A new year is supposed to be a time of fresh starts, enthusiasm for what’s to come, and resolutions to do something different. But starting something new suggests that we’ve recently finished something old. Despite what the calendar says, we are certainly not done with what we started in 2022. Inflation continues to prove itself a worthy opponent, markets remain limited by resistance levels, and investors are still searching for things that either confirm or deny a looming recession. In 2023, this ends one way or another.

Rest in Peace, 2022

Unless you’re a glutton for punishment, I think I speak for most of us in saying I’m looking forward to closing the book on this year.

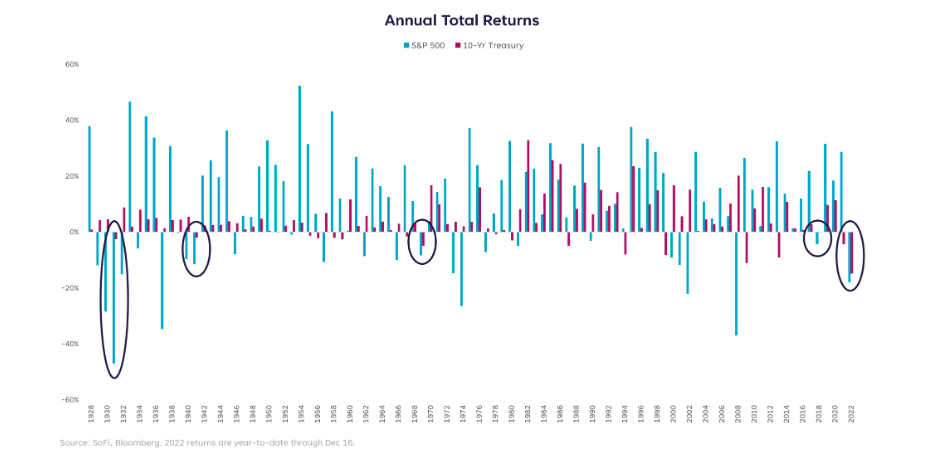

I could list all of the challenges we faced, but in the interest of writing space and my own mood, I’ll leave it at this: equity markets entered bear territory, the 10Y Treasury saw its worst year ever, and the Fed squeezed liquidity with a vise. This resulted in only the fifth year since 1928 when both stocks and bonds were negative.

Like most things, there are two sides to every story. We can look at the negative — nothing worked, diversification failed us, our net worth fell, and markets are broken. Or we can look at the positive — the tough part is behind us, we’ve shaken out the excess froth, we’re making good yields on cash, and bonds are more attractively priced than they’ve been in decades. I’ll take an even more simplistic view and say the chances of us having another year of double-digit declines in both stocks and bonds are very, very slim.

This year was one of calling peaks: peak inflation, peak Treasury yields, peak Fed hawkishness, peak oil prices, and peak uncertainty. With many of those peaks likely in the rearview, it’s safe to say we did some good work in 2022 on both the market and economic fronts. Unfortunately, we’re not done yet. The question of whether we’re in for joy or pain in 2023 can be answered by finding out how the ending occurs, how quickly we draw to a close, and whether we really did pass peak uncertainty.

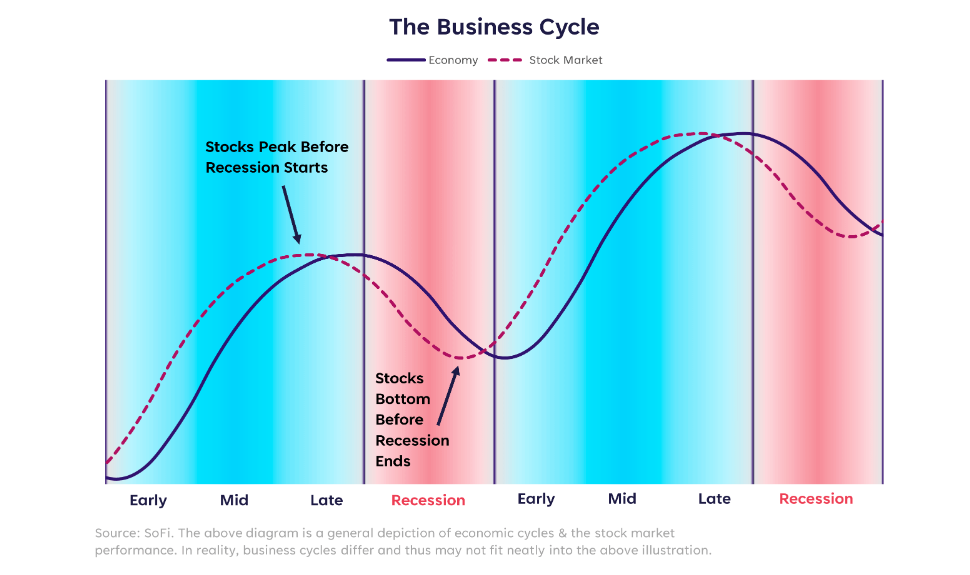

Respect the Cycle

If there is one point I continue to reiterate it’s this one: we must respect the cycle. The cycle I’m talking about is the business cycle, with the typical phases shown below:

The length of each phase and the time between them always varies — but rest assured, the cycle repeats. Determining where we are in this continuum is the puzzle. And even if we know the answer with some degree of certainty, the unpredictable element is how long we’ll stay at that point before moving into the next phase.

There are some clear characteristics of each phase, which I won’t make an exhaustive list of here, but much of the current data indicates we are in the “late cycle” phase. This occurs after peak expansion (remember, 2022 has been a year of peaks) and is typically characterized by high or rising inflation, monetary tightening to control said inflation, a flat or inverted yield curve, and the beginning of a decline in cyclical indicators such as housing or the labor market. Every single one of these boxes has been checked.

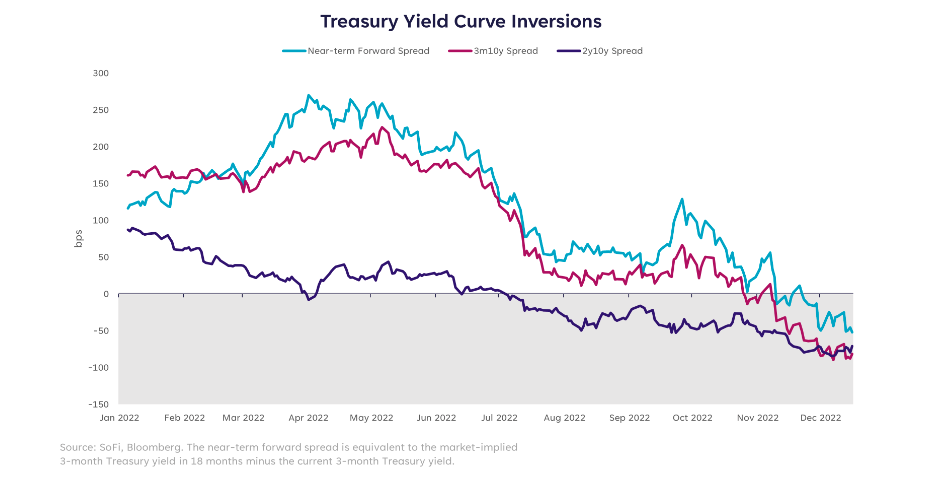

The bond market in particular is shouting “late cycle” from the rooftops, with curve inversions galore.

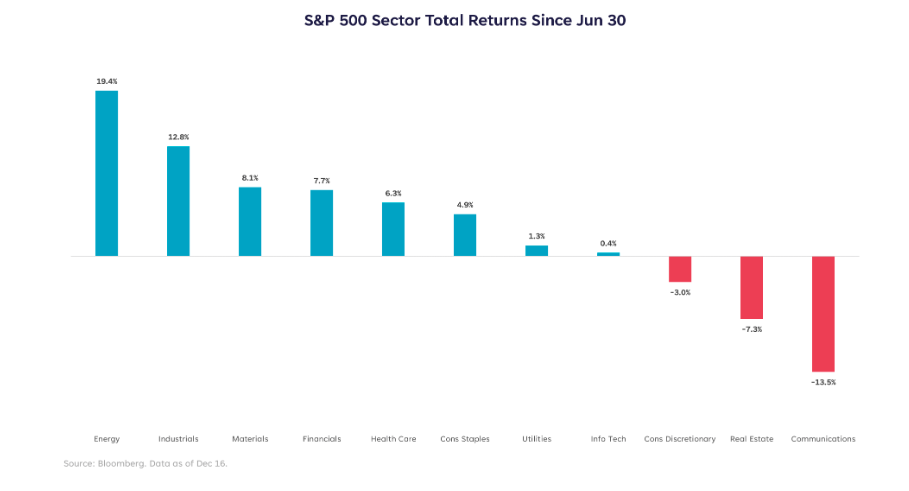

If we look to the stock market, we’d expect “late cycle” to result in a defensive posture, with “safe” sectors outperforming riskier ones. Using June as the point when inflation (CPI) peaked, the sector performance since then sets an interesting tone. Healthcare is the only classically defensive sector that sits in the top half, while most of the others are cyclical. Meaning, the stock market doesn’t definitively agree with a “late cycle” narrative, and mixed signals still abound.

Those mixed signals have driven multiple bear market rallies that failed to materialize into new bull markets. They’ve also brought the volatility index (VIX) briefly below 20, but not allowed it to stay there longer than a few days before popping back up. And they’ve kept us in this purgatory between recession/no recession for what feels like an agonizingly long time.

Calling All Spades

People don’t like to hear words of caution, and they certainly don’t like to hear a message that suggests downside in markets or pain to come in the economy. But if I edited my honest opinions just to limit criticism from optimists, I wouldn’t be doing my job.

So let me call a spade a spade: I think the bond market has this right, and the economic indicators reinforce that message. We’re late cycle. The next spade in my hand says: I don’t see how we get back to early cycle without a recession. I just don’t think we’ve seen enough evidence of it to convince market valuations yet.

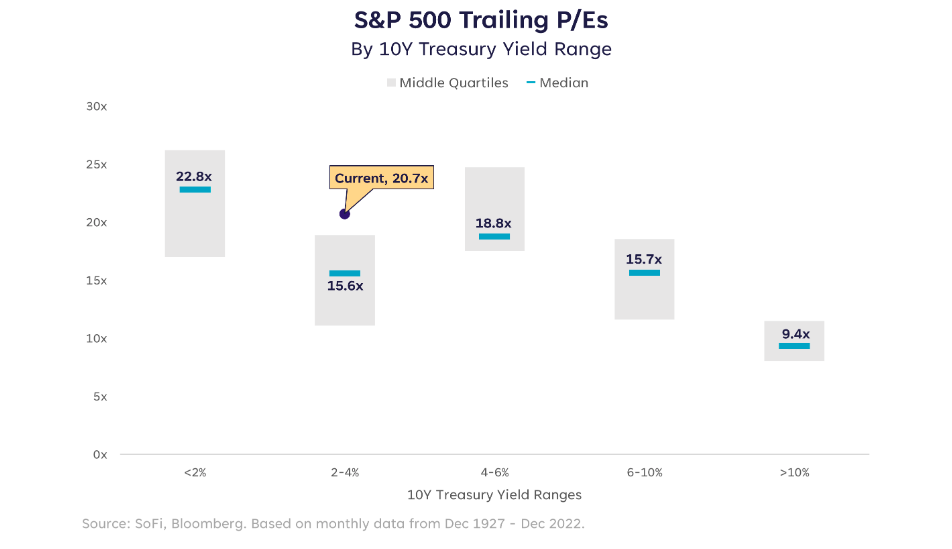

Here’s an illustration of where the trailing price-to-earnings (P/E) ratio is in relation to corresponding 10Y Treasury yield ranges. Relative to history, the current P/E of 20.7x is in the 80th percentile of observations — well above even the top end of the median range.

Forward P/Es tell a similar story. The current forward P/E is 17.0x, which is just slightly below the 10-year average of 17.2x. Moreover, five of those 10 years were spent at a zero-bound fed funds rate, and the average 10Y Treasury yield was 2.1%. The fed funds rate is at 4.5% today, and the 10Y Treasury yield is ~3.5%. Not the same environment by any stretch.

As the name of the ratio says, P/Es depend on the level of earnings. When prices (P) are rising and earnings (E) are steady or falling, stocks are enjoying what’s called “multiple expansion” — a.k.a. rising for reasons unrelated to company performance. One could argue that markets had been riding a multiple expansion train ever since rates went to zero, and promptly exited that train when rates began to rise. The train isn’t even selling tickets anymore.

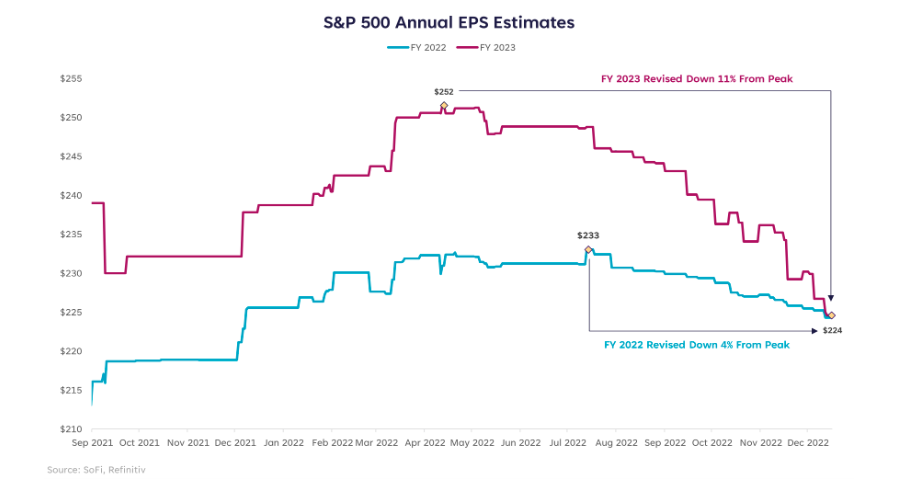

Earnings estimates for 2023 have fallen steadily over the last few months, now sitting at $224/share, which represents no growth over 2022 earnings, but I still think expectations are too high. Those estimates are down from a peak of $252/share in April, and I expect downward revisions to keep rolling in for at least another quarter.

With that backdrop, in order to be bullish on the stock market you have to believe that multiple expansion will carry us forward. I don’t believe that. At least not before we give back some of this P/E multiple and get more in-line with what bond markets are telling us.

Not Sold Separately

One thing I’ve learned as a strategist is that my thesis has to be internally consistent. That said, in order to be consistent with my previously stated take — that I don’t see how we can reset the business cycle without a recession — I also don’t see how we can confirm a recession and expect equity valuations to stay this high.

Which means we can’t have it both ways. We can’t expect inflation to come down by way of reducing demand without seeing collateral damage to consumer spending. We can’t expect demand and pricing power to come down without seeing collateral damage to corporate profits. Add to those forces to downward earnings revisions and there’s likely to be collateral damage to the U.S. economy.

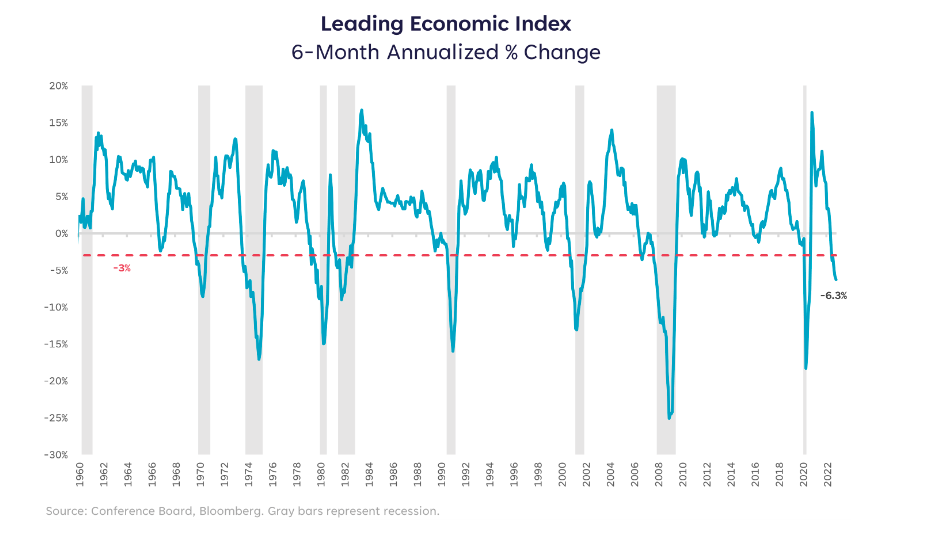

A commonly used indicator of economic health is the index of Leading Economic indicators (LEIs). If we track the 6-month annualized percent change in the index, we can see if it’s moving in a definitive direction over time. The chart below shows what’s happened recently, with the latest 6-month change at -6.3% — meaning LEIs have been steadily falling over that period. Not-so-fun fact: this reading has never fallen below -3% without a recession to follow.

The most recent market bottom in October saw a forward P/E of 15.3x. Valuations may not need to get quite that low again — especially since the earnings (E) have come down, which mathematically allows for a higher P/E on the same price (P). But unfortunately, I don’t think we’re quite done with market drawdowns for this cycle. On the bright side, if we are nearing a recession, the market would theoretically drop before the economy hits a trough. That’s exactly why I expect one more plunge before the imbalances are corrected.

Finding “The One”

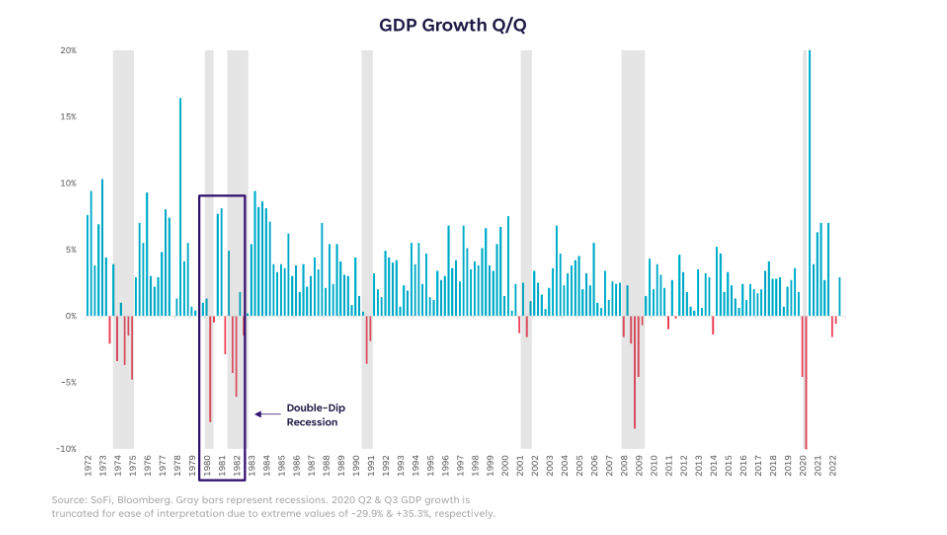

One of the hottest debates of 2022 was how to define “recession.” The generally accepted definition before now was two consecutive quarters of negative GDP growth. We met those conditions in the U.S. during the first half of the year with Q/Q GDP at -1.6% for Q1 ‘22 and -0.6% for Q2. But did it count as a real recession? After all, the drag that brought us to negative territory was largely due to trade imbalances (imported more than we exported) and a reduction in inventory builds. Those items matter, to be sure, but the largest proportion of our economy is consumption, which remained positive for both periods.

Even if we say it counted as a technical recession, it wasn’t broad enough to reset the business cycle (see “Respect the Cycle” above). It was more likely the whiff of recession before the real recession.

As such, if we do enter a recession in 2023, it would technically look like a double-dip recession, much like what occurred in the late 1970s/early 1980s. If at first you don’t succeed, try, try again?

That period and today are eerily similar with inflation as the primary enemy. The difference is that this Fed is determined to not make the same mistakes as that Fed, which one could characterize as a “stop/start” approach to rate hikes. Jerome Powell has committed to steadily increasing rates, if not purposely overtightening, in order to defeat inflation.

The conundrum we face is that most recessions are preceded by a rate hiking cycle — and the idea that we will get through an aggressive hiking cycle and somehow manufacture a soft landing is a bit fantastical, in my view.

But how do we know when the real recession is here, and if it’s “the one” that will finally reset the cycle? That’s where the labor market comes in.

Through almost all of 2022, many have claimed that strength in the labor market is the golden ticket that will help us avert recession in 2023. That could end up being the case, but I’m skeptical that jobs data will stay this strong. The labor market is notoriously one of the last indicators to break in economic downturns, and this cycle is likely no exception. Companies are less willing to lay off workers than ever before because of how difficult it’s been to find new ones. But as wage growth continues to eat into profits and slower demand eats into revenue, pressures mount.

Continuing jobless claims have started to rise, but job openings remain elevated and the unemployment rate is historically low. I expect that story to shift over the course of the next few months. Jobless claims are likely to increase, job openings are likely to fall as companies lay out their 2023 plans, and a slow uptick in the unemployment rate could materialize.

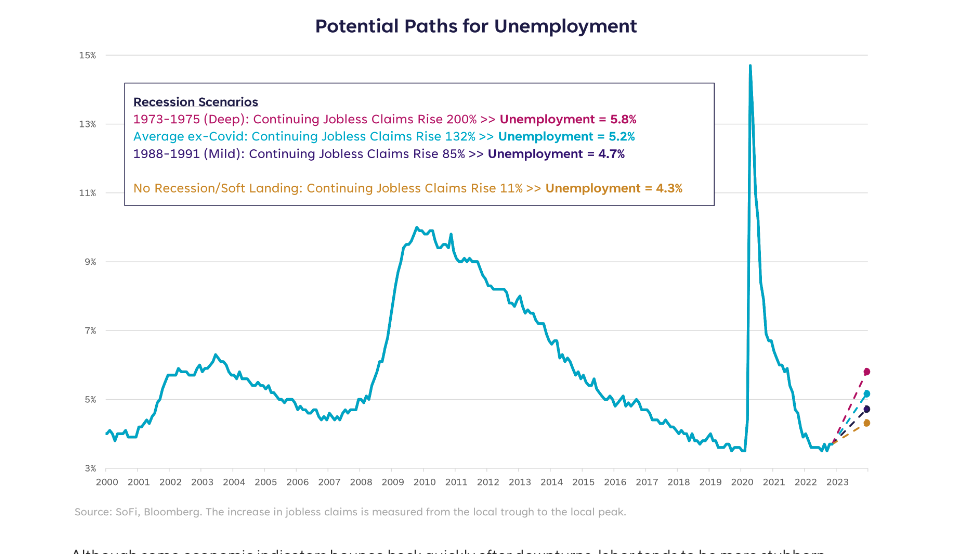

In an attempt to model how this may play out in different scenarios, we’ve made some assumptions on unemployment based on past recessions. The chart below shows what could happen if history repeats itself and the economy loses a similar amount of jobs as prior scenarios.

Without declaring whether I believe a recession will be deep, average, or mild, the good news is the worst we are modeling is an unemployment rate that remains below 6%. The bad news is the length of time it typically takes for this to play out (from trough to peak unemployment) is anywhere from 26-53 months. Woof.

Although some economic indicators bounce back quickly after downturns, labor tends to be more stubborn. Nevertheless, in order to determine if and when “the one” has arrived, I believe labor data will be our irrefutable evidence.

Fama, French, and Finding Opportunities

What does it mean for markets, what happens to my investments, where is the opportunity, and where are the monsters hiding?

I wrote earlier that the likelihood of having another year with double-digit declines in stocks and bonds is highly unlikely. So we’ve got that going for us. I also firmly believe that this indecisive state of “recession/no recession” is worse for markets than simply having a recession and answering the question. Not to mention, the average S&P 500 return 12 months out from a recessionary market bottom is 49%. Not too shabby.

One way to look at opportunities in 2023 is via factor investing. There is an old asset pricing model called the Fama French model. If you’ve never heard of it, that’s because for the better part of the last two decades it hasn’t really worked. But I believe it’s about to take center stage.

The basic premise of the model suggests that value stocks should outperform growth stocks, and small-cap stocks should outperform large-cap stocks. These two factors — the value factor and the size factor — have not produced attractive results through an era of extremely low interest rates and perpetual multiple expansion of large-cap tech stocks. But I think the tides of opportunity will shift back in favor of Fama French in 2023.

Part of that is based on the Fed’s commitment to keeping rates at restrictive levels until we make substantial progress on inflation, which could be a while. That means rates are likely to stay elevated for a large chunk of 2023 and the era of rate-driven multiple expansion is over.

Another part is based on my expectation for a recession in 2023. If and when the market comes to grips with that reality, particularly given that this would be an inflation and rate hike driven recession, large-cap growth stocks may not be the darlings of the next bull market. As such, if markets correct again, I would find value in classic early-cycle sectors and asset classes such as: Financials, Industrials, Semiconductors, Consumer Discretionary, small-caps (particularly small-cap value).

In the bond market, I expect a widening of credit spreads (i.e., lowering of prices) in both investment grade and high yield bonds in concert with an equity market decline. High yield bonds may then become quite attractive from a price and yield standpoint, but be careful not to load up too much on risk if there’s a great deal of stocks already in the portfolio.

Lastly, the much discussed Treasury market. After a year where Treasuries did nothing to offset equity risk, they once again can serve as risk management tools. The opportunity in Treasuries is now, while yields are still elevated and before a recession is confirmed.

TL;DR

For those of you who don’t speak in acronyms, TL;DR = too long didn’t read. I hope you read it, but if you didn’t, here’s the gist: I think the bond market is right, a recession is coming, and stocks will soon trade closer to reasonable valuations. I also believe that we need to reset the business cycle and start anew. If that begins to materialize, I’ll become bullish and position for early cycle markets.

Until then, watch the data with eyes wide open, seek out data that proves you wrong in order to stay balanced, and rest up before the new year begins. We’re in for another adventure.

Learn More:

This article originally appeared on SoFi.com and was syndicated by MediaFeed.org.

Terms and Conditions Apply. SOFI RESERVES THE RIGHT TO MODIFY OR DISCONTINUE PRODUCTS AND BENEFITS AT ANY TIME WITHOUT NOTICE. To qualify, a borrower must be a U.S. citizen or other eligible status and and meet SoFi’s underwriting requirements. Not all borrowers receive the lowest rate. Lowest rates reserved for the most creditworthy borrowers. If approved, your actual rate will be within the range of rates listed above and will depend on a variety of factors, including term of loan, evaluation of your creditworthiness, years of professional experience, income, and a variety of other factors. Rates and Terms are subject to change at anytime without notice and are subject to state restrictions. SoFi refinance loans are private loans and do not have the same repayment options that the federal loan program offers, or may become available, such as Income Based Repayment or Income Contingent Repayment or PAYE. Licensed by the Department of Financial Protection and Innovation under the California Financing Law License No. 6054612. SoFi loans are originated by SoFi Lending Corp. or an affiliate, NMLS # 1121636. (nmlsconsumeraccess)

✝︎ To check the rates and terms you qualify for, SoFi conducts a soft credit pull that will not affect your credit score. However, if you choose a product and continue your application, we will request your full credit report from one or more consumer reporting agencies, which is considered a hard credit pull and may affect your credit.

More from MediaFeed:

Investment tax rules every investor should know

Investing can feel like a steep learning curve. In addition to having a clear grasp of types of investment vehicles available and understanding the role investments play in overall financial strategy, it’s a good idea to understand how taxes may affect your investments. Knowing tax implications of various investment vehicles and investment decisions can help an investor tailor their strategy and end up with fewer headaches at tax time.

Related: What is leverage?

fizkes / istockphoto

Tax requirements for investments can be complicated, and it can be helpful for investors to work with a professional to see how taxes might impact a return on their investment. Doing so might also help ensure that investors aren’t overlooking anything as they explore avenues for favorable tax treatments.

That said, it’s always helpful to enter into any discussion with some solid background information on when and how investments are taxed. Typically, investments are taxed at one or more of these three times:

- When you sell an asset for a profit. This profit is called capital gains—the difference between what you bought an investment for and what you sold it for. Capital gains taxes are typically only triggered when you sell an asset; otherwise, any gain is an “unrealized gain” and is not taxed.

- When you receive money from your investments. This may be in the form of dividends or interest.

- When all profits from investments are considered under an umbrella. This view may trigger a tax called the Net Investment Income Tax (NIIT).

- In the following sections, we delve deeper into each of these situations that can lead to taxes on investments.

nortonrsx

Capital gains are the profits an investor makes from the purchase price to the sale price of an asset. Capital gains taxes are triggered when an asset is sold (or in the case of qualified dividends, which is explained further in the next section). Any growth or loss before a sale is called an unrealized gain or loss, and is not taxed.

The opposite of a capital gain is a capital loss. This occurs when an investor sells an asset at a lower price than purchased. Why would an investor trigger a capital loss? That depends on the investor. Sometimes, an investor needs to sell an asset at a suboptimal time because they need the cash.

At other times, an investor may sell “losing” assets at the same time they sell assets that have gained as a way to minimize their overall tax bill, by using a strategy called tax-loss harvesting. This strategy allows investors to “balance” any gains by deliberately selling profits at a loss, which, according to IRS rules, can be carried over through subsequent tax years.

Sitthiphong/ istockphoto

There are two types of capital gains, depending on how long you have held an asset:

- Short-term capital gains. This is a tax on assets held less than a year, taxed at the investor’s ordinary income tax rate.

- Long-term capital gains. This is a tax on assets held longer than a year, taxed at the capital-gains tax rate. This rate is lower than ordinary income tax. For 2021, as per the IRS , the long-term capital gains tax was $0 for individuals with taxable income less than $80,0000 and no more than 15% for most individuals (for those making more than $496,600, the rate jumps to 20%).

Pinkypills / istockphoto

Dividends are distributions that a corporation, S-corp, trust or other entity taxable as a corporation may pay to investors. Not all companies pay dividends, but those that do typically pay investors in cash, out of the corporation’s profits or earnings. In some cases, dividends are paid in stock or other assets.

Dividends that are part of tax-advantaged investment vehicles are not taxed.

Generally, taxpayers will receive a form 1099-DIV from a corporation that paid dividends if they receive more than $10 in dividends over a tax year. All other dividends are either ordinary or qualified:

- Ordinary dividends are taxed at the investor’s income tax rate.

- Qualified dividends are taxed at the lower capital-gains rate.

In order for a dividend to be considered “qualified” and be taxed at the capital gains rate, an investor must have held the stock for more than 60 days in the 121-day period that begins 60 days before the ex-dividend date. (Additionally, said dividends must be paid by a U.S. corporation or qualified foreign corporation, and must be an ordinary dividend, as opposed to capital gains distributions or dividends from tax-exempt organizations.)

Both ordinary dividends and interest income on investments are taxed at the investors regular income rate. Interest may come from brokerage accounts, or assets such as mutual funds and bonds. There are exceptions to interest taxes based on type of asset. For example, municipal bonds may be exempt from taxes on interest if they come from the state in which you reside.

Victoria Gnatiuk / istockphoto

")

Net investment income tax (NIIT) is a flat 3.8% surtax levied on investment income for taxpayers above a certain income threshold. The NIIT is also called the “Medicare tax” and, as per the IRS , applies to all investment income including, but not limited to: interest, dividends, capital gains, rental and royalty income, non-qualified annuities, and income from businesses involved in trading of financial instruments or commodities.

In 2021, NIIT applies to individuals with an adjusted gross income (AGI) over $200,000 for single filers and $250,000 for married couples filing jointly. For taxpayers over the threshold, NIIT is applied to the lesser of the amount the taxpayer’s AGI exceeds the threshold or their total net investment income.

For example, consider a couple filing jointly who makes $200,000 in wages and has a NIIT of $60,000 across all investments in a single tax year. This brings their AGI to $260,000—$10,000 over the AGI threshold. This would mean the taxpayer would owe tax on $10,000. To calculate the exact amount of tax, the couple would take 3.8% of $10,000, or $380.

g-stockstudio / istockphoto

Certain types of investments may be exempt from tax implications if the money is used for certain purposes. These investment vehicles are called “tax-sheltered” vehicles and apply to certain types of investments that are earmarked for certain uses, such as retirement or education.

There are two types of tax-sheltered accounts:

- Tax-deferred accounts. These are accounts in which money is contributed pre-tax and grows tax-free, but taxes are taken out when money is withdrawn. For example, a 401(k) retirement account grows tax-free until you withdraw money, at which point it is taxed.

- Tax-exempt accounts. These are accounts—such as a Roth 401(k) or Roth IRA, or a 529 plan—in which money can be taken out tax-free if the funds are taken out according to qualifications. For example, money in a Roth account is not taxed upon withdrawal in retirement.

Beyond investing in tax-sheltered accounts, investors may also choose to research or speak with a professional about tax-efficient investing strategies. These are ways to calibrate a portfolio that may help minimize tax hits, grow wealth, and ensure that key portfolio goals—such as ample savings for retirement or ensuring adequate liquidity —are met.

DepositPhotos.com

Dividends, interest, and gains can add up, which is why it’s important for a taxpayer to be mindful of investment taxes not only at tax time, but throughout the year. Understanding the implications of sales and keeping capital gains taxes in mind when planning sales can help investors make tax-smart decisions.

Because there are so many different rules regarding taxes, some investors find it helpful to work with a tax pro to ensure they’re not overlooking anything in their portfolio. Tax law also varies by state, and a tax pro should be able to tailor strategy to a taxpayer’s home state to minimize liability.

Learn More:

This article

originally appeared on SoFi.comand was

syndicated by MediaFeed.org.

SoFi Invest

The information provided is not meant to provide investment or financial advice. Investment decisions should be based on an individual’s specific financial needs, goals and risk profile. SoFi can’t guarantee future financial performance. Advisory services offered through SoFi Wealth, LLC. SoFi Securities, LLC, member FINRA / SIPC . SoFi Invest refers to the three investment and trading platforms operated by Social Finance, Inc. and its affiliates (described below). Individual customer accounts may be subject to the terms applicable to one or more of the platforms below.

1) Automated Investing—The Automated Investing platform is owned by SoFi Wealth LLC, an SEC Registered Investment Advisor (“Sofi Wealth“). Brokerage services are provided to SoFi Wealth LLC by SoFi Securities LLC, an affiliated SEC registered broker dealer and member FINRA/SIPC, (“Sofi Securities).

2) Active Investing—The Active Investing platform is owned by SoFi Securities LLC. Clearing and custody of all securities are provided by APEX Clearing Corporation.

3) Cryptocurrency is offered by SoFi Digital Assets, LLC, a FinCEN registered Money Service Business.

For additional disclosures related to the SoFi Invest platforms described above, including state licensure of Sofi Digital Assets, LLC, please visit www.sofi.com/legal. Neither the Investment Advisor Representatives of SoFi Wealth, nor the Registered Representatives of SoFi Securities are compensated for the sale of any product or service sold through any SoFi Invest platform. Information related to lending products contained herein should not be construed as an offer or pre-qualification for any loan product offered by SoFi Lending Corp and/or its affiliates.

Tax Information: This article provides general background information only and is not intended to serve as legal or tax advice or as a substitute for legal counsel. You should consult your own attorney and/or tax advisor if you have a question requiring legal or tax advice.

External Websites: The information and analysis provided through hyperlinks to third party websites, while believed to be accurate, cannot be guaranteed by SoFi. Links are provided for informational purposes and should not be viewed as an endorsement.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

Crypto: Bitcoin and other cryptocurrencies aren’t endorsed or guaranteed by any government, are volatile, and involve a high degree of risk. Consumer protection and securities laws don’t regulate cryptocurrencies to the same degree as traditional brokerage and investment products. Research and knowledge are essential prerequisites before engaging with any cryptocurrency. US regulators, including FINRA , the SEC , and the CFPB . PDF File, have issued public advisories concerning digital asset risk. Cryptocurrency purchases should not be made with funds drawn from financial products including student loans, personal loans, mortgage refinancing, savings, retirement funds or traditional investments. Limitations apply to trading certain crypto assets and may not be available to residents of all states.

g-stockstudio / istockphoto

g-stockstudio/istockphoto

Featured Image Credit: Pinkypills / istockphoto.