Going Halfsies

The second half of 2023 is underway, and another earnings season is fast approaching. The first half seems to have flown by, despite a tumultuous spring and regional bank crisis, and many investors are still scratching their heads about what went on.

The divisiveness between so-called “bulls” and “bears” grew wider, almost resembling a political landscape where each side looked at the other with anger and resentment, unable to find common ground. Understandably so, given the plethora of conflicting data — not the least of which is the unexpectedly feverish stock market rally in the face of leading economic indicators and bond market signals that are clearly waving a red flag.

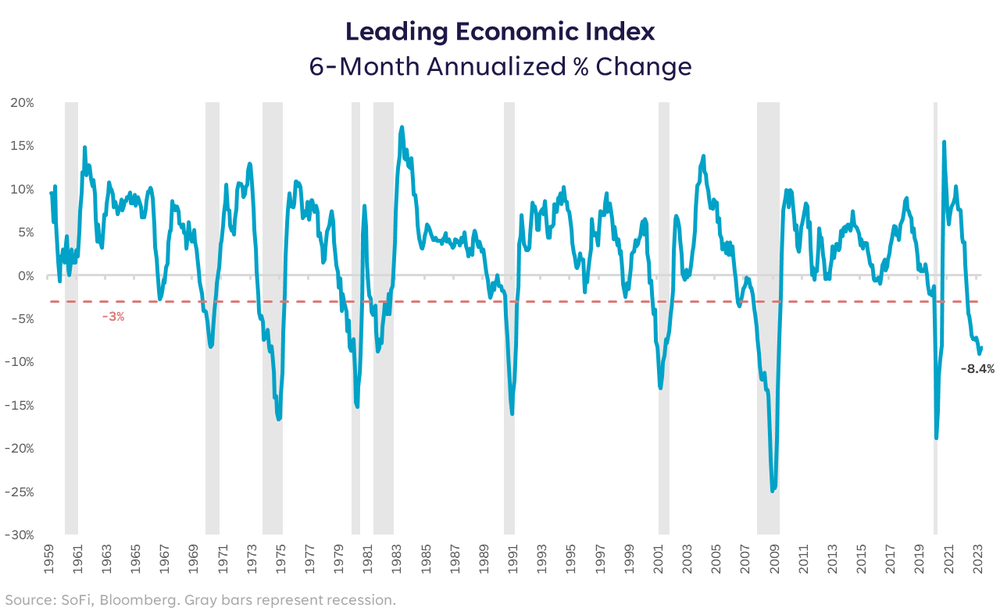

In fact, never since the data series began in 1959 has the annualized 6-month change in the Leading Economic Index dropped below 3% without a recession to follow. That measure currently sits at -8.4%.

Yet the coincident indicators (the ones that don’t signal a macro shift ahead of time, but react at the same time as said shift) have been durable. Data sets such as payroll employment, industrial production, and personal income are holding up and fighting the theory that fast rate hikes cause clear economic destruction.

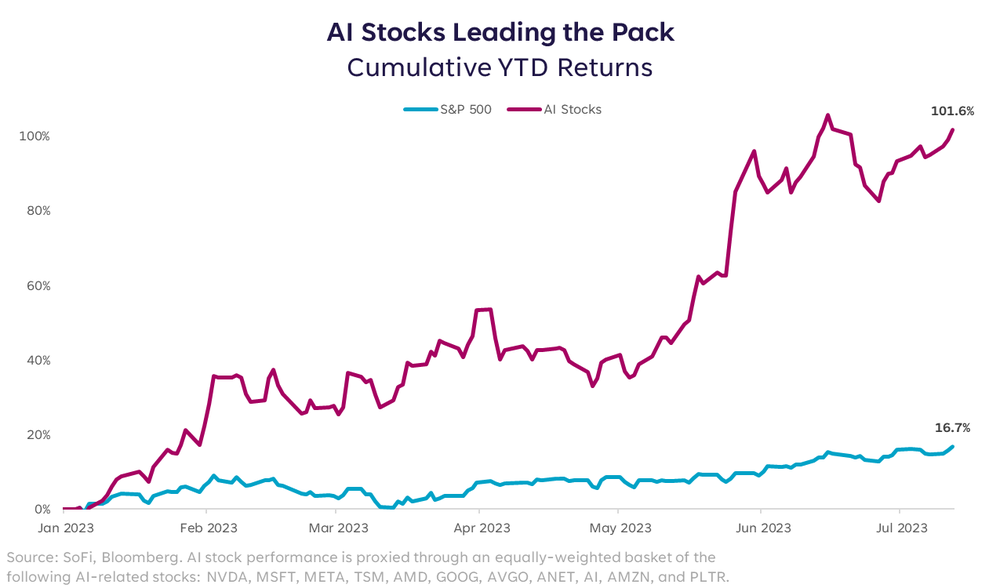

On top of this, the first half of 2023 saw an enthusiasm around AI that drove prices of AI-related stocks up at an astonishing pace. The returns of most of the remaining stocks in the S&P 500 paled in comparison, but investor sentiment and excitement around this new theme was contagious.

A Watched Pot…

You know how that statement ends. We’ve been watching the recession and drawdown pot for what seems like forever, and not a bubble has boiled to the top.

Is it just taking longer, or is it never going to happen? If I knew the answer to that question with certainty, I could finish this article right here and be on with my day. Unfortunately, or perhaps fortunately for entertainment purposes, I don’t know. What I do know is that some of the market-based relationships are out of whack, and things don’t stay out of whack forever.

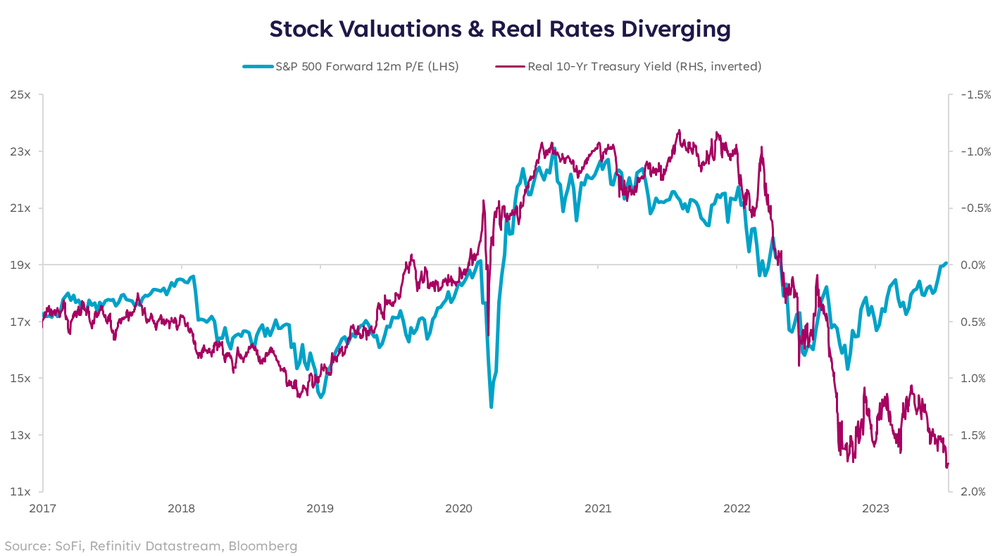

For example, when rates rise, so does the discount rate on companies’ future cash flows, which mathematically pressures their present value. In other words, higher rates make future earnings less valuable in today’s dollars, thus investors are typically less willing to pay up for them. But the opposite has been true YTD.

The chart below shows the expansion in the S&P 500 price-to-earnings (P/E) multiple while the real yield on 10-year Treasurys remained high and even rose further (inverted here to show the typical relationship vs. the current divergence). (Learn more at Home Affordability Calculator)

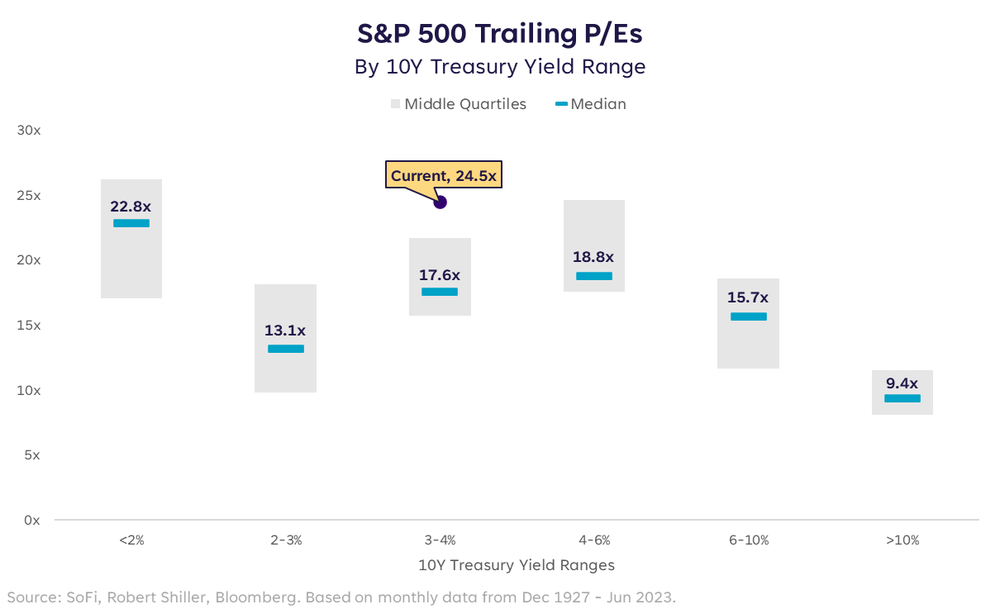

Not only have valuations risen, but they currently sit above their 5-, 10-, and 15-year averages, making them look expensive by historical standards, and by the nature of the current environment.

Using trailing P/Es (because they offer a longer historical perspective), the current 10-year yield range (between 3-4%) suggests a median trailing P/E of 17.4x. As of this writing, the trailing P/E sits well above the median, and even well above the middle range, at 24.5x. Tough to argue that it looks cheap or attractive as an entry point.

New bull markets don’t typically start from already elevated P/E ratios, which makes me continuously skeptical of this rally’s staying power. Nevertheless, it carries on, and the phrase “don’t fight the tape” plays on repeat in all of our heads.

The volatility index (VIX) hit a 3-year low of 12.91 at the end of June, further amplifying the calm and positive market tone. But some might say it also further amplified the tone of complacency, which is not usually a set-up for continued upside. And although we should heed the warning to not fight the tape, the phrase that’s said louder and perhaps with more proven power is still, “don’t fight the Fed.”

Fight Club

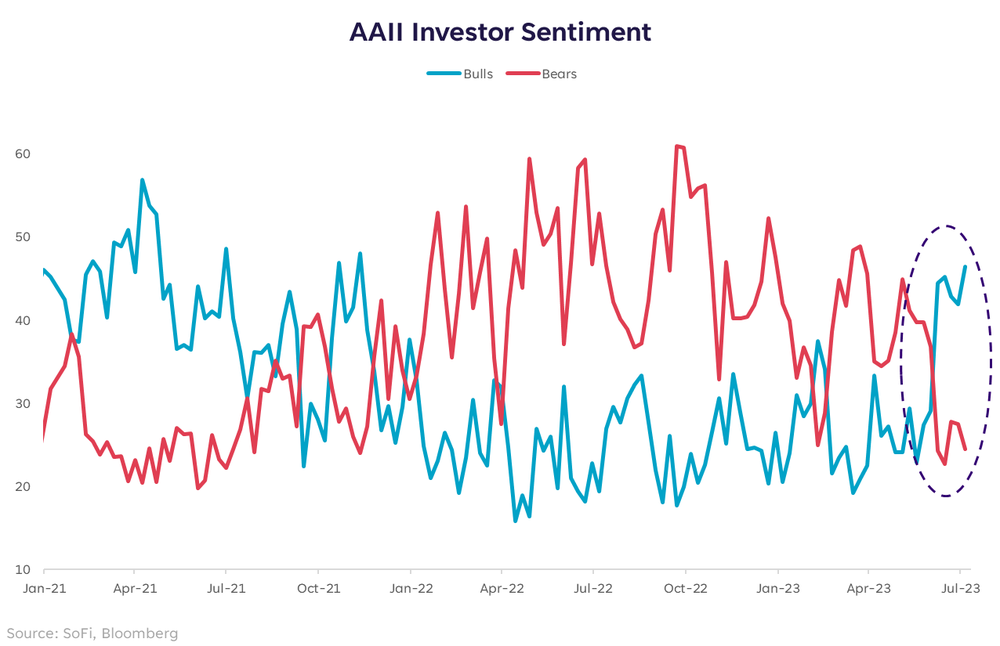

The title of my 2023 annual outlook was “This Ends One Way or Another” and it’s clear that it hasn’t ended yet. As each month goes by without a right-sizing of valuations, or an obvious and wide-reaching negative effect of monetary tightening, it becomes more and more tempting to wonder if it may not ever end the way I expect it to. And I am not alone, as evidenced by the massive flip in investor sentiment over recent months. (Learn more at Personal Loan Calculator)

The bulls and bears keep fighting, with bulls not fighting the tape and bears not fighting the Fed. During this period, I’m also reminded of a warning that’s often flagged by chartists to notice and be wary of extremes. Much like large divergences, extremes don’t last forever.

Although the absolute level of bulls vs. bears in the chart above doesn’t appear to be at extremes, the almost instantaneous reversal in the two is quite extreme. Generally, large and swift moves can be followed by large and swift moves back in the other direction as markets and investors attempt to settle on some sort of middle ground.

Respect the Cycle

I’m bordering on overusing that phrase, but I stand by the statement that we must respect the cycle. It’s true there was no clear recession and no lasting nor significant drawdown in the first half. It’s also true that I absolutely did not expect the strong returns we’ve seen over the first six months of the year.

But liquidity is still shrinking, inflation is falling but has taken a meaningful bite out of many Americans’ finances, and the Fed is on a mission to send hawkish messages until they’re satisfied. The second half of this year is likely to see few, if any, additional rate hikes and is likely to mark the beginning of a new phase of monetary policy — one that’s characterized by holding rates high and waiting for the first signs of a cut. It’s also one I don’t think we know how to finish.

This is my 19th year in the biz, and it never ceases to amaze me how unpredictable and fascinating markets can be. I suppose the element of surprise is one of the main draws to this industry, which can be an intoxicating adrenaline rush, and a never-satiated thirst to figure it all out.

The lags may be longer this time, the catalysts may be different, and the reaction function of markets to a global pandemic are unprecedented in modern times. But the economic cycle doesn’t tend to skip phases. It just keeps us guessing about their timing.

This article originally appeared on SoFi.com and was syndicated by MediaFeed.org.

Please understand that this information provided is general in nature and shouldn’t be construed as a recommendation or solicitation of any products offered by SoFi’s affiliates and subsidiaries. In addition, this information is by no means meant to provide investment or financial advice, nor is it intended to serve as the basis for any investment decision or recommendation to buy or sell any asset. Keep in mind that investing involves risk, and past performance of an asset never guarantees future results or returns. It’s important for investors to consider their specific financial needs, goals, and risk profile before making an investment decision.

The information and analysis provided through hyperlinks to third party websites, while believed to be accurate, cannot be guaranteed by SoFi. These links are provided for informational purposes and should not be viewed as an endorsement. No brands or products mentioned are affiliated with SoFi, nor do they endorse or sponsor this content.

Communication of SoFi Wealth LLC an SEC Registered Investment Advisor

SoFi isn’t recommending and is not affiliated with the brands or companies displayed. Brands displayed neither endorse or sponsor this article. Third party trademarks and service marks referenced are property of their respective owners.

Communication of SoFi Wealth LLC an SEC Registered Investment Adviser. Information about SoFi Wealth’s advisory operations, services, and fees is set forth in SoFi Wealth’s current Form ADV Part 2 (Brochure), a copy of which is available upon request and at here. Liz Young is a Registered Representative of SoFi Securities and Investment Advisor Representative of SoFi Wealth. Her ADV 2B is available at here.

3 fool-proof budgets that can work for anyone

To get an idea of what needs to go in a budget, it can be helpful to review some common monthly expenses:

- Housing: Everyone needs somewhere to live and housing comes with not just rent or mortgage payments, but insurance requirements, utilities, and maintenance costs.

- Food: Alongside groceries, many consumers like to include some room in their budget for dining at restaurants or their morning coffee order they pick up on the way to work.

- Debt: If someone has debt like student loans, auto loans, or a mortgage loan, then they also likely have minimum monthly debt payments that they need to pay or they risk incurring fines, hurting their credit score, or losing collateral.

- Medical Expenses: From health insurance premiums and copayments to prescription medications, there are a lot of expected medical expenses that recur each month.

- Fun Spending: What’s life without a little fun? While going to the movies, traveling, or buying home decor may not be necessary expenses, we all spend a little money on the things that bring us joy.

Jovanmandic/istockphoto

When it comes time to sit down and actually create a budget, these are the steps you can generally take to make a monthly plan for your money.

- Step 1. Identify all sources of income. The key to knowing what you can do with your money each month stems from knowing just how much income you have coming in. You should tally up all regular sources of income such as paychecks from a job, rent money from a property you own, or revenue from a small business or side hustle.

- Step 2. Write down ongoing necessary expenses. There are some expenses that pop up every single month no matter what. The necessary ongoing expenses such as rent, car payment, and groceries are what need to be written down first. Tally up that amount to see how much is left for other expenses. Don’t forget to include minimum debt payments here.

- Step 3. Take a cold, hard look at unnecessary spending. Pull receipts or credit card and bank statements for the past three to six months to get an idea of where any unnecessary spending is occurring. See what expenses can be cut (like pricey subscriptions or impulse purchases) to determine how much money needs to be set aside for unnecessary expenses.

- Step 4. Set financial goals and rework the budget. Once it’s clear how much extra money is available for non-necessary expenses each month, it’s a good idea to think about how some of that money can make accomplishing financial goals like paying off debt or saving for retirement easier. After setting goals, look back at the budget as a whole to see where expenses can be cut to make room for these goals.

Ridofranz/istockphoto

Everyone’s monthly budget is unique to them and their personal and financial needs, but generally, this list is an example of monthly expenses:

- Food

- Housing

- Utilities

- Phone

- Transportation

- Health care

- Pet care

- Debt payments

- Retirement contributions

- Savings contributions

- Discretionary spending

Prostock-Studio/istockphoto

There is no one right way to budget and some people find different budgeting methods work better for them. Let’s review some popular examples of monthly budgets to make it easier to visualize how budgeting can work. (Learn more atPersonal Loan Calculator).

PeopleImages/istockphoto

Some people find it easier to stick to a budget if they’re spending cash instead of using a credit or debit card to make purchases. This is why the envelope system is such a popular budgeting method.

The way this method works is the budgeter allocates a certain amount of money for major spending categories (food, gas, utilities, etc.) and then places that exact amount of cash in an envelope with the expenses written on it. Once they empty an envelope, they can no longer spend money on that type of expense unless they decide to cut another expense and put money from a different envelope into the empty one.

To boost savings, don’t forget to participate in the envelope savings challenge!

Del Henderson Jr/istockphoto

If you need help determining how to spend your money, you may prefer a budget that guides you more. With a 50/30/20 budget, 50% of take-home pay goes toward necessary expenses, 30% is spent on discretionary spending, and 20% is put towards financial goals like paying off debt early or building an emergency savings fund fast.

There’s no need to stick to this allocation exactly. For example, there’s no harm in spending a smaller percentage of take-home pay on discretionary spending and more on financial goals, but this general framework can help budgeters make an effective plan for their money without feeling deprived. (Learn more atPros and Cons of Personal Loans

https://www.sofi.com/learn/content/pros-and-cons-of-personal+loans/

).

fizkes/istockphoto

One way to stay really disciplined with budgeting is to set a zero-based budgeting plan. What this means is that every dollar of income that comes in each month is “assigned” an expense, down to the last dollar. This doesn’t mean that every dollar must be spent. Allocating money to go into a savings account counts. If someone struggles to save due to spending temptations, they may really appreciate this approach.

fizkes/istockphoto

It’s easy to give up on budgeting after getting off track, but the secret to making a budget work is a mixture of reflection, adaptability, and perseverance. Take some time at the end of the month to reflect on what went right and what went wrong. If you keep overspending in one category, but there’s frequently money left over in another category, then it may simply be time to adjust your budget.

Once someone revamps their budget, they can make easier progress toward reaching their savings goal. This is where a savings account can really come in handy. Need a new savings account? Lantern makes it easy to quickly compare interest rates, fees, and account minimums at different banks at the same time. That way, consumers can find the right savings account to help them reach their financial goals.

This article originally appeared on SoFi.com and was syndicated by MediaFeed.org.

Please understand that this information provided is general in nature and shouldn’t be construed as a recommendation or solicitation of any products offered by SoFi’s affiliates and subsidiaries. In addition, this information is by no means meant to provide investment or financial advice, nor is it intended to serve as the basis for any investment decision or recommendation to buy or sell any asset. Keep in mind that investing involves risk, and past performance of an asset never guarantees future results or returns. It’s important for investors to consider their specific financial needs, goals, and risk profile before making an investment decision.

The information and analysis provided through hyperlinks to third party websites, while believed to be accurate, cannot be guaranteed by SoFi. These links are provided for informational purposes and should not be viewed as an endorsement. No brands or products mentioned are affiliated with SoFi, nor do they endorse or sponsor this content.

Communication of SoFi Wealth LLC an SEC Registered Investment Advisor

SoFi isn’t recommending and is not affiliated with the brands or companies displayed. Brands displayed neither endorse or sponsor this article. Third party trademarks and service marks referenced are property of their respective owners.

Communication of SoFi Wealth LLC an SEC Registered Investment Adviser. Information about SoFi Wealth’s advisory operations, services, and fees is set forth in SoFi Wealth’s current Form ADV Part 2 (Brochure), a copy of which is available upon request and at here. Liz Young is a Registered Representative of SoFi Securities and Investment Advisor Representative of SoFi Wealth. Her ADV 2B is available at here.

PeopleImages/istockphoto

Larry_Reynolds/istockphoto

Featured Image Credit: monkeybusinessimages/istockphoto.