Life insurance protects your loved ones against financial expenses when you pass away. It can also help you pay for the estate taxes of a deceased member of your family. Some may not be aware of the benefits and strategies that can be implemented to maximize such advantages. MoneyGeek breaks down how life insurance can be used in estate planning and provides tips.

Image Credit: DepositPhotos.com.

What the Numbers Say

The following data show an overview of life insurance and estate planning in the United States:

- 54% of people living in the United States have life insurance coverage. The percentage of life insurance owners in the country declined 14% over a 10-year period ending in 2020.

- 55% of Americans ages 55 and up have a will, but only 18% have all recommended legacy essentials, which include a will, healthcare directive/proxy and a durable power.

- More than 55% say their insurance is for income replacement and transferring of wealth across generations. 80% of insured say their goal is to pay for their burial costs and final expenses.

- More than half of Americans think that the estimated cost for a $250,000 term life policy for a 30-year-old healthy individual is $500 or more per year.

- 70% say they need life coverage: Around 42 million non-owners showed purchase intent.

Image Credit: SolisImages / istockphoto.

5 Ways Life Insurance Can Help With Estate Planning

Survivors are often tasked with sorting through the assets and liabilities of a deceased person while they are grieving. Life insurance can alleviate the difficulties of estate planning by providing financial support to family members and business asset coverage.

Image Credit: vgajic.

1. Estate Taxes Payment

One of the best ways to pay for estate taxes is by having a life insurance policy. Federal estate tax applies to the gross estate of the deceased and must be paid within nine months after the death of an owner. Some states also impose estate taxes. Proceeds of life insurance are often tax-free.

Image Credit: DepositPhotos.com.

2. Business Asset Coverage

Choosing universal life insurance gives you access to an investment savings component. Depending on the terms of your policy, you can also borrow the cash value as a financial cushion in case your business encounters problems.

Additionally, life insurance can serve as collateral for a business loan or fund a buy-sell agreement. Buy-sell agreements set prices and terms that surviving partners must follow to purchase the shares of the deceased or leaving partner. If you die, surviving owners will receive death benefits, and your family will get payment for your interest in a company.

Image Credit: DepositPhotos.com.

3. Faster Payouts

Expenses related to the death of a person include funeral and burial costs, possible debts and taxes. Liquidating assets can take time. The Death Benefit of a life insurance policy, on the other hand, can be claimed immediately, which makes it useful for paying out such expenses and reducing the financial burden of a death on your family.

Image Credit: DepositPhotos.com.

4. Estate Equalization

Having more than one heir to an estate can lead to complications. When it is difficult to split up assets, conflicts may arise. Additionally, there are cases when breaking up an estate can reduce its ability to generate revenue. In such instances, life insurance can be used to equalize estate inheritance. For instance, one heir may receive property while another may receive the death benefit proceeds of the insurance policy.

Image Credit: GaudiLab / istockphoto.

5. Future Preparation

As the owner of a policy, you have the option to choose how the proceeds of your insurance will be used. For instance, you can continue supporting a loved one even after your death, which is especially helpful for aging adults, minors and children with disabilities. Others may use it to continue alimony or child support payments, fund a trust for another purpose. With a trust, you can hold assets on behalf of your beneficiary under the supervision of a trustee.

Image Credit: Halfpoint / istockphoto.

Choosing the Right Life Insurance

Before buying life insurance, it is important to think about your needs and circumstances and know the answers to some basic questions. For example, how much coverage will you need? What kinds of life insurance are out there?

Which providers offer the best policies? The following steps can help you make an informed decision.

Image Credit: Depositphotos.

1. Calculate the coverage amount you need

Consider your annual income, assets, expenses and debts. An approximate calculation will help you find out how much life insurance you need. For some, having coverage that is ten times your salary may be a good starting point.

However, this technique may not be useful for everyone. Often, it is helpful to include all outstanding debts when calculating necessary coverage.

Image Credit: DepositPhotos.com.

2. Decide on what type of life insurance to buy

There are different types of life insurance. With term life insurance, your loved ones will get a death benefit payout after you die. However, the “term” only covers a certain number of years. If you happen to outlive the term, you or your loved ones will not receive payment. Permanent life insurance, which includes universal life insurance and whole life insurance lasts a lifetime.

Image Credit: DepositPhotos.com.

3. Compare insurance providers and prices

Proceed payouts usually happen during stressful times, and having a reliable provider can help your loved ones have a hassle-free experience. Shopping around can help you find the best provider and most accurate policy. Compare personalized quotes from at least three insurance companies, and check the financial stability and customer service ratings of insurers if possible.

Image Credit: DepositPhotos.com.

4. Learn the application process

Once you find the right insurer, you can proceed to the application process. Most companies allow clients to apply online, through mail or via insurance agents. Ask in advance if there are documents you need to prepare. Most likely, you will need to provide basic personal information. Depending on the policy you choose, you may also have to see a medical professional for a health assessment.

Image Credit: DepositPhotos.com.

5. Choose your beneficiaries

The beneficiary of your policy can be a person or an organization. Your insurance provider will tell you what information is needed, but you will most likely have to provide the tax identification number or Social Security of your chosen beneficiaries. If you plan on naming a minor or child with a disability to your policy, consider leaving the cash value to a trust.

Image Credit: DepositPhotos.com.

Using Life Insurance in Estate Planning

Generally, life insurance plays three main purposes in estate planning. First, it provides death benefits to chosen beneficiaries. Second, it provides liquidity that can be helpful with an estate. Lastly, it allows loved ones to obtain financial support. That said, there are various strategies to maximize the benefits that life insurance offers when it comes to estate planning.

Image Credit: tommaso79/ iStock.

Dealing with Estate Taxes

The value of an estate can rise or fall depending on federal and state taxes. Estate taxes are due nine months after the death of the owner. Savings, investments, loans and liquidation can all help settle an outstanding balance.

However, such tools may not be enough. In reality, life insurance can be one of the most advantageous ways to alleviate the financial burden of paying an estate tax. Proceeds will be given to your beneficiaries, and insurance payouts are often tax-free. The following resources can help you learn more:

- Internal Revenue Service: The IRS can answer some of the most common questions about estate tax issues, including what is included in an estate, if you are required to file, when you can expect an estate tax closing letter and what happens if you sell property that you’ve inherited.

- Tax Foundation: The Tax Foundation is an independent tax policy nonprofit which provides research and analysis. It works on state and federal tax policy to educate Congress, politicians and others about the short and long-term impact of reform.

- NOLO Legal Encyclopedia: The encyclopedia provides a primer on the states which have appealed estate taxes, the states that impose estate taxes and many other relevant issues.

- Congressional Budget Office: The Budget Office offers a helpful guide to understanding estate and gift taxes, including the types of people who pay them and the types of assets that make up taxable estates.

- American College of Trust and Estate Counsel: ACTEC regularly updates a state death tax chart which you can consult to find out more information about the laws that apply in your state. The chart shows whether a tax is tied to federal state death tax credit or if an estate tax has been repealed.

Expert Tip: Check the estate tax exclusion law in your state. While the federal estate tax exclusion is $11.7 million for individuals and $23.4 million for married couples, your state may have lower exclusion amounts. According to a proposed federal tax law, starting on January 1, 2026, the exemption will return to $5.49 million adjusted for inflation. With inflation, this amount may be around $6 million for individuals or $12 million for married couples.

Image Credit: DepositPhotos.com.

Estate Equalization and Asset Distribution

Deciding on the inheritance to leave behind to each of your heirs can help protect against fallout after someone passes away. Assets like businesses and residences may have multiple owners, which is where life insurance comes in.

That’s because death benefit proceeds can be used to balance the value of assets. For instance, you can leave behind your business to one child and give death benefits to another. Life insurance can also be used to equalize distribution to heirs using your business. For example, you can have a buy-sell agreement wherein the company buys a life insurance policy that will pay a benefit to participating heirs upon your death.

Expert tip: Before finalizing the terms of your life insurance policy, it may help to have a discussion with your heirs. Determine which children are willing to participate in your business and which are not. Doing so can help you have non-participating children receive a cash distribution from your policy.

Image Credit: DepositPhotos.com.

Income Replacement and Access to Cash

Being the breadwinner of a family comes with many responsibilities. A family may depend on you for expenses, and your death may lead to the loss of significant income. With life insurance, you can continue supporting your loved ones through the proceeds of your policy. Depending on the type of policy you choose, you can use insurance as income replacement or coverage for unexpected expenses like medical costs or debt payment. You can also turn your insurance into retirement income by surrendering the cash value or executing an exchange into an annuity.

Expert tip: A permanent life insurance policy can accumulate cash value over time, and you can withdraw funds to cover emergency expenses. If you take out a loan against your policy, it is tax-free if it doesn’t exceed the premiums paid in a policy.

Image Credit: bunditinay / istockphoto.

Should You Have an Irrevocable Life Insurance Trust?

If you aim to use life insurance in estate planning, an irrevocable life insurance trust (ILIT) can be created to control either a term or permanent insurance policy while a policy owner is still alive. With an ILIT, you can transfer your policy to the trust or use the trust to purchase life insurance, which means the trust owns your insurance policy. The trust document will determine who will administer assets, designate beneficiaries and establish terms on how beneficiaries receive benefits.

Image Credit: DavidsAdventures/istockphoto.

How an Irrevocable Life Insurance Trust Works

An ILIT removes a life insurance policy from your estate, helping you minimize or even eliminate your estate tax liabilities on assets that do not qualify for a charitable or marital deduction. It can also help with the management and distribution of proceeds upon the death of the insured by immediately providing liquidity for the decedent’s estate and estate beneficiaries.

Image Credit: DepositPhotos.com.

Parties involved with an ILIT

There are multiple parties involved with an ILIT:

- Insured/Grantor: The person covered by the policy. The grantor is the one transferring assets to the trust. They determine who the beneficiaries will be. Upon the execution of the agreement, the grantor cannot change or terminate an ILIT because it is irrevocable.

- Trustee: The ILIT’s trustee is the policy’s owner and beneficiary and is the one who manages or administers the trust. The trustee controls the trust until the conditions and time the grantor has set has been satisfied. The policy’s proceeds are determined by the terms of the ILIT.

- Beneficiaries: Beneficiaries are individuals or entities who will receive the policy’s benefits after the death of the insured. A parent or legal guardian can oversee actions if the beneficiary is a minor. But keep in mind there is a limited time for named beneficiaries to exercise their withdrawal rights. After the specified period, a trustee has more funds available to pay life insurance premiums.

Image Credit: istockphoto/RossHelen.

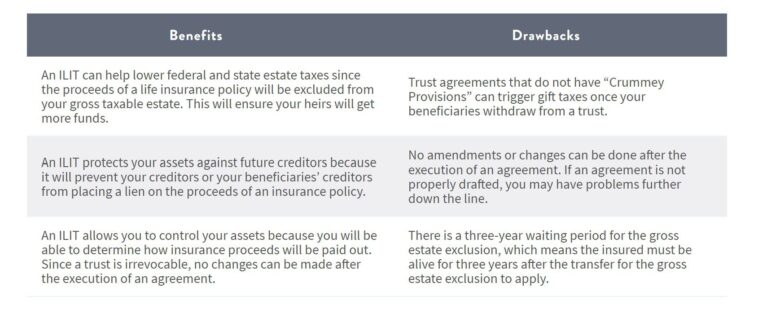

Benefits and Drawbacks of Irrevocable Life Insurance Trust

An Irrevocable Life Insurance Trust comes with a variety of advantages and drawbacks. For example, an ILIT is a great option if you want to set aside your assets for specific purposes, but you may be responsible for paying gift taxes if a beneficiary withdraws from a trust. Make sure to weigh all pros and cons before deciding to create one.

Image Credit: Moneygeek.

The Bottom Line About ILIT

ILITs can help with wealth management and estate planning. However, they may not be the best option for everyone. Keep in mind that the trust agreement under an ILIT is irrevocable. That means you can no longer change the terms once they are in effect. If you think the terms may cause problems in the future, consider alternative options, such as choosing an entity to be the owner of the life insurance policy, giving a policy as a gift to ensure that it is out of your estate or making your child the insurance policy owner.

Image Credit: fizkes/istockphoto.

Common Challenges and How to Avoid Them

Estate planning requires proper preparation. The same approach may not be applicable for everyone, so take a look at the particulars of your situation, conduct your own research, consult with professionals and learn about all possible options and alternatives.

It’s vital to learn how to recognize estate planning challenges. To prevent incurring losses and ensure that you are getting the best available option for you and your heirs, pay attention to family members with disabilities, blended families, family-owned businesses and spouses.

Image Credit: DepositPhotos.com.

1. Family Members with a Disability

Estate planning can help you take care of your surviving loved ones after you pass away. For some, that means choosing which assets to give to whom.

However, there may be cases when a certain family member requires more care. Finding the best legal tools can be difficult. If you have children with disabilities, consider the following resources:

- Academy of Special Needs Planners

- Federation for Children with Special Needs

- Special Needs Alliance

- The Arc Center for Future Planning

Image Credit: DepositPhotos.com.

2. Blended Families

A blended family situation can complicate estate planning. For instance, one or both spouses may have children from prior relationships which can lead to conflicts of interest. It may also be difficult to decide on how to treat children when it comes to inheritance.

Image Credit: laflor.

3. Family Businesses

Estate planning that involves a family-owned business can be stressful and challenging. Some parents find it difficult to ensure that all children get fair treatment. If some heirs are more involved in the business, they may not agree to share ownership or profits with their non-participating siblings.

Image Credit: DepositPhotos.com.

4. Spouses

In many cases, surviving spouses inherit the deceased’s estate. A problem may arise when a spouse decides to make changes to the estate after the death of the owner. This situation can be more problematic in blended families if a surviving spouse chooses to favor their children over the deceased’s children from earlier relationships.

Image Credit: monkeybusinessimages.

How to Avoid Common Mistakes

The decisions you make about estate planning will impact the lives of your loved ones after you pass away. It’s important to consider your assets and liabilities, speak to your family and consider life insurance. A do-it-yourself approach can work just fine, but always look at the possibility of hiring law professionals and getting advice from financial advisors or insurance agents.

Taking time to investigate the entirety of the process can help you avoid making costly mistakes.

Image Credit: Inside Creative House / istockphoto.

1. Consider your assets and liabilities

It is important to figure out which assets and liabilities may affect your heirs in the future. Determine the best way to distribute assets and find out if there are debts that may affect your heirs after your death.

Image Credit: fizkes/istockphoto.

2. Talk to your family

When it comes to estate planning, one of the most pressing issues is the distribution of assets. To avoid conflict among your heirs, discuss your plans with them. This way, they will know what wishes they have to fulfill upon your death. It can also help clarify any issues about their inheritance.

Image Credit: istockphoto.

3. Consider life insurance

Life insurance can provide many benefits to your family, such as settling estate taxes, ensuring that all your heirs get an equal inheritance and helping give financial support after your death so your family can take care of expenses, such as funeral and burial costs.

Image Credit: DepositPhotos.com.

4. Discuss with professionals

When it comes to estate planning, it is important for you to know all your options and find the best ones based on the particularities of your situation. A lawyer or financial advisor can help you make great decisions, give you proper knowledge and even help you draft a trust agreement that can protect you against any possible complications.

This article originally appeared on MoneyGeek.com and was syndicated by MediaFeed.org.

Image Credit: Ridofranz/istockphoto.

More from MediaFeed

Why a frugal lifestyle is powerful, painless & fun

Image Credit: Georgijevic.