In a month where growth data came in strong & inflation data came in cool, the Federal Reserve decided to hike rates and reiterated that future decisions will depend on the totality of the data. Treasury yields rose and fell as economic data rolled in, while U.S. stock indices rose for the 5th straight month. Commodities saw prices rise the most since March 2022, which alongside a weaker US dollar helped boost emerging market stocks. Volatility in both stocks & bonds remained relatively muted for a second straight month.

Macro

- The Federal Reserve raised the fed funds rate target range to 5.25%-5.50% on Jul 26, leaving open the possibility of further rate hikes.

- 209k jobs were added in June, the first downside surprise in 15 months, while the prior two months were revised 110k.

- July CPI came in below expectations on both a headline (0.2% m/m & 3.0% y/y) and core (0.2% m/m & 4.8% y/y) basis.

- Q2 GDP rose by 2.4% q/q and the Atlanta Fed GDP Nowcast initiated Q3 tracking at +3.5%, which would be the most since Q4 2021.

- Consumer confidence rose in July according to both the University of Michigan & Conference Board, notably surpassing expectations.

- Oil prices rose by $11 (+15.8%) in July, the largest m/m increase since Jan 2022.

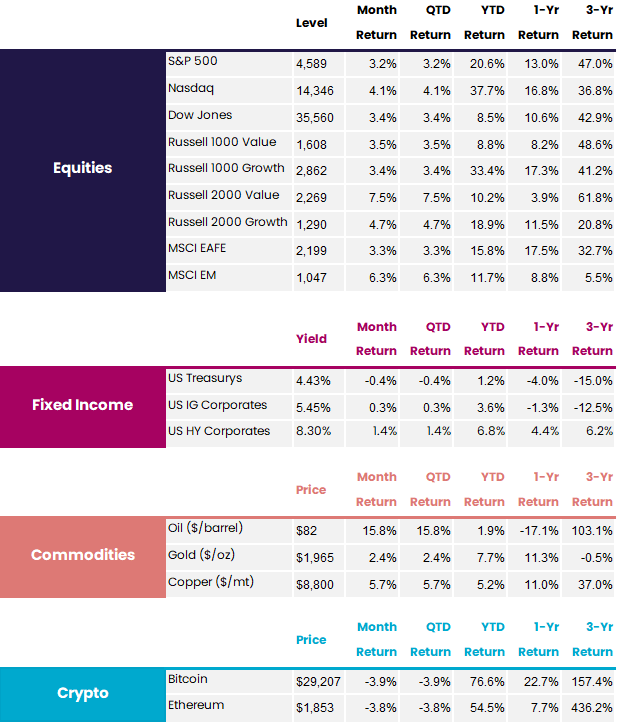

Equities

- Bottom-up 2023 EPS estimates for the S&P 500 fell from $219 to $218 in July, while top-down strategist estimates rose from $214 to $216.

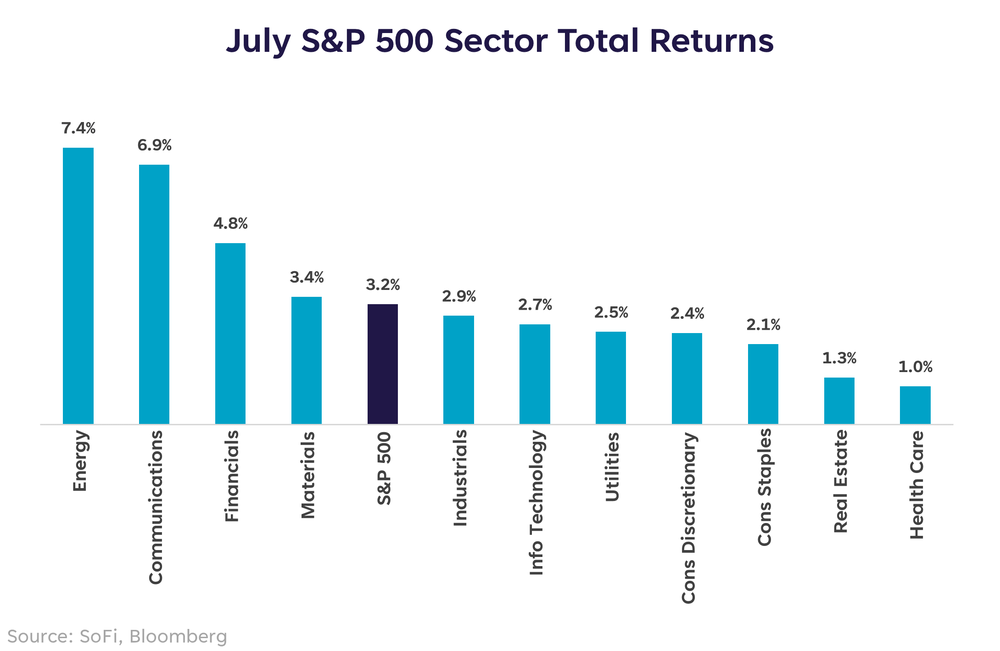

- All S&P 500 sectors had positive returns in July, the second such month in a row.

- The S&P 500 forward 12m P/E surpassed 19.8x at the end of July, the highest level since early April 2022.

- Emerging markets outperformed developed markets for the first time since Nov 2022, buoyed by a rebound in oil & commodities, as well as a weaker US dollar.

Fixed Income

- 2Y & 10Y Treasury yields swung by as much as 46bps & 34bps, respectively, as bond traders reacted to data pointing to strong growth and softer inflation.

- HY bonds outperformed Treasurys & IG bonds for the fourth month in a row, the longest such streak in over two years.

Crypto

- A district court judge ruled that Ripple’s XRP token was not a security when purchased through exchanges, but that it was a security when sold to institutional investors.

The Last Mile is the Hardest

What a difference a year can make. In July 2022, headline CPI had just come in at 9.1% y/y, equity markets were 15-20% off their highs, and the Fed was in the early stages of its most aggressive tightening cycle in over four decades. Now? Annual inflation fell to a smidge below 3%, stocks are up 30-40% off the lows of last year, and markets expect that the Fed just hiked for the last time this cycle.

All clear? Maybe not. It’s often said that the last mile in a marathon is the hardest. A runner’s energy levels are depleted, and time seems to move agonizingly slower as the finish line gets closer. In many ways, investors & the economy find themselves in that position.

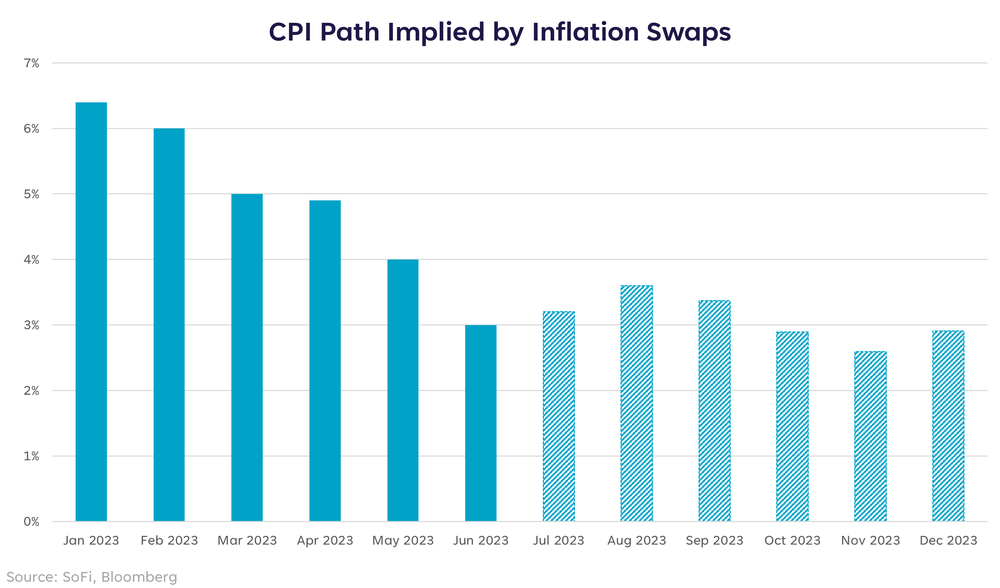

Inflation swap pricing indicates that investors expect y/y inflation to move higher over the next three months, largely due to base effects. Additionally, core inflation, which the Fed believes is a better gauge for judging underlying inflation, has remained elevated due to slower-moving shelter & services components. This is important because the Fed has an inflation target of 2%, not “2% is ideal but 3% is okay”. While inflation has fallen a meaningful amount over the first half of the year, the last leg won’t likely come so easily.

Will the Fed Complete the Marathon?

Chair Powell begins every post-FOMC statement press conference reiterating the Fed’s commitment to restoring price stability. The Fed often notes that while there is risk of doing too much (i.e. hiking too far and causing more economic pain than necessary), the greater risk is not doing enough (i.e. failing to keep inflation down, resulting in inflation expectations rising).

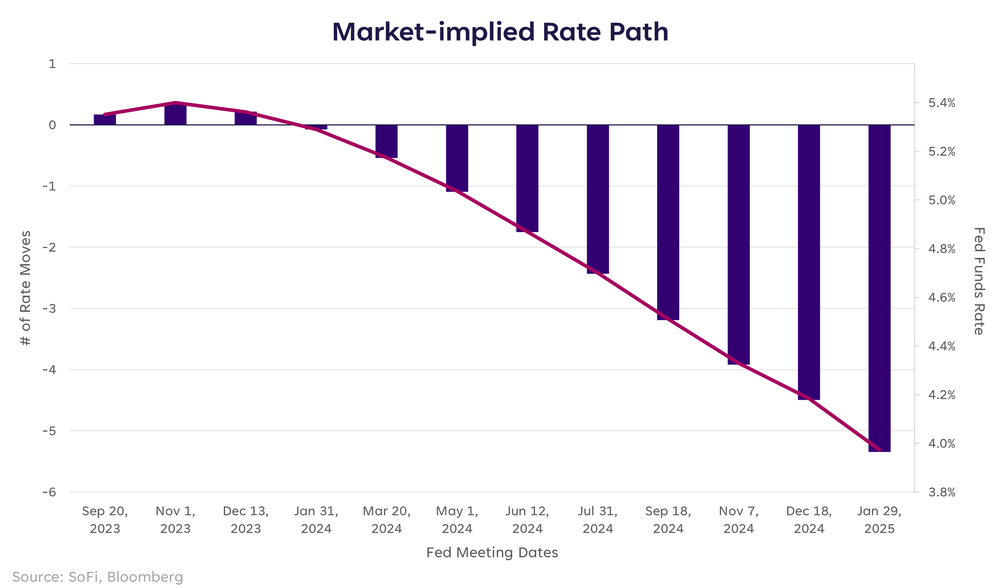

That begs the question: does the Fed plan on running out the final mile? Declines in used car prices & rents point to a summer of core CPI disinflation, with some speculating that the Fed will then have justification to stop hiking. In fact, fed funds futures pricing imply only ~40% odds of an additional rate hike this year, with 4-5 rate cuts priced in for 2024.

However, this has all come with the labor market continuing to add jobs at a robust pace and despite the Fed expecting below-trend growth, economic growth has accelerated as measured by GDP or private investment. For the Fed to begin to cut rates soon, they’d likely need to see signs of economic conditions weakening. Market participants may be expecting the Fed to bow out of this marathon too early. Remember, the last mile is the toughest one.

When should I get a personal loan vs. use a credit card?

You’ve decided that you need to borrow some money, but you don’t know exactly which type of loan will be best for your needs. Two of the most popular types of loans are personal loans and credit cards — but you don’t have to be a personal finance expert to know that they are both very different ways to borrow money.

Below we highlight the pros and cons of a personal loan vs. credit card to help you find out which one is best for your needs.

AaronAmat / iStock

A personal loan is a type of installment loan where the lender provides the borrower with a lump sum of money that they can use for a variety of purposes, such as making home improvements, covering car repairs, or consolidating debt.

Whether using a personal loan to pay down medical debt or pay for a vacation, personal loans can provide you with funding to meet your goals.

Generally, personal loans are paid back each month in fixed payments, or installments, with interest. Repayment is typically spread over a period of 12 months to seven years. You can use a personal loan for emergencies and financing major purchases.

Personal loans can be either secured or unsecured. An unsecured personal loan is an installment loan that’s not secured by any property such as a home or vehicle, whereas a secured personal loan is backed by some type of collateral. (Learn more at Personal Loan Calculator)

designer491/istockphoto

A personal loan works like an installment loan that gives the borrower a lump sum of money — not revolving credit — that can be used for a variety of purposes. The borrower typically repays the loan over a set term, and these required payments may go toward principal, interest, and fees.

Typical Personal Loan Requirements

The requirements for personal loan funding typically require the borrower to provide proof of identity and proof of income. Lenders may review your creditworthiness when determining whether to approve or deny your personal loan application.

Typical Personal Loan Terms

Each lender can determine the terms and conditions of a personal loan, including the annual percentage rate (APR) comprising the interest rate and upfront fees. Borrowers with excellent credit may receive a lender’s best APR, whereas borrowers with bad credit may receive less favorable terms if approved for a loan.

Personal loan amounts may range from $1,000 to $100K. Personal loan repayment terms typically range from 12 months to seven years. You may compare personal loan rates and select an offer from the lender of your choice.

When to Choose a Personal Loan

A personal loan can be ideal for making large purchases. This simple type of loan allows you to break down a big purchase into smaller monthly payments that you spread out over time. A personal loan can also have lower interest rates than some other types of loans, including credit cards.

Generally, interest rates are lower for secured vs. unsecured personal loans, though with the former you run the risk of losing your collateral.

One of the top uses for a personal loan can be to consolidate your debts, especially those with high interest rates. And it’s also a great type of loan for people who would prefer to be committed to making the same payments each month. There are even personal loans available after bankruptcy.

wutwhanfoto/istockphoto

A credit card is a financial instrument that represents a revolving loan. When you use a credit card to pay for something, the credit card issuer (e.g., your bank) covers the cost of the purchase with the understanding that the cardholder will pay back the amount borrowed, plus any interest that applies.

When credit card users pay their entire statement balance in full by the statement due date, nearly all credit card issuers will waive interest charges. Credit cards typically represent an unsecured loan, so there’s no property that can be repossessed if credit card payments aren’t made. And while using a credit card irresponsibly can certainly damage your credit card, they can also help build it — in fact, there are a number of top credit building cards out there.

Credit card users also enjoy robust security protections against fraud and billing mistakes. They can also offer rewards in the form of cash back, points, or miles. And finally, credit cards can provide travel insurance policies, purchase protection benefits, and other perks.

bernie_photo/istockphoto

A credit card works like revolving or open-end credit — cardholders have a line of credit and the ability to make transactions up to the credit limit.

One of the keys to understanding credit cards is recognizing how your line of credit limits the spending power on your card. A portion of your available credit is used when you make transactions on the card. Unless you have a $0 balance, cardholders are expected to make at least minimum monthly payments each billing cycle.

Paying your credit card bills may replenish your available credit.

Typical Credit Card Requirements

Consumers typically need proof of identity and proof of income to become a credit card account holder. Credit card issuers may review your creditworthiness when determining whether to approve or deny your credit card application.

Some credit cards may offer 0% intro APR on purchases for several billing cycles or cash back rewards. You may compare credit cards and apply for the card of your choice.

damircudic/istockphoto

Depending on your circumstances, a personal loan may not be the right choice. A credit card can be a good option when you need a secure and convenient method of payment and are confident you can pay off your balance in the short term to avoid paying interest.

As a revolving loan, a credit card has no set terms, other than the minimum payment amount you must make each month. With a credit card, you can borrow as much or as little as you need up to your approved credit limit, and you only pay interest on the loan based on your account’s average daily balance. Some credit cards can also come with 0% APR introductory financing offers for new accounts.

That means you won’t begin incurring interest on your charges until the day they are made, and you can make payments against your balance at any time, and in any amount. All you have to do is make sure that you make at least the minimum payment each month on or before the statement due date.

izzetugutmen/istockphoto

When comparing a personal loan vs. credit card, it’s important to consider the benefits and drawbacks of each.

When is a personal loan better than a credit card? This chart highlights how either a personal loan or credit card can help you meet your goals and the pros and cons of an installment loan vs. credit card.

Sofi

This table highlights some of the pros and cons of credit cards. (Learn more atHow Many Credit Cards Should I have?)

Sofi

Once you understand the advantages and drawbacks of each, it’s up to you to decide whether a personal loan or credit card will best meet your needs.

A personal loan can be a better choice when you are making a large purchase and want fixed repayment terms. A credit card, on the other hand, can be a better option when you occasionally need to finance smaller purchases, or are just looking for a method of payment that can sometimes be used as a loan.

SARINYAPINNGAM/istockphoto

Even if you understand the difference between a loan vs. credit card, there are other funding options that may be worth considering. Below we highlight some alternative funding options you may consider:

- HELOC: A home equity line of credit, or HELOC, uses the equity in your home to secure a revolving personal loan, allowing you to draw funds as you need them. Just keep in mind you are putting your home up as collateral, which means you could risk losing it if you fail to repay the loan.

- 401(k) loan: You can also take loans from your 401(k) retirement plan, which is essentially making a loan to yourself from your own savings. However, there can be substantial penalties if you fail to pay it back on time or leave your employer with an unpaid loan. You’ll also be missing out on potential growth on those funds.

- Loans from friends and family: Friends and family can offer you personal loans. And while they may offer excellent terms without having to make a formal application, family loans can risk your relationships if not paid back.

fizkes/istockphoto

As you can see, there are clear differences between credit cards and personal loans, as well as pros and cons to consider when weighing whether a personal loan vs. credit card is better for your financial situation. Make sure you understand the ins and outs of whichever financial product you choose and that you can afford to pay off any debt you incur to avoid negative consequences to your credit score.

This article originally appeared on SoFi.com and was syndicated by MediaFeed.org.

Please understand that this information provided is general in nature and shouldn’t be construed as a recommendation or solicitation of any products offered by SoFi’s affiliates and subsidiaries. In addition, this information is by no means meant to provide investment or financial advice, nor is it intended to serve as the basis for any investment decision or recommendation to buy or sell any asset. Keep in mind that investing involves risk, and past performance of an asset never guarantees future results or returns. It’s important for investors to consider their specific financial needs, goals, and risk profile before making an investment decision.

The information and analysis provided through hyperlinks to third party websites, while believed to be accurate, cannot be guaranteed by SoFi. These links are provided for informational purposes and should not be viewed as an endorsement. No brands or products mentioned are affiliated with SoFi, nor do they endorse or sponsor this content.

Communication of SoFi Wealth LLC an SEC Registered Investment Advisor

SoFi isn’t recommending and is not affiliated with the brands or companies displayed. Brands displayed neither endorse or sponsor this article. Third party trademarks and service marks referenced are property of their respective owners.

Communication of SoFi Wealth LLC an SEC Registered Investment Adviser. Information about SoFi Wealth’s advisory operations, services, and fees is set forth in SoFi Wealth’s current Form ADV Part 2 (Brochure), a copy of which is available upon request and at here. Liz Young is a Registered Representative of SoFi Securities and Investment Advisor Representative of SoFi Wealth. Her ADV 2B is available at here.

Doucefleur/istockphoto

William_Potter/istockphoto

Featured Image Credit: FreshSplash/istockphoto.