It’s a fact that anyone who has ever made an online purchase using a credit card likely knows all too well: credit cards have a lot of numbers. The credit card number itself can be as long as 19 digits — and those aren’t the only numbers that appear on a person’s card or that a consumer may be asked to provide when making a payment.

Although it might seem like it to anyone who isn’t up on terminology about credit cards, those numbers aren’t random. Each credit card contains unique numbers that provide information about the credit card, offer security, and fulfill other functions. Keep reading to learn what all those numbers on the back (and front) of a credit card actually mean.

How Many Digits Are in a Credit Card Number?

A credit card number — the string of numbers that appear on the front of a card — can be as short as eight digits and as long as 19. Most cards land on the longer side, with 15 to 16 numbers on average. However, there is no defined length for credit card numbers.

Whether long or short, the digits within a credit card number reveal some key information. For instance, they contain embedded information about the card itself, such as the brand of the credit card.

(Learn more: Personal Loan Calculator)

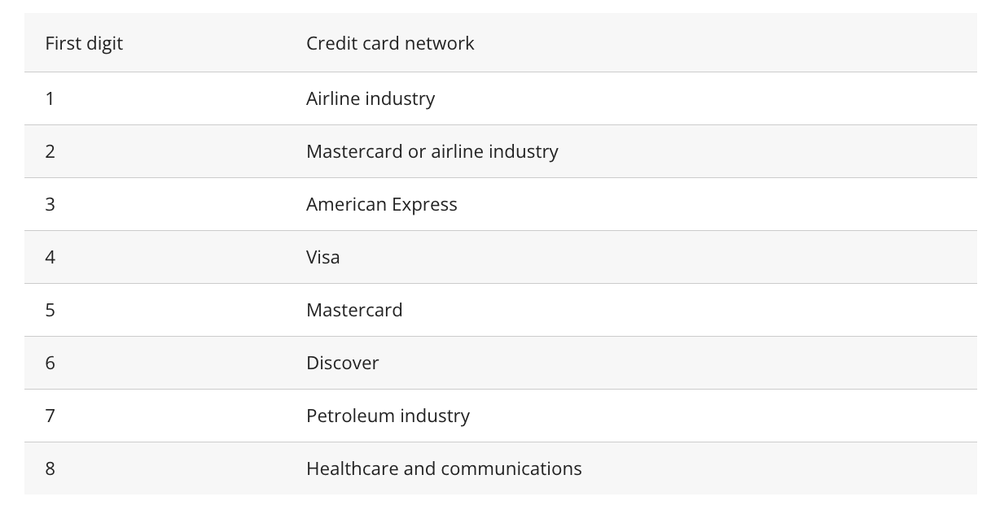

The First Digit: Major Industry Identifier (MII)

Unless it’s a specialty card, the first digit in a credit card number often reflects the credit card network to which a card belongs. This typically holds true regardless of which bank issued the card.

This means that knowing whether a card is a Visa or Mastercard, for example, can often come down to checking that first digit. In some cases, however, the first digit of a credit card may reflect the industry with which the card is affiliated, as you can see in the table below:

The First Six Digits: Issuer Identification Numbers (IIN)

The next five digits in a credit card number reveal information about the credit card issuer, such as a bank or credit union. Together with the first digit on a credit card, the first six digits together make up the Issuer Identification Number (IIN).

This number indicates what type of credit card it is and where it was obtained. However, because a bank may have different products and brands, a person who looks at a number of credit cards from the same issuer may find that these numbers do indeed vary.

The 7-18 Digits: Account Numbers

While the digits that make up a credit card’s Issuer Identification Number would be the same for any cardholder who has the same type of credit card issued by the same financial institution, that’s not the case with the next group of numbers in the string.

Starting with digit seven, the next numbers — up until the final number — are account identifiers that reflect the cardholder’s unique account. These numbers may or may not be the same as the credit cardholder’s account number. If the two numbers are different, the cardholder should be able to find both when reading a credit card statement, even though only the account identifier would appear on the actual card.

In the event that a credit card is lost or stolen, these numbers would be changed on the replacement card.

Why Do Card Number Lengths Vary?

Because there is no standard length for credit cards, the length of the account number will vary depending on the length of the entire credit card number.

For a typical 16-digit credit card, the account number would consist of nine numbers, comprising digits seven through 15. Because American Express cards only contain 15 digits in the credit card number, the account numbers for those cards are only eight digits long. But if a credit card was, say, just 10 digits long, the account number would only consist of three numbers.

The Final Number: The Validator

The last digit in the string that comprises a credit card number is not part of the account number. Rather, it’s called the validator (and sometimes the checksum or check digit). While this digit doesn’t say much on its own, it functions as a secret check to ensure a credit card number is valid.

The validator works by applying a mathematical formula, called the Luhn algorithm, to all of the digits in a credit card number. Once those numbers are plugged into the formula, the result would be the same as the validator number. If the number is not the same, it suggests that there is an inaccuracy, such as a typo in the credit card number provided or the transposal of two digits.

This algorithm is often embedded in payment processors and not something a cardholder or merchant would check manually.

Numbers on the Back of Your Card

Now that we’ve covered the credit card number, what about all those digits on the back of the card? Here’s what they are and how they’re used.

Expiration Date

The credit card expiration date indicates when a credit card is valid until. This number may appear on either the front or back of the credit card. It consists of a month and a year, and a cardholder may continue to use their card until the last day of the month indicated.

Although a credit card expiration date lets a person know when their card will need to be replaced, it also provides a security function. That’s because if someone is able to illegally obtain another person’s credit card number, they may not also have access to the card’s expiry date.

Often when making a purchase, the requested credit card details will include that date. This may be in a four-digit (month and last two digits of the year) or six-digit (month and all four digits of the year) format. In such instances, if the purchaser is unable to provide both numbers, or enters the wrong expiry date, the authorization would fail.

CVV

There’s another number on a credit card that is also used for security purposes, called the Card Verification Value or CVV. It’s also sometimes called the security code.

The CVV is a random number intended to reduce unauthorized credit card use. It is not the same as one’s security PIN. For most credit cards, this is a three-digit number that appears on the signature strip on the back of the card. American Express cardholders can find their four-digit CVV on the front of their credit card.

Similar to the expiry date, a CVV is information that an unauthorized user would not have if they were able to access a credit card number on its own. If the CVV and credit card number do not match, a transaction (whether for a shopping spree or someone buying bitcoin with a credit card) should fail.

More Secure Technologies

While your various credit card numbers can provide some security, they’re not the only thing keeping your card secure.

Traditionally, credit cards have what’s called a magnetic stripe, or magstripe. This strip is typically located on the back of a card. When the card is swiped, its account number is transmitted to complete the purchase.

However, as this technology has shown security flaws, credit card issuers have started to phase it out. Often cards will also have a smart chip, which is able to encrypt your information and generate a unique code for each transaction, making your information harder to steal. Rather than swiping your card with a chip (known as an EMV card), you’ll dip it into a chip reader.

Companies are also starting to look into biometric cards, which would use both a chip as well as an identifying feature, such as a fingerprint, to offer an extra layer of security.

Credit Card Number vs Account Number

With all this talk of numbers, you may be wondering: is there a difference between a credit card number and an account number? Many people think these are one in the same, but they aren’t. Whereas your credit card number appears on your physical card, your account number is on your credit card statement.

If you need to replace your card because it is stolen or lost, you will get a new credit card number. Your account number, on the other hand, will remain the same.

Credit Card Number Tips

Although a credit card is a piece of plastic, the numbers embossed on it are sensitive financial details and should be carefully guarded. Here are some tips for keeping them secure.

Never Store Your Credit Card Number, Expiration Date, and CVV in One Place

While each of these numbers on their own contain important details, in combination they give a malicious user everything they need to successfully process a transaction. Without also being able to enter the correct expiry date and CVV, they may not be able to complete their transaction.

Keep an Eye on Expiry Dates

While banks typically send out a new card in advance of the expiry date, there may be instances where a cardholder doesn’t receive their new card in time — and that can be stressful for anyone who relies on a credit card for everyday purchases. Keeping an eye on your credit card’s expiry date is a good way to avoid being caught without a working credit card.

The Takeaway

From choosing a credit card to understanding what all the numbers on the front and back of the card mean, feeling comfortable paying with plastic can take some legwork. Depending on which credit card you get, your credit card numbers will vary.

This article originally appeared on SoFi.comand was syndicated by MediaFeed.org.

Lantern By

SoFiSoFi receives compensation in the event you obtain a loan, financial product, or service through the Lantern marketplace. This Lantern website is owned by SoFi Lending Corp., a lender licensed by the Department of Financial Protection and Innovation under the California Financing Law, license number 6054612; NMLS number 1121636. (www.nmlsconsumeraccess.org). This site is NOT owned and operated by SoFi Bank. Loans, financial products, and services may not be available in all states.

All rates, fees, and terms are presented without guarantee and are subject to change pursuant to each provider’s discretion. There is no guarantee you will be approved or qualify for the advertised rates, fees, or terms presented. The actual terms you may receive depends on the things like benefits requested, your credit score, usage, history and other factors.

*Check your rate: To check the rates and terms you may qualify for, Lantern and/or its network lenders conducts a soft credit pull that will not affect your credit score. However, if you choose a product and continue your application, the lender(s) you choose will request your full credit report from one or more consumer reporting agencies, which is considered a hard credit pull and may affect your credit.

All loan terms, including interest rate, and Annual Percentage Rate (APR), and monthly payments shown on this website are from lenders and are estimates based upon the limited information you provided and are for information purposes only. Estimated APR includes all applicable fees as required under the Truth in Lending Act. The actual loan terms you receive, including APR, will depend on the lender you select, their underwriting criteria, and your personal financial factors. The loan terms and rates presented are provided by the lenders and not by SoFi Lending Corp. or Lantern. Please review each lender’s Terms and Conditions for additional details.

Many factors affect your credit scores and the interest rates you may receive. SoFi is not a Credit Repair Organization as defined under federal or state law, including the Credit Repair Organizations Act. SoFi does not provide “credit repair” services or advice or assistance regarding “rebuilding” or “improving” your credit record, credit history, or credit rating. For details, see the FTC’s website on credit (consumer.ftc.gov)

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.¹

SoFi’s Insights tool offers users the ability to connect both SoFi accounts and external accounts using Plaid, Inc.’s service. When you use the service to connect an account, you authorize SoFi to obtain account information from any external accounts as set forth in SoFi’s Terms of Use. SoFi assumes no responsibility for the timeliness, accuracy, deletion, non-delivery or failure to store any user data, loss of user data, communications, or personalization settings. You shall confirm the accuracy of Plaid data through sources independent of SoFi. The credit score provided to you is a VantageScore® based on TransUnion® (the “Processing Agent”) data.

Personal Loan

SoFi Lending Corp. (“SoFi”) operates this Personal Loan product in cooperation with Engine by MoneyLion. If you submit a loan inquiry, SoFi will deliver your information to Engine by MoneyLion, and Engine by MoneyLion will deliver to its network of lenders/partners to review to determine if you are eligible for pre-qualified or pre-approved offers. The lenders/partners receiving your information will also obtain your credit information from a credit reporting agency. If you meet one or more lender’s and/or partner’s conditions for eligibility, pre-qualified and pre-approved offers from one or more lenders/partners will be presented to you here on the Lantern website. More information about Engine by MoneyLion, the process, and its lenders/partners is described on the loan inquiry form you will reach by visiting our Personal Loans page as well as our Student Loan Refinance page. Click to learn more about Engine’s Licenses and Disclosures, Terms of Service, and Privacy Policy.Personal loan offers provided to customers on Lantern do not exceed 35.99% APR. An example of total amount paid on a personal loan of $10,000 for a term of 36 months at a rate of 10% would be equivalent to $11,616.12 over the 36 month life of the loan.

Student Loan RefinanceSoFi Lending Corp. (“SoFi”) operates this Student Loan Refinance product in cooperation with Engine by MoneyLion. If you submit a loan inquiry, SoFi will deliver your information to Engine by MoneyLion, and Engine by MoneyLion will deliver to its network of lenders/partners to review to determine if you are eligible for pre-qualified or pre-approved offers. The lenders receiving your information will also obtain your credit information from a credit reporting agency. If you meet one or more lender’s and/or partner’s conditions for eligibility, pre-qualified and pre-approved offers from one or more lenders/partners will be presented to you here on the Lantern website. More information about Engine by MoneyLion, the process, and its lenders/partners is described on the loan inquiry form you will reach by visiting our Personal Loans page as well as our Student Loan Refinance page. Click to learn more about Engine’s Licenses and Disclosures, Terms of Service, and Privacy Policy.

NOTICE: The debt ceiling legislation passed on June 2, 2023, codifies into law that federal student loan borrowers will be reentering repayment. The US Department of Education or your student loan servicer, or lender if you have FFEL loans, will notify you directly when your payments will resume For more information, please go to https://docs.house.gov/billsthisweek/20230529/BILLS-118hrPIH-fiscalresponsibility.pdf https://studentaid.gov/announcements-events/covid-19

If you are a federal student loan borrower considering refinancing, you should take into account the new income-driven payment plan, SAVE, which replaces REPAYE, seeks to make monthly payments more affordable, and offers forgiveness of balances that were originally $12,000 or lower after 120 payments, among other improvements. Also, please note that once you refinance federal student loans you will no longer be eligible for current or future flexible payment options available to federal loan borrowers, including but not limited to income-based repayment plans, such as SAVE, or extended repayment plans.

Auto Loan RefinanceAutomobile refinancing loan information presented on this Lantern website is from Caribou, AUTOPAY, Engine by MoneyLion, and each of Engine’s partners (along with their affiliated companies). Caribou, AUTOPAY, and Engine by MoneyLion pay SoFi compensation for marketing their products and services on the Lantern site.

Auto loan refinance information presented on this Lantern site is indicative and subject to you fulfilling the lender’s requirements, including but not limited to: credit standards, loan size, vehicle condition, and odometer reading. Loan rates and terms as presented on this Lantern site are subject to change when you reach the lender and may depend on your creditworthiness, consult with the lender for more details. Additional terms and conditions may apply and all terms may vary by your state of residence.

Secured Lending DisclosureTerms, conditions, state restrictions, and minimum loan amounts apply. Before you apply for a secured loan, we encourage you to carefully consider whether this loan type is the right choice for you. If you can’t make your payments on a secured personal loan, you could end up losing the assets you provided for collateral. Not all applicants will qualify for larger loan amounts or most favorable loan terms. Loan approval and actual loan terms depend on the ability to meet underwriting requirements (including, but not limited to, a responsible credit history, sufficient income after monthly expenses, and availability of collateral) that will vary by lender.

BankingSoFi Lending Corp. (“SoFi”) operates this website in cooperation with Engine by MoneyLion presenting promotions for products and services offered by other banks, lenders, and financial institutions. If you select a promotion above, you will be connected to the website of the company offering the product. The promotions presented on this site are from companies that pay SoFi and Engine by MoneyLion compensation for marketing their products and services. This may affect whether a provider is featured on this site and could affect the order of presentation. Lantern and Engine by MoneyLion do not include all providers in the market or all of their available offerings. Click to learn more about Engine’s Licenses and Disclosures, Terms of Service, and Privacy Policy.

More from MediaFeed:

How to protect your money after you die

Not all wills are alike; there are actually four main kinds and one of them is right for you. Sure, writing a will can be an easy task to put off until “someday.”

But what if the worst were to happen before “someday?” That could mean a complicated and emotionally draining legal process for your loved ones. Creating a will not only can provide peace of mind for your loved ones after you die, but it can also provide peace of mind for you right now.

Studio Firma

The simple definition of a will is a document that states your final wishes. This alone was sufficient a century ago, when many people had limited property to pass down. But in the modern era, when “property” encompasses everything from the contents of your long-forgotten storage unit to the crypto you decided to buy on a whim, a simple will may not encompass your complex life.

Not only that, but a will is a document that only takes effect after you die. But what if you were medically unable to make decisions? Modern end-of-life documents encompass your wishes if you were medically or otherwise unable to make decisions on your own. Among these documents is one that also has the world “will” in its name.

ebstock / istockphoto

As you begin estate planning, you’ll likely come across four common types of wills. These are:

- A simple will

- A joint will

- A testamentary trust will

- A living will

Let’s look at each type of will more closely.

DepositPhotos.com

Like the name, a simple will may be the type of will that pops into your mind when you hear the word “will.” This will can:

- State how you want your property bequeathed upon death

- Provide guardianship specifications for minors

Upon death, a simple will is likely to go through a legal process known as probate to divide assets. Sometimes, in the case of high-net worth individuals, probate can be expensive. (For those with complex situations and a positive net worth, a trust can help handle those what-ifs. It can transfer assets out of your estate and into the trust, which can be advantageous in terms of taxes.)

But in many situations, a simple will can provide peace of mind for people in good health. Later, these individuals may want to take on more complex estate planning, but a will provides a good foundation when it comes to making sure guardians are named and property is divided according to your wishes.

A simple will can be created through online templates, and the cost can be zero dollars to several hundred dollars. More expensive online options may come with support from an attorney who can help answer simple questions. Once created, a will then needs to be made legal according to state laws. This may include signing the will in front of witnesses. You may also want to have it notarized. Having a hard copy of the will, as well as people who know how to access it in case of your death, can ensure the will is found in a timely manner if you were to die.

DepositPhotos.com

A joint functions in much the same way as a simple will, except it is a will created by two people, usually who are married to each other. It merges their wishes into a single legal document. In many cases, this kind of will dictates that property will be left entirely to the surviving partner. Here’s the catch, though: Upon death, property will be distributed in the manner dictated by the will — the surviving person does not have the ability or authority to make changes to what the will says once the initial spouse has died.

This can sound streamlined, especially if couples were planning to leave everything to each other anyway. But this type of will can cause headaches. For example, if the surviving spouse has more children or gets remarried, it can be almost impossible to provide for additional people not named in the initial, joint will. There could be problems even if the surviving spouse does not remarry. For example, if the marital home is considered an asset to be given to the couple’s children upon the death of both of the will’s creators, it may be impossible for the surviving spouse to sell a home to downsize.

One alternative that may suit married couples is to create two individual wills. This may provide a greater degree of flexibility and better achieve the desired effect without ruling out all of life’s what-ifs.

Serenethos / istockphoto

A testamentary trust will is usually part of big-picture estate planning. It is a document that creates a trust that goes into effect when you die. This trust can outline how certain types of property will be divided. A testamentary trust can have certain stipulations (for example, someone only inherits X piece of property when they reach Y age). This can also be used for people with minors or dependents to help ensure that wishes are followed.

What’s more, a testamentary trust can also help provide for pets. Because a pet can’t own property, naming your “fur baby” within a will can set up a legal headache. But a testamentary trust can ensure that your pet will be provided for according to your wishes.

It’s worth noting that a testamentary trust will go through the probate process, and it may not have the same tax benefits for recipients as other types of trusts. Weighing the pros and cons of different trust options can be helpful before settling on the best one for your situation.

fizkes/istockphoto

This is a hard topic to think about, but what if you were in an accident and were knocked unconscious? What if you were undergoing treatment for a serious medical condition and couldn’t fully grasp the options offered to you? There’s a way to put a trusted relative or friend in the decision-making role.

A living will, which is also known as an advance directive, specifies your wishes if you were medically incapacitated or unable to make or communicate decisions about your medical care. It also stipulates who your healthcare proxy, also known as a medical power of attorney, would be to make medical decisions on your behalf.

If you are creating a living, you may also want to create a power of attorney document as well. This designates a person, who may or may not be the same person as your healthcare proxy, who has the right to make financial decisions on your behalf. Having a living will can cover unexpected situations that may occur before death and can be an integral part of end-of-life planning.

twinsterphoto / iStock

While end of life planning can be a challenging or sad endeavor, it’s an important step in making sure your assets are directed where you want them to go and that other important wishes are executed as you want. There are four main types of wills to help you legally record your plans. You’ll have options; more than one may suit your needs.

And you can decide to use online services or work in person with an attorney. In either case, having the appropriate forms completed will give you peace of mind right now — and help smooth things along for your loved ones in the future during a difficult time.

Learn More:

This article originally appeared on SoFi.com and was syndicated by MediaFeed.org.

Ladder policies are issued in New York by Allianz Life Insurance Company of New York, New York, NY (Policy form # MN-26) and in all other states and DC by Allianz Life Insurance Company of North America, Minneapolis, MN (Policy form # ICC20P-AZ100 and # P-AZ100). Only Allianz Life Insurance Company of New York is authorized to offer life insurance in the state of New York. Coverage and pricing is subject to eligibility and underwriting criteria. SoFi Agency and its affiliates do not guarantee the services of any insurance company. The California license number for SoFi Agency is 0L13077 and for Ladder is OK22568. Ladder, SoFi and SoFi Agency are separate, independent entities and are not responsible for the financial condition, business, or legal obligations of the other. Social Finance, Inc. (SoFi) and Social Finance Life Insurance Agency, LLC (SoFi Agency) do not issue, underwrite insurance or pay claims under LadderLife policies. SoFi is compensated by Ladder for each issued term life policy. SoFi offers customers the opportunity to reach Ladder Insurance Services, LLC to obtain information about estate planning documents such as wills. Social Finance, Inc. (“SoFi”) will be paid a marketing fee by Ladder when customers make a purchase through this link. All services from Ladder Insurance Services, LLC are their own. Once you reach Ladder, SoFi is not involved and has no control over the products or services involved. The Ladder service is limited to documents and does not provide legal advice. Individual circumstances are unique and using documents provided is not a substitute for obtaining legal advice.

This article is not intended to be legal advice. Please consult an attorney for advice.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

SoFi offers customers the opportunity to reach the following Insurance Agents:

Home & Renters: Lemonade Insurance Agency (LIA) is acting as the agent of Lemonade Insurance Company in selling this insurance policy, in which it receives compensation based on the premiums for the insurance policies it sells.

Insurance not available in all states.

Gabi is a registered service mark of Gabi Personal Insurance Agency, Inc.

SoFi is compensated by Gabi for each customer who completes an application through the SoFi-Gabi partnership.

nortonrsx/ istockphoto

DepositPhotos.com

Featured Image Credit: fizkes/istockphoto.