If borrowers were challenged to repay student loan debt before the coronavirus struck, you can imagine their plight in the pandemic’s wake.

Due to preexisting challenges and a new widespread loss of income, more than one-third of student loan borrowers are suffering from food insecurity, and a majority of them (6 in 10) are generally struggling to cover their expenses, according to our survey of 1,000-plus in student loan debt. And in just May alone, four in 10 missed payment on at least one bill or debt payment.

As our findings show, relief efforts — such as the federal student loan repayment suspension and the one-time economic impact payments (a part of the Coronavirus Aid, Relief and Economic Security Act, or CARES Act) — haven’t done enough to remedy repayment for many borrowers.

Editorial note: This content is not provided or commissioned by any financial institution. Any opinions, analyses, reviews or recommendations expressed in this article are those of the author’s alone, and may not have been reviewed, approved or otherwise endorsed by the financial institution.

Image Credit: DepositPhotos.com.

Methodology

Student Loan Hero commissioned Qualtrics to conduct an online survey of 1,042 student loan borrowers. The survey was fielded between May 26 and May 29, 2020.

Image Credit: Joerg Siegert/iStock.

Student loan borrowers losing income, confidence in their finances

You don’t have to lose a job to see your household income take a hit, as our survey respondents can attest.

About 1 in 10 reported being the victim of a layoff or furlough, yet more than a third saw their wages or hours drop below normal. Likewise, about half of borrowers have seen their earnings decrease, echoing the 51% figure highlighted in another of our recent surveys, which specifically covered private student loan borrowers affected by the coronavirus pandemic.

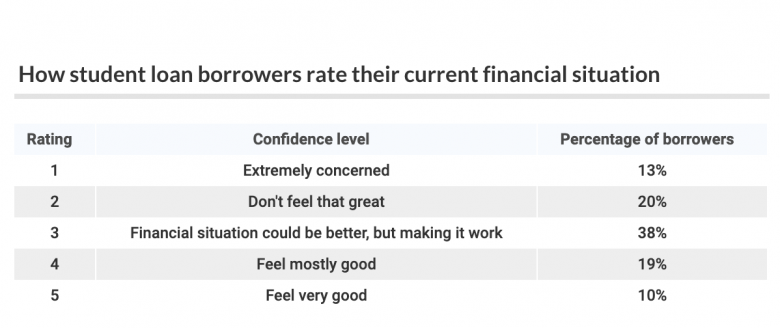

A decrease in income has led some borrowers to lose confidence in their personal finances. In fact, about 1 in 7 borrowers reported being “extremely concerned” about their current financial situation.

Along racial lines, borrowers who identified as Black or Hispanic were more likely to rate their current situation as a 1, the lowest possible score on a five-point scale, than those who were white or Asian.

Fortunately, the government has allowed a suspension on student loan repayment (see more below under “Federal loan suspension”), and even when that expires, there are income-driven repayment plans available to make payments more affordable. Support programs for private student loans may be harder to come by, but many lenders have provided breaks during the coronavirus outbreak.

Image Credit: StudentLoanHero.

Borrowers struggle to cover essential needs, pay bills

Of course, a drop in wages leaves less money to go around for all expenses, not just student loans. In some cases, just putting food on the table is a struggle.

Nearly half of respondents whose jobs were impacted by the coronavirus said food insecurity was a pressing issue for their family. And even when including all borrowers, more than one-third (36%) reported either a “little” (28%) or “great deal” (8%) of problems getting enough to eat.

The proportion of those suffering food insecurity rose to 45% among those with children under 18.

Food insecurity is top of mind for many student loan borrowers still on campus. More than a quarter of enrolled teens and 20-somethings were having trouble paying bills or feeding themselves, according to our survey of college students affected by the coronavirus pandemic.

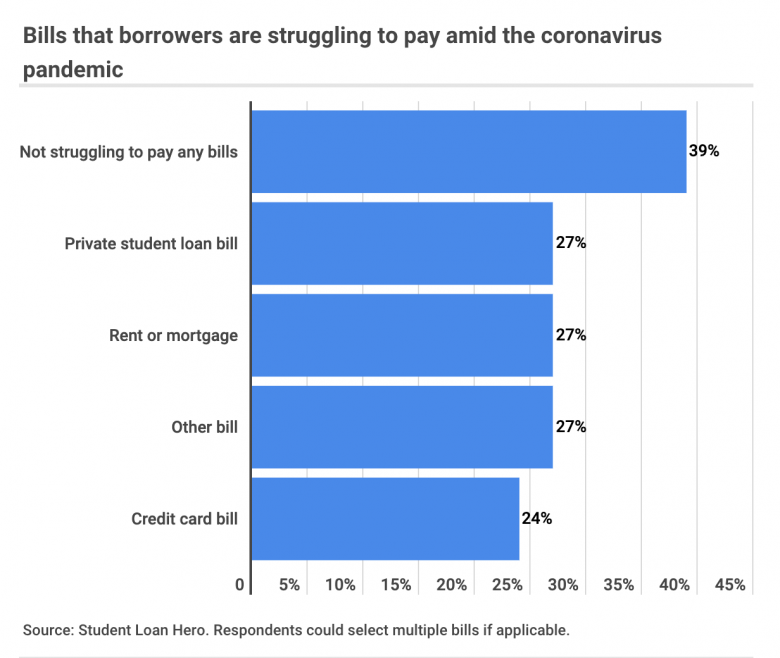

In just May alone, 4 in 10 borrowers reported missing a recurring payment, leaving them delinquent on at least one type of consumer debt. That proportion rose to 53% among those who were laid off or furloughed or saw their wages or hours trimmed. More broadly, about 77% of borrowers whose income was impacted by the ongoing pandemic said they were having trouble covering one or more of their monthly bills.

Most commonly, 17% of all respondents weren’t able to make their credit card payment — this is concerning, since these tend to have some of the highest interest rates among different debt types. About 15% of respondents also failed to meet their private education loan dues; private loans, it should be noted, typically carry higher interest rates than federal loans.

Image Credit: StudentLoanHero.

Federal loan suspension, economic impact payments prove some measure of relief

As noted above, federal student loan borrowers have a six-month, interest-free payment suspension, lasting through September, thanks to Congress’ CARES Act. That reprieve gave millions of student loan borrowers a chance to catch their breath.

While federal loan borrowers are divided evenly on whether to keep sending payments, those who suffered a loss of income were less likely to stay current.

Just 40% of borrowers whose jobs have been affected by the worsening economy have elected to remain in active federal loan repayment, compared with 58% whose wages weren’t shaken by the pandemic.

Image Credit: StudentLoanHero.

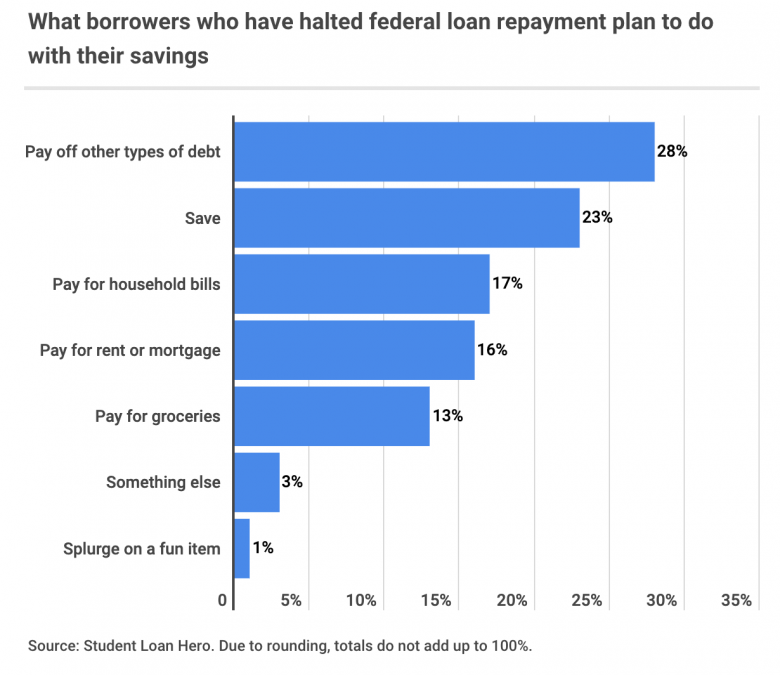

Student loan borrowers are spending their economic impact payments on household bills

The six-month federal loan repayment suspension has famously excluded some federal and all private loan borrowers. On the other hand, economic impact payments have been more accessible (even if these payments haven’t made it into the hands of college students).

About 83% of our respondents have received or expect to receive an economic impact payment, which runs up to $1,200 per eligible individual.

Image Credit: StudentLoanHero.

How to survive student loan repayment during the pandemic

No matter how the ongoing coronavirus crisis may have muddied your student loan repayment, there are, thankfully, plenty of supportive resources.

If student loans seem like the lightest of your concerns, focus your energy elsewhere for now. Consult charitable organizations to help cover the basics, particularly if you face food insecurity or other priority issues. Once you’ve met these needs, revisit your student loan repayment and set a path forward.

Aside from the federal loan repayment suspension and the option to lower your monthly payment via income-driven repayment plans (mentioned above), all student loan borrowers should contact their lender to check up on their options.

While you’re at it, review your state-offered resources, particularly if you hold private loan debt. Our student loans and coronavirus interactive quiz could also point you in the right direction.

Borrowers whose income, credit score and student loan repayment have gone unaffected by the coronavirus pandemic might consider student loan refinancing to take advantage of the current drop in interest rates. By refinancing your education debt with a private lender, you could score a lower rate and a single monthly payment.

However, federal loan borrowers should think twice about refinancing, as it would irreversibly strip their government-held debt of unique safeguards like IDR plans and loan forgiveness programs.

This article originally appeared on StudentLoanHero.com and was syndicated by MediaFeed.org.

Image Credit: iStock/jacoblund.