the amount of pay periods can vary depending on what days employees work.

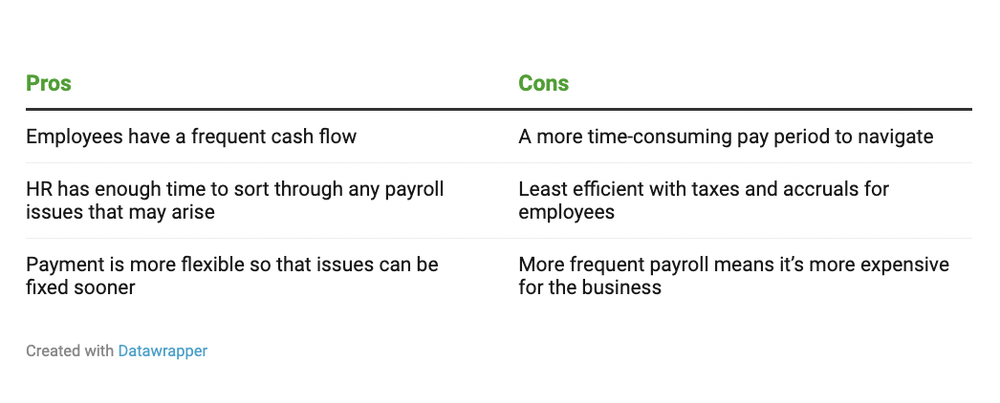

Weekly pay periods

52 pay periods a year

An employee with weekly pay will receive 52 paychecks a year. Hourly employees and part-time employees are typically paid weekly. A weekly pay period is ideal for employees who tend to work overtime or whose work schedules change every week. However, a more frequent payroll schedule can also be more expensive for the business.

With this pay period, employees will record their hours for the week and submit a timesheet at the end of the workweek. They will then be paid the following week because it gives the payroll clerk time to make adjustments. Some employees enjoy a weekly pay period because it’s a more consistent cash flow.

Biweekly pay periods

26 pay periods a year

An employee who is paid biweekly will typically receive 26 paychecks a year. Employees paid biweekly can either be hourly or salaried. Biweekly pay periods are more cost-effective than weekly payroll, but processing payroll for months with three pay periods can be confusing.

Employers who use this payroll schedule can benefit from a more cost-efficient way to pay their employees than weekly pay periods. However, pay periods can quickly become confusing.

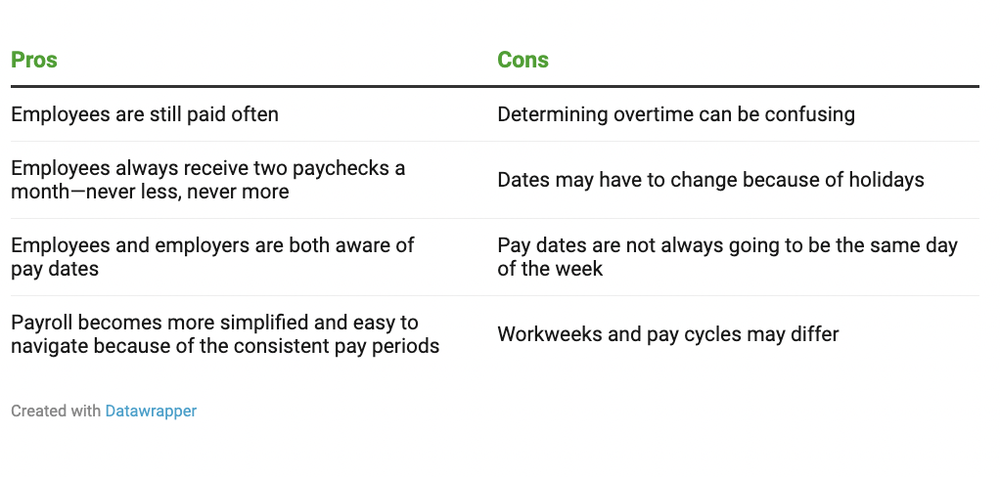

Semimonthly pay periods

24 pay periods a year

An employee who is paid semimonthly will receive 24 paychecks a year. Employees with semimonthly salaries will typically receive payments on the first and 15th of each month. Semimonthly payroll works best for salaried employees who have a consistent schedule.

Semimonthly payroll is easy for both the employer and the employee. It’s easy for the employer to calculate employee costs. However, the semimonthly pay period can be confusing for hourly workers if overtime needs to be applied.

Monthly pay periods

12 pay periods a year

An employee who is paid monthly will receive 12 paychecks a year. Monthly pay periods typically only work for salaried employees. Employees with monthly salaries usually receive payment on either the first or last day of the month.

Monthly payroll is the most cost-effective of the bunch and is the easiest to calculate, especially when taxes are concerned. Employers can also rely on the consistency of this payroll schedule.

Fixed pay periods

A fixed pay period is a method of paying employees where they receive the same amount of money for each pay cycle, regardless of how many hours they work or how much they produce.

This is great for a variable pay period, where employees are paid based on their performance, such as commission, bonuses, or overtime. Employers can also show their employees that they value them by offering consistent yet flexible pay.

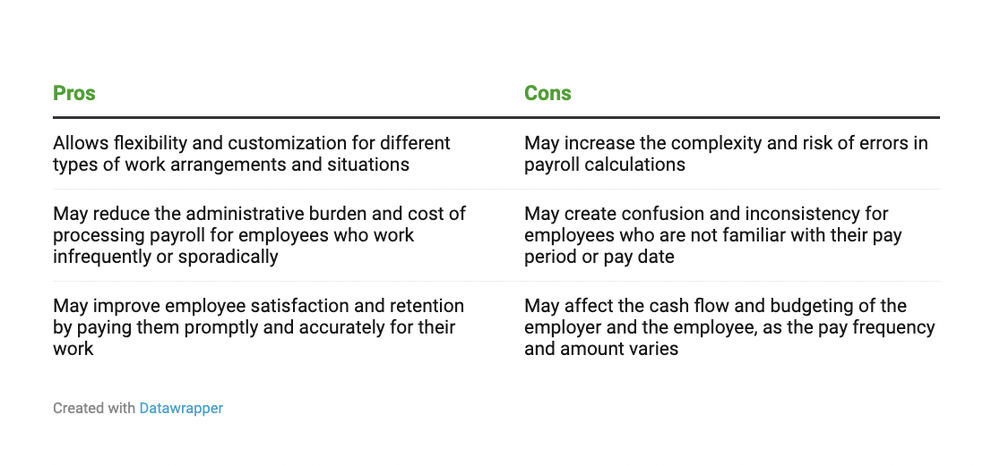

Custom pay periods

A custom pay period is a type of pay schedule that is not fixed or recurring but rather determined by specific circumstances. For example, a custom pay period may occur when an employee resigns or is terminated, and the employer needs to calculate the final wages and deductions for that employee.

A custom pay period may also be used for seasonal employees, employees who work on a project basis, or employees with irregular hours. This pay period can help employers create customized pay plans for their employees on a case-by-case basis.

Instant pay periods

Instant pay period is a term that refers to a system where employees can access their earned wages before their scheduled payday. This means that workers do not have to wait for weeks or months to receive their income but can withdraw it as soon as they complete their work hours. This pay period can potentially reduce administrative costs and burdens for employers.

Pay period examples

Consider if you have an employee who earns $50,000 a year. Here is how their payments might breakdown across each pay period — and how many pay periods to expect:

- Daily: $192 a day

- Weekly: $962 a week

- Biweekly: $1,923 every other week

- Semimonthly: $2,083 twice a month

- Monthly: $4,166 a month

- Fixed: Fixed amount at agreed-upon intervals

- Custom: Customized pay periods and amounts

- Instant: Instant payments for every workday

Although monthly paychecks may be larger, they’ll be less frequent than other pay period options. Consider these factors when selecting your pay period.

7 factors to determine which pay period is right for your business

One of the most important decisions you have to make as a business owner is how often to pay your employees. The pay period you choose can affect your cash flow, payroll costs, employee satisfaction, and compliance with labor laws.

There is no one-size-fits-all answer to this question, but some of the factors you should consider are:

- Employment laws and regulations: Consider any local labor laws that could affect your payroll schedule choices.

- Workweeks: If your employees don’t work traditional workweek schedules, a more customized payroll option may benefit your team better.

- Payroll costs: Calculate the payroll costs associated with each type of payroll and determine which one your small business has the budget for.

- Overtime: Factor in how your business will incorporate overtime pay into your payroll schedule to determine which type is best for your team.

- Employee needs: Consider if your employees have specific payment needs or desired payroll schedules in mind.

- Withholdings: Ask yourself if a payroll schedule will align with your employees’ tax withholdings.

- Reporting: If your business already follows a set reposting schedule, consider aligning your pay periods with your reporting periods.

By weighing these factors carefully, you can choose a pay period that works best for your business and your employees.

This article originally appeared on the QuickBooks Resource Center and was syndicated by MediaFeed.org.

More from MediaFeed:

The ultimate guide to prepping your taxes

It’s that time of year again: Typically, by midnight on April 15, taxpayers must e-file or mail their federal and, if applicable, state tax returns for the previous calendar tax year without penalty. Well before the deadline, though, it’s wise to do your prep work, hunting down the necessary documents, finding a tax pro or software to help you through the process, and learning about any new tax deductions or credits you might be eligible for.

It can definitely be a challenge to get organized, but by following certain steps, you can be ready to file properly and on time. Here, we’ll help you along with important tips, including:

- When is tax-filing season?

- How do you prepare for tax season?

- Should you hire a tax pro?

- Which tax documents do you need?

- By when do you need to file taxes?

fizkes / iStock

Tax season typically begins in January. So, for tax year 2022, January 2023 marks the start of the season. You should receive a Form W-2 by January 31st or, with any mail delay, soon thereafter. The same deadline applies to certain 1099-MISC forms for independent contractors. Each financial institution that paid you at least $10 of interest during the year must send you a copy of the 1099-INT by January 31st as well.

Waiting until the last minute to prepare for tax filing is never advisable. If taxpayers work for one employer, their taxes may not be complicated, but if they have side gigs or they’re self-employed, tax returns can take a while to fill out.

The due date for individuals to file their taxes is usually April 15th of a given year or, if that falls on a weekend, the next following weekday. However, Tax Day is Tuesday, April 18, 2023, for tax year 2022. This is due to the fact that the 15th is a Saturday and the observance of the Emancipation Day holiday in Washington, D.C. on the 17th. For this reason, the date that returns are due has moved forward an additional day to the 18th.

Before filing, here’s how to prepare for tax season.

Piotrekswat/istockphoto

Taxpayers can either prepare and file their taxes on their own or hire a professional. If they choose the latter, they can go to a tax preparation service like H&R Block or contact a local accountant or other tax pro. Some people feel more secure with a professional who can guide them through the process, know the latest deductions, and perhaps help them avoid IRS audit triggers.

The costs for a professional vary, and the more complicated a return is, the higher the costs will be.

The IRS has a tool where taxpayers can find a tax preparer near them with credentials or select qualifications. Doing so will mean paying a fee. How much? According to the National Society of Accountants,in 2020-2021, the average price tag for preparing and filing an itemized Form 1040 with Schedule A, Schedule C (this is for sole proprietors of a business), plus a state tax return, was a not insignificant $515. For a simpler return, the average fee is typically closer to $200.

Or you could use software which is likely to cost less but require a greater investment of your time. For instance, TurboTax’s 2022 prices range from $59 and up, depending on whether you need additional features, like those for people who run their own businesses.

Daenin Arnee/istockphoto

You might also want to try this alternative: IRS Free File lets you prepare and file your federal income tax online for free. There are two options, based on income.

- You can file on an IRS partner site if your adjusted gross income was $73,000 or less. This is a guided preparation, and the online service does all the math.

- Those with income above $73,000 who know how to prepare paper forms and can do basic calculations can fill out and file electronic federal tax forms. (There is no state tax filing with this option, however.)

fizkes/istockphoto

Gathering the right papers is an important part of preparing for tax season. By the end of January, you should have received tax documents from employers, brokerage firms, and others you did business with. They include a W-2 for a salaried worker and what are known as 1099s for freelancers and contract workers.

Employers will send the documents in the mail or electronically.

Investors might receive these forms:

- 1099-B, which reports capital gains and losses

- 1099-DIV, which reports dividend income and capital gains distributions

- 1099-INT, which reports interest income

- 1099-R, which reports retirement account distributions.

Other 1099 forms include:

- 1099-MISC, which reports payments in lieu of dividends

- 1099-Q, which reports distributions from education savings accounts and 529 accounts.

If taxpayers won anything while gambling, they’ll need to fill out Form W-2G. If they paid at least $600 in mortgage interest during the year, they’ll receive Form 1098, whose information can be used to claim a mortgage interest tax deduction.

A list of income-related forms can be found on the IRS website.

Last year’s federal return, and, if applicable, state return could be good reminders of what was filed last year and the documents used. That can help you pinpoint any missing tax documents.

Larry_Reynolds/istockphoto

Wondering whether to take the standard deduction or itemize deductions? The higher figure is the winner.

The vast majority of Americans claim the standard deduction, the number subtracted from your income before you calculate the amount of tax you owe.

For tax year 2022, the standard deductions are:

- $12,950 for a single filer

- $25,900 for a married couple filing jointly

- $12,950 for a married couple filing separately

- $19,400 for a head of household.

Those age 65 or older or who are blind can claim an additional standard deduction of $1,400 or $1,750 if using the single or head of household filing status.

Individuals interested in itemizing tax deductions can look into whether they’re eligible for a long list of deductions like a home office (and, if eligible, whether to use the simplified option for computing the deduction), education deductions, healthcare deductions, and investment-related deductions.

The IRS notes that you may benefit from itemizing deductions if any of these apply:

- Don’t qualify for the standard deduction

- Had large uninsured medical or dental expenses during the year

- Paid interest and taxes on your home

- Had large uninsured casualty or theft losses

- Made large contributions to qualified charities

- Have total itemized deductions that are more than the standard deduction to which you otherwise are entitled.

Then there are tax credits, a dollar-for-dollar reduction of the income tax you owe. So if you owe, say, $1,500 in federal taxes but are eligible for $1,500 in tax credits, your tax liability is zero.

There are family and dependent credits, healthcare credits, education credits, homeowner credits, and income and savings credits. Taxpayers can see the entire tax credits and deductions list on the IRS website.

designer491/istockphoto

Details count (a lot) when filing your return, and one important point to include is the Social Security number for any children and other dependents. If you omit this, you may lose any dependent credits, like the Child Tax Credit, that you qualify for.

Also know that if you are divorced, only one parent can claim children as dependents.

FG Trade/istockphoto

On the subject of children, tax time is a good time to review and update beneficiary designations. While it won’t change your tax-filing calculations, it will potentially reduce the tax burden your beneficiaries may pay on what they inherit after you die.

Moyo Studio/istockphoto

As you get ready for tax filing, it’s wise to check your progress towards your retirement fund (hopefully you have one). Money that you put into a 401(k), 403(b), or other tax-deferred account reduces your taxable income. In other words, it helps minimize your tax bill. The contributions you make aren’t taxed until you decide to withdraw funds.

If you feel you can afford to contribute more, know that for 2022, the limits for tax deferred contributions are $20,500 for 401(k) accounts, with an additional $6,500 for catch-up contributions for taxpayers who are age 50 or older. Check the IRS website for more details.

DNY59/istockphoto

Another tax-filing tip: If you’ve reached retirement age, make sure you take any distributions that are necessary. For instance, if you’ve celebrated your 72nd birthday and have funds in a 401(k) or IRA, you must make your RMD, or required minimum distribution, by December 31st, or face a penalty of 50% of the RMD total. That’s a pitfall most people would want to avoid.

andreswd/istockphoto

Taxpayers who do not have taxes withheld from their paychecks can pay estimated taxes every quarter to avoid owing a big chunk of change come Tax Day.

In 2022, quarterly estimated taxes were due on April 18th, June 15th, and September 15th, with the fourth due early in the next year, on January 17th, 2023.

SrdjanPav/istockphoto

What happens if you discover, at tax-filing time, that you can’t pay the full amount you owe? One option is to pay as much as you can and then set up a payment plan with the IRS for the rest. This is a method that gives you a longer time frame in which to pay what you owe. Depending on whether you have a short-term or long-term IRS payment plan, there may be setup fees.

mareesw/istockphoto

Here’s an important tip: prioritize filing electronically, especially if you anticipate receiving a refund. Electronic returns can typically be processed more quickly than paper ones, which means you’ll get your infusion of cash that much sooner.

Another benefit of filing this way is that your return is much less likely to have errors. Electronic returns tend to have just 1% with errors. But for “hard copy” paper returns, that number ratchets up to about 20% with mistakes.

NoDerog/istockphoto

What if you don’t quite have your act together and your tax-filing materials ready to roll on time? It happens. If you need more time to prepare your federal tax return, you can electronically request an extension until October 16th, 2023, to file a return. This involves filing IRS Form 4868.

To get the extension, you must estimate your tax liability and pay any amount due by April 15th to avoid penalties. That’s right: Getting an extension to file doesn’t mean you shouldn’t be paying your taxes in a timely way.

coldsnowstorm/istockphoto

Filing a tax return can be enough to keep you busy without worrying about getting scammed. But unfortunately, there are fraudsters out there, trying to take advantage of the season. For instance, you might get an email, phone call, or even a text message that says it’s from the IRS. They may say there’s an issue with a return of yours and that they need to speak with you ASAP. Don’t fall for it: The only way the IRS will ever communicate with you is via U.S. mail, unless you are involved in some kind of litigation with them.

designer491/istockphoto

Now that you’ve learned more about tax filing, here are some reasons to get started sooner rather than later on your return.

- Avoid deadline anxiety. For some people, procrastination can lead to a lot of stress as the filing date approaches. They risk having to pull the proverbial all-nighter to get their return done on time or wind up blowing the deadline. By starting sooner, you can chip away at the process of pulling materials together and completing forms and breathe a little easier.

- Dodge processing delays. If you file earlier, you are likely to slip in before the deluge of returns hits the IRS’ offices. You might even get your refund (if you’re due one) sooner.

- Take the time to plan. Perhaps you know you’re going to owe money. Or you’re not sure if that’s the case. In either scenario, starting the tax-filing process earlier will give you time to see what you may owe and then figure out how to pay any funds that are due.

Milan_Jovic/istockphoto

“Tax prep” isn’t a phrase signaling that big fun is on the way, but putting off the inevitable isn’t the best choice. Prepare for tax season as early as possible by gathering documents and information, choosing a preparer or getting ready to DIY, and learning about tax credits and deductions.

Learn More:

This article originally appeared on SoFi.com and was syndicated by MediaFeed.org.

Please understand that this information provided is general in nature and shouldn’t be construed as a recommendation or solicitation of any products offered by SoFi’s affiliates and subsidiaries. In addition, this information is by no means meant to provide investment or financial advice, nor is it intended to serve as the basis for any investment decision or recommendation to buy or sell any asset. Keep in mind that investing involves risk, and past performance of an asset never guarantees future results or returns. It’s important for investors to consider their specific financial needs, goals, and risk profile before making an investment decision.

The information and analysis provided through hyperlinks to third party websites, while believed to be accurate, cannot be guaranteed by SoFi. These links are provided for informational purposes and should not be viewed as an endorsement. No brands or products mentioned are affiliated with SoFi, nor do they endorse or sponsor this content.

Communication of SoFi Wealth LLC an SEC Registered Investment Advisor

SoFi isn’t recommending and is not affiliated with the brands or companies displayed. Brands displayed neither endorse or sponsor this article. Third party trademarks and service marks referenced are property of their respective owners.

Communication of SoFi Wealth LLC an SEC Registered Investment Adviser. Information about SoFi Wealth’s advisory operations, services, and fees is set forth in SoFi Wealth’s current Form ADV Part 2 (Brochure), a copy of which is available upon request and at www.adviserinfo.sec.gov. Liz Young is a Registered Representative of SoFi Securities and Investment Advisor Representative of SoFi Wealth. Her ADV 2B is available at www.sofi.com/legal/adv.

pcess609/istockphoto

damircudic/istockphoto

Featured Image Credit: DepositPhotos.com.