If you are a small business owner, the financial resources of your customers can play a key factor in your company’s success. Customer financing, such as buy now, pay later services, can encourage shoppers to complete their purchases.

Customer financing can be a win-win situation for both customers and business owners, but it also comes with extra steps, such as managing a customer credit policy. Let’s explore the types of financing you can offer, how to implement them, and your alternative options.

What is customer financing?

Customer financing is a program or service a business offers to help customers pay for products, goods, or services over time. Usually, financing involves an application process where the customer’s overall credit risk is assessed with a credit check.

Types of customer financing

By offering customer financing, businesses may attract more customers who aren’t able to afford the full cost of a product or service upfront. Additionally, customer financing, which provides an additional payment option, can help businesses increase sales.

The main options for customer financing are primary financing, which considers creditworthiness, and secondary financing, which is open to all sorts of credit. Most customer financing methods are primary financing, while secondary financing includes such services as lease-to-own arrangements.

(In-house) financing

In-house financing is where a business acts as a creditor and offers its own financing program to customers. This is a more involved process for the business than third-party financing.

For in-house loans, you may need to pay costs associated with credit checks and collecting payments, which require both software and staffing. You’ll also need to develop a credit policy for your business and have a system to manage your accounts receivable.

Note that accounting software may help simplify the payment process with invoices and automated payment reminders—potentially freeing up time to focus on your business.

Third-party financing

Third-party financing refers to a type of financing where small business owners rely on a third-party provider to act as a lender at the point of sale. In most of these programs, the customer enters into a payment plan to pay off a purchase’s full amount over time, often through monthly payments.

Third-party financing companies allow a wide range of credit to be approved compared to other, more strict forms of financing. In some cases, these financing programs are interest-free, while others might assess interest charges at set interest rates.

One of the most popular forms of third-party financing is the buy now, pay later model—a form of short-term financing that’s typically interest-free. Buy now, pay later financing is a popular tool for online retailers.

The fees and expenses of third-party financing apps are typically a fixed amount per transaction (such as 30 cents) and a percentage of the sale.

For example, a $300 sale using customer financing could include a $0.30 fixed charge for you, as well as 3.29% of the sale. Thus, the fees would be $10.17, which is the $0.30 fixed charge, plus $9.87 ($300 x 3.29%).

The trade-off of these fees is that third-party financing companies handle credit checks and payment collection.

Customer financing alternatives

Some businesses may find third-party financing too expensive or unavailable for their industry. As a result, you may look into other ways to encourage customers to make their purchases.

For example, service-based businesses like plumbing and HVAC companies can partner with specialized companies to provide financing. Simply accepting credit card payments could be another way to boost sales if customer financing isn’t possible.

Layaway is another option you can offer. It’s a payment plan where a business reserves a product for a customer until the customer pays for the item, typically with a series of partial payments.

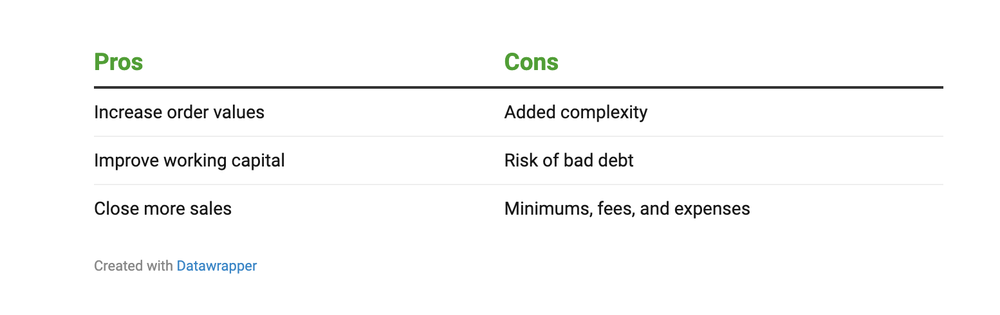

Pros and cons of customer financing

Small business owners should evaluate both the benefits and drawbacks of offering customer financing. We’ve summarized some of the pros and cons below:

Benefits of customer financing

- Increase order values: Businesses offering customer financing may see higher average orders. Larger orders mean more revenue to boost your bottom line. Plus, customers get to buy the product they want instead of a lower-cost option.

- Improve working capital: When you offer payment plans and financing options to customers, it may allow you to invoice customers who would otherwise pay in arrears so you can receive a partial payment upfront instead. Receiving payment upfront, even if it’s only a partial payment, improves your cash flow management and gives you access to working capital.

- Close more sales: The initial upfront cost can be an obstacle for customers deciding whether to make a purchase. However, if you can break up the cost of a product or service with a payment plan, customers might be able to afford those smaller payments.

Drawbacks of customer financing

- Added complexity: Offering in-house financing can add time and complexity to payments. Using the right tools can help you automate the added bookkeeping required to account for financing and payment plans. QuickBooks can help automate recurring payments, allowing business owners to accept payments online. QuickBooks also offers an invoice advance program called Get Paid Upfront that allows you to get funded for approved invoices.¹

- Risk of bad debt: Although allowing financing can be a great way to get new customers, businesses that offer to finance assume some risk due to the possibility customers will not make payments according to the agreed terms. Establishing and enforcing a servicing or collections policy can help ensure you have safeguards in place to protect against bad debt.

- Minimums, fees, and expenses: If you use a third-party financing provider, you will likely have to pay fees for it. In some cases, you will need to pay a flat monthly fee, while other providers may charge a percentage of each transaction. Some providers also require a certain transaction amount before you can offer financing to customers during the checkout process.

How to offer credit to customers in 4 steps

Introducing financing options for customers can encourage customer loyalty. Offering credit can be especially useful for high-ticket items or for customers who prefer paying in installments.

Here’s a straightforward, four-step process to consider for offering credit to your customers, making it easy for them to shop now and pay later while driving growth for your business:

1. Review your options

In step one, you’ll evaluate whether it makes more sense to offer in-house or third-party financing. With in-house financing, you have more control, but you also bear the responsibility of collecting payment. On the other hand, you avoid the fees and expenses that can come with third-party financing.

Third-party financing also might not be an option for your industry. Third-party apps work well for retailers and e-commerce stores, but they might not be a good fit for businesses like wholesale distributors, professional service firms, or manufacturers.

When choosing a third-party financing option, consider:

- Interest and fees the service or app will charge customers

- The application process for customers

- Credit limits they offer

- Expenses they will charge your business

- Additional tools or services they offer

You want to make sure your in-house process or the third-party service process is not too cumbersome for customers. Also, make sure either process offers a high enough credit limit for customers to actually complete the purchase.

2. Pick an option

If you decide to go the in-house route, you’ll want to then start working on in-house policies, such as terms and conditions and methods for automating recurring payments. Additionally, you’ll want to decide on a credit application process. Note that in-house financing means you’ll have to dedicate more time to accounts receivables.

If you go with third-party financing, you’ll want to decide on a service that is easy to implement. You also want a service that does not make the checkout process cumbersome for the customer.

3. Implement it

Once you have your financing plan, it’s time to implement it. For in-house financing, this means creating an accounts receivable collection process. In particular, you’ll want to:

- Prepare your accounting system for accounts receivable journal entries

- Create a credit system for determining customer creditworthiness

- Set the credit terms you’ll offer, such as flexible payment terms

For third-party financing, you’ll need to add your financing option to the checkout process. This means adding it to your product pages, checkout pages, and point-of-sale systems.

4. Let customers know

Once you have everything in place, it’s time to let customers know about it. This can include email marketing or adding marketing to your website. You can also announce the financing via social media. More importantly, you’ll want to advertise on your product pages.

Choose the best payment setup for your business

At the end of the day, it’s your decision whether you want to offer a financing program or financing options to your customers. Whether you decide on a third-party company or to provide financing in-house, these financing solutions can mean more sales.

When you do make a sale, you can make it easier to get paid with recurring invoices and by enabling digital payments via your payments software.

This article originally appeared on the QuickBooks Resource Center and was syndicated by MediaFeed.org.

More from MediaFeed:

Home businesses tax deductions to take as a small business owner

Small business owners take on a considerable amount of responsibility. Beyond serving clients, they must also take care of all the minutiae of running a business, including keeping track of expenses they can deduct as a small business owner.

Fortunately, small business owners and entrepreneurs who use their home for work can benefit from various home business tax deductions that help them reduce their taxable business income. Common deductions include office supplies, software and internet access, but deductions can vary widely depending on the type of home business you run.

- Who qualifies for home business tax deductions?

- 25 home business tax deductions for your small business

- How to write off home business expenses

StockRocket/istockphoto

If you run your business out of your home, you may be able to deduct expenses for the use of your residence on your taxes for your small business. The home office deduction can be utilized by homeowners and renters, and any type of residence can qualify (single-family home, condominium, manufactured housing, etc.).

To qualify for the home office deduction, your home business activities must meet the following criteria:

- Regular and exclusive use. According to the IRS, you must “regularly use part of your home exclusively for conducting business.” In other words, you must have a space in your home that you use only for business purposes, such as a home office or extra room that is used only for business and never for personal use.

- Principal place of business. To qualify for the home office deduction, your home also must be the principal place your business operates from, although there are exceptions. The IRS reported that you may qualify for the home office deduction if you also have a business location outside of your home, provided you use your home for a substantial component of your business. For instance, if you conduct business in another location but have meetings with clients or patients in your home, the IRS allows you to deduct expenses for the part of your home that you use “exclusively and regularly” for business purposes.

There are some exceptions to these rules, including for those who run a home daycare. If your small business involves watching children in your home, then it would be impossible to meet the “exclusive use” criteria if you’re watching children in your own living area. To qualify for this exception to the exclusive use rule, you must provide daycare for children, persons age 65 or older or persons who are unable to care for themselves. Additionally, you must have “applied for, been granted or be exempt from having a license, certification, registration or approval as a daycare center or as a family or group daycare home under state law,” noted the IRS.

Suradech14/istockphoto

If you’re eager to reduce your taxable income this year, figuring out which home business tax deductions you can take is a smart first step. Here are 25 common deductions you may be able to qualify for.

monkeybusinessimages/istockphoto

Business supplies and office expenses, such as office furniture, printer paper, pens, calculators and business cards, are deductible provided they are for business use. According to the IRS, business expenses must be both ordinary and necessary, meaning they are “common and accepted in your trade” and “helpful and appropriate,” though not necessarily indispensable.

Ridofranz/istockphoto

Small business computers and software you need to purchase for your business, including small business accounting software, should be tax-deductible business expenses provided these purchases are ordinary and necessary for your business to remain in operation.

monkeybusinessimages/istockphoto

You may also be able to deduct home repairs and maintenance performed on your place of residence, but only for the part of your residence that is used exclusively for business purposes. According to the IRS, an example could include “painting or repairs only in the area used for business,” like a new coat of paint or replacement flooring in your home office.

dima_sidelnikov/istockphoto

You can deduct the business portion of your rent as an expense if the property you rent is for use in your trade or business. However, you cannot deduct rent as a business expense if you have or will receive equity in or a title to said property. Per the IRS, rent is defined as “any amount you pay for the use of property you do not own.”

In terms of depreciation, the IRS said that you can typically deduct depreciation on the business use portion of your home as well, in an amount up to the gross income limitation over a 39-year period.

monkeybusinessimages/istockphoto

If you have a home office, your house utilities will also be required for your business. As a result, you can deduct a portion of your utility bills, such as gas and electric bills. However, you can only deduct a portion of these expenses since, obviously, part of your utility bills are for personal use.

m-imagephotography/istockphoto

If you use your car for business purposes, you can deduct auto-related expenses for the business use of a car. The IRS also reported that, if you use your car for both personal and business use, you must divide your car expenses based on the mileage you drive for personal and business purposes.

FlamingoImages/istockphoto

You can also deduct mileage for all travel related to business. The IRS offers a table of standard mileage rates and mileage deduction rules you can refer to for the last several years, including mileage expenses for 2020.

tommaso79/istockphoto

You can also write off employees’ pay as a small business owner. This is true even if you operate your business out of a home office.

KapturePhotoSolution/istockphoto

You can also deduct contributions to retirement plans, including tax-advantaged retirement plans for the self-employed or small business owners, such as an SEP IRA or a solo 401(k).

LightFieldStudios/istockphoto

If your business is paying interest on a credit card or loan that you borrowed for business activities, you should also be able to deduct this interest as a business expense.

Liderina/istockphoto

According to the IRS, you may be able to deduct various federal, state, local or foreign taxes that are directly related to your trade or business.

chatsimo/istockphoto

You can typically deduct the cost of business-related insurance products you pay for, provided they are applicable to your trade or profession.

SamuelBrownNG/istockphoto

If your business creates products or purchases them for resale, you can typically deduct the cost of these products or the costs involved in manufacturing them. This can include the cost of raw materials, freight, shipping, storage, direct labor and more.

chachamal/istockphoto

Thanks to the Tax Cuts and Jobs Act of 2017, you may be able to deduct up to 20% of your qualified business income on your taxes. This deduction does have limitations based on your trade or business as well as how much you earn, however. Specifically, joint tax filers with incomes below $315,000 and other filers with incomes below $157,000 can claim this deduction in full provided they work in a qualifying industry. For 2018, joint tax filers with incomes between $315,000 and $415,000 and individuals with incomes between $157,000 and $207,500 were subject to phase-outs.

Jelena Danilovic/istockphoto

If you use your home for business purposes, you can generally deduct cleaning services and supplies that you purchase for the business-related portion of your home.

AndreyPopov/istockphoto

If you own your home and have a home mortgage, you can deduct a portion of your mortgage interest on your business taxes. Deductions are based on the percentage of your home that you use for your business. If your lender requires mortgage insurance, part of that can be deducted as well.

rrecrutt/istockphoto

Business-related travel expenses can also be taken as a business expense. This could include travel to meet with clients or to professional education or training events.

jacoblund/istockphoto

If you pay for professional services, such as legal advice or tax preparation, these expenses can be deducted as business expenses.

Jacob Ammentorp Lund/istockphoto

If you pay for marketing help or a business coach, these expenses can be deductible from your business income.

shironosov/istockphoto

If you ship items for business purposes, shipping costs can be deductible on your taxes. The same is true for postage when used for business purposes.

Chaay_Tee/istockphoto

A security system that protects the doors and windows in your home from intruders can also be partially deductible as a business expense, provided part of your home is used for business purposes.

Zinkevych/istockphoto

Professional memberships you pay for and subscriptions to business-related publications can also be tax-deductible.

FlamingoImages/istockphoto

The IRS said that while the first local telephone landline in your home is not a deductible business expense, “charges for business long-distance phone calls on that line, as well as the cost of a second line into your home used exclusively for business, are deductible business expenses.”

Ridofranz/istockphoto

Health insurance for yourself and your family is deductible as a business expense when you’re self-employed, although you do not have to have a home office to qualify for this deduction.

FlamingoImages/istockphoto

If you pay for or reimburse education expenses for an employee, you can deduct the expenses if they are part of a qualified educational assistance program, per IRS rules.

Poike/istockphoto

If you’re feeling overwhelmed by all of the home office business expenses you might have to keep track of, you should know that the IRS also offers a standardized home office deduction that requires less legwork upfront. Here are the two options you have when it comes to how to write off home office business expenses this year:

- Simplified home office deduction: Since the 2013 tax year, taxpayers have been able to access a simplified option for computing the home office deduction. This option lets you determine a standard deduction based on the square footage of your home office space, thus letting you avoid tracking and reporting all of your individual home office expenses. Of course, the simplified method isn’t perfect since you can’t take some deductions like depreciation. You also cannot carry over a loss from a previous year, which is a departure from the regular method.

- Regular method: If you keep excellent records and prefer to deduct business expenses the old-fashioned way, you are still able to do so. With this method, you would need to keep detailed records of all your actual expenses for your home office including mortgage interest, utilities, depreciation and more. From there, your deduction will still be determined based on the percentage of your home used for business purposes.

If you’re using the regular method, you should plan on using IRS Form 8829 for certain business-related tax deductions when you file your taxes. But be aware that some business expenses don’t fall under the home office deduction, so they would be deductible within other areas of your taxes, such as Schedule C or F. Examples include telephone expenses, dues and salaries.

Also note that if you use the simplified method and itemize deductions, you can deduct some expenses for your home that are otherwise deductible, including mortgage interest and property taxes, as itemized deductions using Form 1040 or 1040-SR, Schedule A.

When choosing which method to use for your home office deduction, keep in mind that both options have pros and cons. The regular method requires a lot more work, but you have the potential for a larger deduction if you have a lot of qualified expenses within a year. The simplified method is easier, but not necessarily ideal if you want to recapture depreciation when you sell your home, or if you want to be able to carry over losses. Make sure you understand each method and its limitations so you can make an informed decision.

This article originally appeared on LendingTree.com and was syndicated by MediaFeed.org.

DepositPhotos.com

Featured Image Credit: DepositPhotos.com.