Editor’s note: The opinions in this article are the author’s, and do not necessarily represent the views of MediaFeed.com.

I have spent most of my career working for large financial institutions like Citigroup, Merrill Lynch, Credit Suisse, Charles Schwab and many more. Most of my time and effort was spent helping these companies understand the various customer segments for whom they could launch products in global markets. In my time, I learned one basic rule:

Companies focus on making products for, and selling products to, their most profitable customers. The rest of us are just along for the ride.

Customer needs vs. company profits

By looking at this from a financial institution’s perspective — pretty quickly I can tell that big financial companies just aren’t focused on me as a customer. I am not one of those customers that trades 50x a month or has ½ million dollars in my bank account — and many of these companies won’t give me the time of day. They spend much of their time and money getting me to sign up as a customer and then forget all about my experience and needs once I’ve transferred my assets.

That’s not to say that they won’t be trying to convert me into a more profitable customer. In a previous life, I spent considerable time developing strategies to maximize lifetime value of customers for financial firms:

- Requests to move money into an expensive managed product, pitched as expert advice where they can charge higher rates for your assets, and make more money

- Recommendation to bring money from other firms under the guise of “consolidation”, pitched as a convenience to me, while they now have more assets to charge a fee on, to make more money

- Periodic sales calls to get me to “talk to an advisor”, who are largely trained salespeople to help the company identify areas where they can make more money

Anyone seeing a pattern here? No knock to these companies, there are clearly some customers that want or need to consolidate their money into managed products or get guidance from an advisor. My issue is that I’m just not one of these customers — I don’t feel the need to “talk to an advisor”. I like to keep accounts at multiple firms, I currently have 2–3 brokerage accounts that I use for varying goals. So as a customer, I find myself wondering: “What exactly are these companies doing for me?”

The money trail

Most discount brokers are moving away from the trading space and diversifying into higher-margin products. This isn’t a new phenomenon; the writing has been on the wall for decades. Different firms are focusing on different things; Schwab tries to sell me advice, whereas Northwestern Mutual can’t believe I don’t want even more life insurance. Everyone has a mortgage provider or credit card partner for whom I would be a great customer. I wish they would focus on making the experience better for products I am using, vs. trying to get me to use more of their products that have a stale experience.

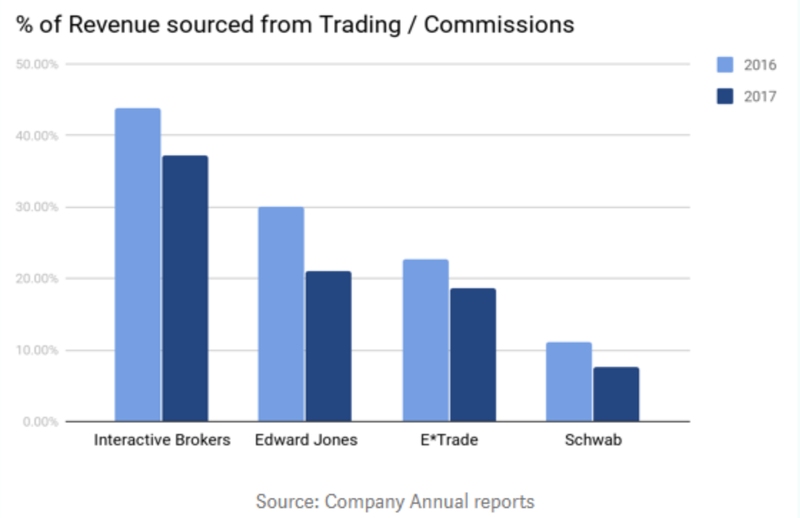

I realize these are businesses and they need to focus on making the most money; I spent years helping several do just that. The shift away from individual brokerage customers like me becomes pretty self-evident when you look at the earnings of some of the larger public brokerage firms. Revenues from self-directed brokerage continue to be a smaller portion of total annual revenues. Brokerages have spent the last decade leaving behind their initial customers and moving towards charging to give advice — “Wealth Management”. Trading now makes up a minimal portion of annual revenues. Even Interactive Brokers, the stalwart platform for self-directed investors, makes less than 50% of their revenue from trading commissions.

This data shows that these companies are focused on creating alternate sources of revenue (read: selling managed products, advice, funds, etc.) and not truly cultivating the trading customer base. All of these companies are investing in back-end infrastructure to be able to monetize your cash. A number of discount brokers have launched their own ETFs as another channel to capture revenue. Most banks/brokers are launching some variation of a robo-advisor as it’s a scalable way to gather assets. In spite of all these product launches within brokerages, I haven’t seen much innovation in my self-directed trading accounts in quite some time.

Who’s thinking about me as a customer?

There has been a lack of innovation in the self-directed space for a long time. In the startup space, the two key areas where I’ve seen disruption are decreased fees for market access, and the ability to trade esoteric asset classes (e.g., real estate or cryptocurrencies). Lowering pricing isn’t product innovation, it’s a marketing strategy. For me, the current trading products on the market aren’t worth paying for — but I would be willing to pay for the right product. As far as other asset classes, I’m not sure how much of my portfolio I really need to invest in real estate/cryptocurrencies for long-term growth and/or diversification.

The larger companies continue to be focused on their most profitable customers — and are leaving behind the rest of us — everyday customers that may not fit a typical “active” trader profile but are instead a “buy and hold” investor or a “monitor but trade infrequently” investor. Clients in these categories spend a majority of their time on monitoring potential trades and discussing investment ideas with friends.

I’ve long been frustrated by the lack of options in the self-directed space. It’s an open secret in the industry that trading just doesn’t make the kind of money advice does — and if you want innovation, look at advice.

The future of individual investing

Finding new trade ideas for me is a combination of chatting with friends, reading news articles through a variety of portals (e.g., Apple Stocks, Bloomberg) and seeking/providing guidance on investment forums (e.g., Seeking Alpha, Yahoo Finance). This has historically been, and continues to be, a cumbersome process across the multiple online and offline platforms. This use-case has never been a priority for banks as the customer base doesn’t justify the cost of upgrading their legacy systems.

Many of us learned about the efficient frontier in finance class during undergrad. I’ll hypothesize that most traders don’t ensure that their portfolio is maximizing returns while minimizing risk — certainly, I’ve never found a good tool for this as an individual investor. In my experience, most trading volume is driven by cash on hand/access to margin; not a rigorous analysis. Personally, I rarely sit and do the calculations for my actual stock portfolio. I invest in industries that I think aren’t heavily correlated and place a mix of short and long-term bets, but outside of that — I know I need help to ensure I’m appropriately balancing my risks and rewards while selecting my own stocks.

That last piece is essential. Many advisors can help you balance risk/reward through managed products, index funds or specialized ETFs, but they do not help the average investor with a truly customized portfolio. And I don’t want someone to invest on my behalf, but instead, want some assistance in helping me invest smarter.

Vote with your assets

At the end of the day, I asked myself “Why am I paying these companies that can’t give me what I want?” And let’s be honest — we are paying them — be it through commissions, or what they earn on the cash sitting in our bank accounts. Just as companies choose the customers that help their bottom line — the power is now in the hands of the traders to choose the company that maximizes their bottom line.

About the Author

Rohit Gera has worked across various sub-industries within Financial Services throughout his career. Much of this work is offering strategic guidance to large and small companies in areas of market entry, product growth strategy (digital and non-digital), and overall strategic planning. He has worked as a strategy consultant at Deloitte Consulting with clients ranging from retail banks, insurance companies, investment banks, and brokerages. In his last role, he was a Managing Director for Strategy at Charles Schwab, where we worked on digital growth strategy, international market entry, and overall strategic planning. He has also been a mentor for Startup Leadership (Silicon Valley), and an adviser for StartupBootcamp NYC — Fintech.

All views expressed in this article are Rohit’s own and do not necessarily reflect the position of Nvstr Financial LLC (“Nvstr”) or its affiliates. This communication is for discussion purposes only. Neither Nvstr nor the author endorses any linked content. Statements herein may not be representative of the typical experience of Nvstr customers and are no guarantee of future performance or success. The contents of this article and of nvstr.com are not investment advice or a recommendation of a securities transaction or investment strategy. This is not an order, solicitation, or offer to buy or sell securities or business interests. Investing in stocks is inherently risky; using margin may increase these risks.

Nvstr is a member firm of FINRA and SIPC. Further information can be found at nvstr.com/about and on FINRA’s BrokerCheck website.

This article originally appeared on Nvstr.com and was syndicated by MediaFeed.org.

Featured Image Credit: g-stockstudio/iStock.