Native Americans are the most likely group to be unbanked in the U.S., according to a Federal Deposit Insurance Corporation (FDIC) survey, and many lack access to banking services and ATMs. Native American-owned banks and credit unions help address this issue by providing financial services to Native American communities.

While anyone can bank with a Native American bank or credit union, these institutions aim to serve and empower Native American individuals. To qualify as a Native American bank or credit union, these institutions must either be majority-owned by Native Americans or have a board of directors that’s majority Native American.

What Is a Native American Bank or Credit Union?

A Native American bank or credit union is a type of minority depository institution (MDI) that’s majority-owned by Native Americans or has a board of directors that’s majority Native American. These banks and credit unions also primarily serve Native American communities and seek to provide their customers with affordable and accessible banking services and products.

As MDIs, Native American banks receive assistance from the government to operate, particularly technical and management assistance. Banks are for-profit institutions, whereas credit unions are member-owned organizations.

Why These Institutions Are Important

Native American-owned banks help equip American Indian and Alaska Native communities with financial education and empowerment. As mentioned, Native Americans are the most likely group to be unbanked, meaning it’s difficult for many people and businesses to access checking and savings accounts, loans, mortgages, credit cards, and other financial services. Online banking isn’t necessarily a solution, since not all tribal residents have access to broadband.

Lack of access to banking also impacts people’s credit scores. A poor or nonexistent credit score makes it even harder to access affordable loans. Native American banks and credit unions can help combat these problems and connect people with affordable products and the opportunity to build their creditworthiness.

Minority Depository Institutions (MDIs)

Native American-owned banks and credit unions are a type of MDI, which are institutions that are majority-owned or governed by people of color. MDIs came into being with the Financial Institutions Reform, Recovery, and Enforcement Act of 1989.

To be designated as an MDI, the bank must have more than half of its voting stock owned by minority individuals (Black, Native American, Hispanic American, or Asian American individuals). Alternatively, it must have a Board of Directors where the majority of people are minority individuals and predominantly serve minority communities.

Federally designated MDIs receive government assistance, such as technical, training, and education programs, and preservation of minority ownership in the case of a merger or acquisition.

Community Development Financial Institutions (CDFIs)

Similar to MDIs, community development financial institutions (CDFIs) have a mission to support economically disenfranchised communities. They support community development by providing financial services, loans, investments, training programs, minority-owned businesses, and other development efforts.

Along with providing banking services to underserved communities, CDFIs often run microloan programs to help small business owners launch and grow businesses. They may also provide small business grants for minorities or fund affordable housing and community facilities.

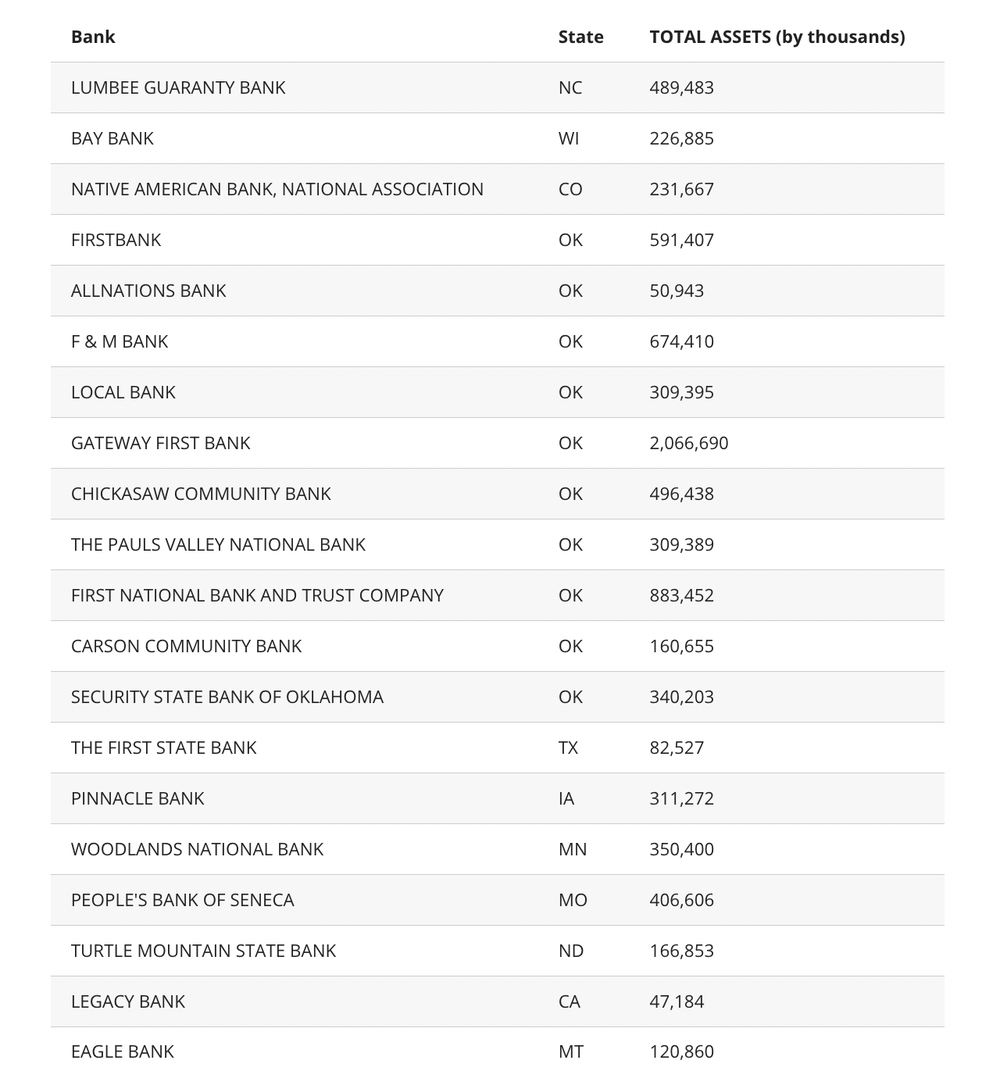

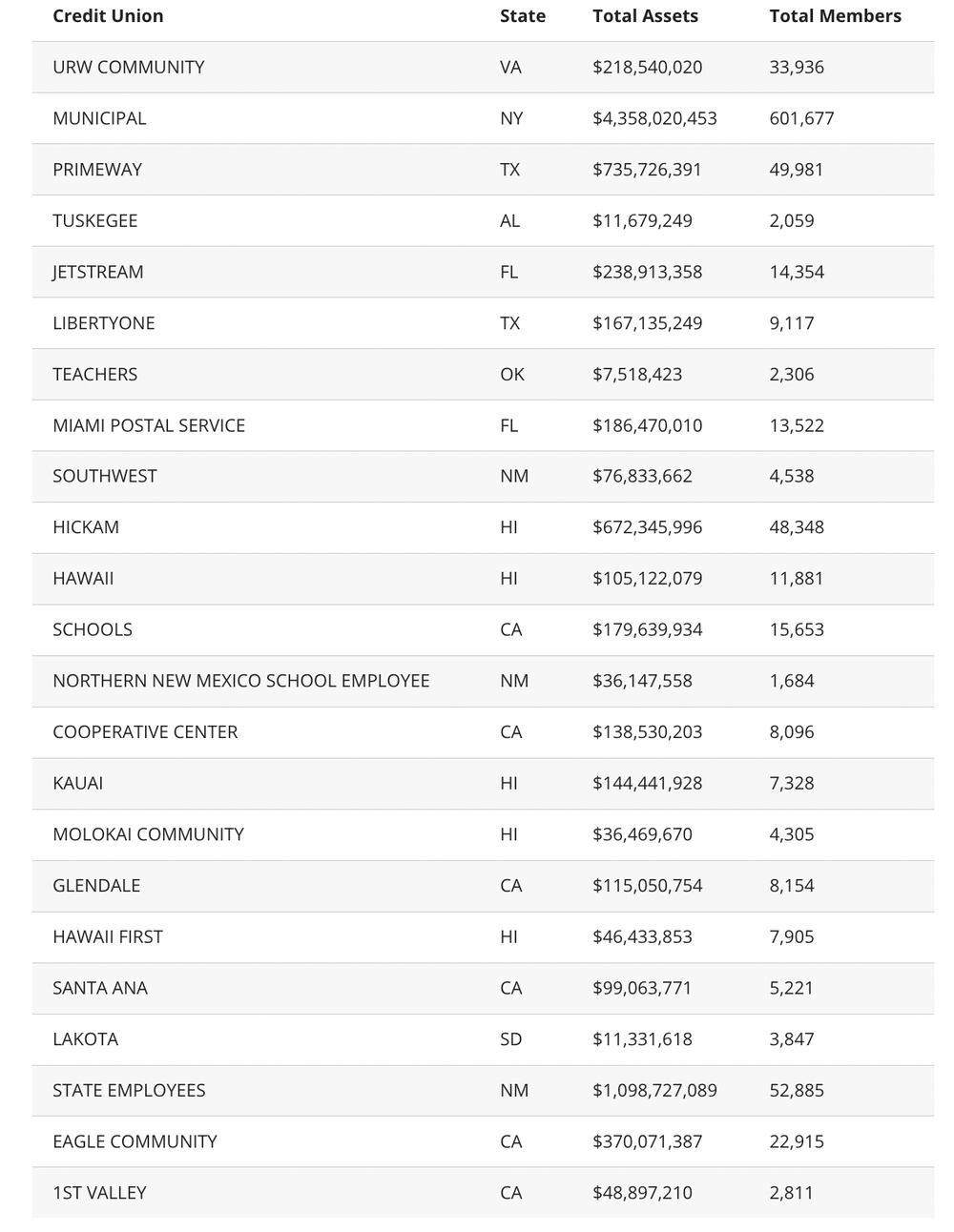

Active Native American-owned Banks and Credit Unions

The FDIC maintains a list of Minority Depository Institutions. Here are some of the active banks that are Native American or Alaskan Native American owned.

The National Credit Union Administration (NCUA) maintains a list of credit union MDIs. Here are some of the Native American credit unions active today, including their state, total, assets, and total members.

(Learn more: Personal Loan Calculator)

Supporting Your Local Financial Institutions

Anyone can bank with a Native American-owned bank or other MDI. These institutions are committed to supporting communities that have historically been excluded from mainstream banking services.

By banking with an MDI, you can help support its mission and community. Keep in mind, though, the differences between banks vs. credit unions. While almost anyone can open an account with a bank, credit unions have specific membership requirements. You might need to live in a certain area or work for an eligible employer to join.

The Takeaway

Native American-owned banks and credit unions serve traditionally underbanked communities and help equip people with financial self-sufficiency. While these banks primarily serve indigenous communities, anyone can join these or other minority-serving institutions to support their mission.

This article originally appeared on SoFi.com and was syndicated by MediaFeed.org.

Lantern By

SoFiSoFi receives compensation in the event you obtain a loan, financial product, or service through the Lantern marketplace. This Lantern website is owned by SoFi Lending Corp., a lender licensed by the Department of Financial Protection and Innovation under the California Financing Law, license number 6054612; NMLS number 1121636. (nmlsconsumeraccess). This site is NOT owned and operated by SoFi Bank. Loans, financial products, and services may not be available in all states.

All rates, fees, and terms are presented without guarantee and are subject to change pursuant to each provider’s discretion. There is no guarantee you will be approved or qualify for the advertised rates, fees, or terms presented. The actual terms you may receive depends on the things like benefits requested, your credit score, usage, history and other factors.

*Check your rate: To check the rates and terms you may qualify for, Lantern and/or its network lenders conducts a soft credit pull that will not affect your credit score. However, if you choose a product and continue your application, the lender(s) you choose will request your full credit report from one or more consumer reporting agencies, which is considered a hard credit pull and may affect your credit.

All loan terms, including interest rate, and Annual Percentage Rate (APR), and monthly payments shown on this website are from lenders and are estimates based upon the limited information you provided and are for information purposes only. Estimated APR includes all applicable fees as required under the Truth in Lending Act. The actual loan terms you receive, including APR, will depend on the lender you select, their underwriting criteria, and your personal financial factors. The loan terms and rates presented are provided by the lenders and not by SoFi Lending Corp. or Lantern. Please review each lender’s Terms and Conditions for additional details.

Many factors affect your credit scores and the interest rates you may receive. SoFi is not a Credit Repair Organization as defined under federal or state law, including the Credit Repair Organizations Act. SoFi does not provide “credit repair” services or advice or assistance regarding “rebuilding” or “improving” your credit record, credit history, or credit rating. For details, see the FTC’s website on credit (consumer.ftc.gov)

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.¹

SoFi’s Insights tool offers users the ability to connect both SoFi accounts and external accounts using Plaid, Inc.’s service. When you use the service to connect an account, you authorize SoFi to obtain account information from any external accounts as set forth in SoFi’s Terms of Use. SoFi assumes no responsibility for the timeliness, accuracy, deletion, non-delivery or failure to store any user data, loss of user data, communications, or personalization settings. You shall confirm the accuracy of Plaid data through sources independent of SoFi. The credit score provided to you is a VantageScore® based on TransUnion® (the “Processing Agent”) data.

Personal Loan

SoFi Lending Corp. (“SoFi”) operates this Personal Loan product in cooperation with Engine by MoneyLion. If you submit a loan inquiry, SoFi will deliver your information to Engine by MoneyLion, and Engine by MoneyLion will deliver to its network of lenders/partners to review to determine if you are eligible for pre-qualified or pre-approved offers. The lenders/partners receiving your information will also obtain your credit information from a credit reporting agency. If you meet one or more lender’s and/or partner’s conditions for eligibility, pre-qualified and pre-approved offers from one or more lenders/partners will be presented to you here on the Lantern website. More information about Engine by MoneyLion, the process, and its lenders/partners is described on the loan inquiry form you will reach by visiting our Personal Loans page as well as our Student Loan Refinance page. Click to learn more about Engine’s Licenses and Disclosures, Terms of Service, and Privacy Policy.Personal loan offers provided to customers on Lantern do not exceed 35.99% APR. An example of total amount paid on a personal loan of $10,000 for a term of 36 months at a rate of 10% would be equivalent to $11,616.12 over the 36 month life of the loan.

Student Loan RefinanceSoFi Lending Corp. (“SoFi”) operates this Student Loan Refinance product in cooperation with Engine by MoneyLion. If you submit a loan inquiry, SoFi will deliver your information to Engine by MoneyLion, and Engine by MoneyLion will deliver to its network of lenders/partners to review to determine if you are eligible for pre-qualified or pre-approved offers. The lenders receiving your information will also obtain your credit information from a credit reporting agency. If you meet one or more lender’s and/or partner’s conditions for eligibility, pre-qualified and pre-approved offers from one or more lenders/partners will be presented to you here on the Lantern website. More information about Engine by MoneyLion, the process, and its lenders/partners is described on the loan inquiry form you will reach by visiting our Personal Loans page as well as our Student Loan Refinance page. Click to learn more about Engine’s Licenses and Disclosures, Terms of Service, and Privacy Policy.

NOTICE: The debt ceiling legislation passed on June 2, 2023, codifies into law that federal student loan borrowers will be reentering repayment. The US Department of Education or your student loan servicer, or lender if you have FFEL loans, will notify you directly when your payments will resume For more information, please go to https://docs.house.gov/billsthisweek/20230529/BILLS-118hrPIH-fiscalresponsibility.pdf https://studentaid.gov/announcements-events/covid-19

If you are a federal student loan borrower considering refinancing, you should take into account the new income-driven payment plan, SAVE, which replaces REPAYE, seeks to make monthly payments more affordable, and offers forgiveness of balances that were originally $12,000 or lower after 120 payments, among other improvements. Also, please note that once you refinance federal student loans you will no longer be eligible for current or future flexible payment options available to federal loan borrowers, including but not limited to income-based repayment plans, such as SAVE, or extended repayment plans.

Auto Loan RefinanceAutomobile refinancing loan information presented on this Lantern website is from Caribou, AUTOPAY, Engine by MoneyLion, and each of Engine’s partners (along with their affiliated companies). Caribou, AUTOPAY, and Engine by MoneyLion pay SoFi compensation for marketing their products and services on the Lantern site.

Auto loan refinance information presented on this Lantern site is indicative and subject to you fulfilling the lender’s requirements, including but not limited to: credit standards, loan size, vehicle condition, and odometer reading. Loan rates and terms as presented on this Lantern site are subject to change when you reach the lender and may depend on your creditworthiness, consult with the lender for more details. Additional terms and conditions may apply and all terms may vary by your state of residence.

Secured Lending DisclosureTerms, conditions, state restrictions, and minimum loan amounts apply. Before you apply for a secured loan, we encourage you to carefully consider whether this loan type is the right choice for you. If you can’t make your payments on a secured personal loan, you could end up losing the assets you provided for collateral. Not all applicants will qualify for larger loan amounts or most favorable loan terms. Loan approval and actual loan terms depend on the ability to meet underwriting requirements (including, but not limited to, a responsible credit history, sufficient income after monthly expenses, and availability of collateral) that will vary by lender.

BankingSoFi Lending Corp. (“SoFi”) operates this website in cooperation with Engine by MoneyLion presenting promotions for products and services offered by other banks, lenders, and financial institutions. If you select a promotion above, you will be connected to the website of the company offering the product. The promotions presented on this site are from companies that pay SoFi and Engine by MoneyLion compensation for marketing their products and services. This may affect whether a provider is featured on this site and could affect the order of presentation. Lantern and Engine by MoneyLion do not include all providers in the market or all of their available offerings. Click to learn more about Engine’s Licenses and Disclosures, Terms of Service, and Privacy Policy.

More from MediaFeed:

7 brilliant ways to avoid high bank fees

Have you ever heard the old saying, “Penny wise and pound foolish”?

It’s a little knock at folks who tend to be frugal about small expenditures but not so cautious when they’re buying the big stuff. (The person who uses coupons to purchase toilet paper, for example, but doesn’t negotiate a better price for an expensive new car.)

We all like to think we’re using our money efficiently, but it can be easy to miss out on chances to save. That’s especially true when costs are automatic and virtually invisible (or, at least buried in the fine print), like the maintenance fees some banks charge for their checking accounts.

Customers tend to think of them as the price of doing business. After all, it can be tough to function in today’s world without some kind of cash management account where you can deposit, hold and withdraw money.

But those fees can eat away at the money you’ve worked hard to earn. And according to the most recent Moneyrates.com survey, monthly maintenance fees continue to rise, and now add up to an average $162.96 per year.

The good news is there are ways to avoid account maintenance fees without going back to the good old days of shoving money under the mattress. This list is in no way comprehensive of all the options out there, but here are a few possible ways to avoid potential fees.

Related: Comparing the different types of deposit accounts

This article originally appeared on SoFi.com and was syndicated by MediaFeed.org.

DepositPhotos.com

Because online financial institutions don’t have brick-and-mortar branches, tellers or other overhead costs, they tend to pass those savings on to their customers. That typically means better interest rates for savings, but also low or no fees on account balances.

DepositPhotos.com

If you aren’t ready for online banking — or you want to keep at least some money in a traditional financial institution — there are still ways to possibly duck that monthly maintenance charge.

Fees and rules vary from bank to bank, and from account type to account type, but generally you can avoid the cost if you keep your balance over a certain threshold. If your balance drops below that amount, your bank statement will show you were charged for the month.

Banks measure and enforce the minimum balance in different ways, and there can be more than one minimum balance for the same account. (One amount might be required to keep an account open, for instance, while a higher balance could be required to qualify for fee waivers or interest payments on deposits.)

So be sure you understand the requirements for your specific type of account. You can usually find that information on the financial institution’s website, but if you can’t, call customer service for a jargon-free rundown. And you could also ask that you receive an email or text if your balance drops below the minimum.

DepositPhotos.com

Banks may waive the maintenance charge for those who have funds electronically transferred into an account.

You can check your bank’s website to see if this is their policy. It may be possible to have paychecks, tax refund, Social Security checks and other payments delivered this way.

There may be a monthly minimum set for this amount, as well, so ask about that — and how the minimum applies if you split the direct deposit among two or more accounts.

AndreyPopov / Getty

If your bank is looking for a total customer relationship, it may offer free services for those who use more than one of their services (such as a savings account, certificate of deposit, or IRA).

Just be sure to do some research and crunch the numbers before you put all your money in one place. Another institution may have a better rate on CDs, or offer better investment services, etc.

DepositPhotos.com

You may qualify for a lower fee (or no fee) if you’re a veteran, a senior, disabled, or a student. It can’t hurt to ask — and be prepared to show some paperwork. You also might be able to get a discount if you ask your bank to stop sending you monthly statements in the mail.

The incentives for going paperless aren’t always about money — and your bank may try to convince you that it’s more about cutting clutter and saving the planet. But paperless is a source of savings for them, and it might mean savings for you, too.

LSOphoto / istockphoto

Maybe you chose your bank years ago based on location, reputation, or a friend’s recommendation. But if you’re paying for services that are free elsewhere, it might be time to consider a breakup.

Before you go, you may want to talk to someone in charge about why you’re leaving, and see if you can negotiate terms you feel better about. If that isn’t possible, take the time to research your next move.

Will you be comfortable with a change? You could check out what other customers are saying in online reviews, and look at the website to be sure there aren’t any surprise fees with your new account. Consider whether online banking is a fit for you as you go forward.

PeopleImages

If you aren’t sure what kind of fees you’re paying month to month, you might want to start taking a closer look at your statements. You may find you’re being incorrectly charged — or that you’re making mistakes yourself that are costing you more money than you’re saving.

Learn more:

External Websites: The information and analysis provided through hyperlinks to third party websites, while believed to be accurate, cannot be guaranteed by SoFi. Links are provided for informational purposes and should not be viewed as an endorsement.

SoFi Money

SoFi Money is a cash management account, which is a brokerage product, offered by SoFi Securities LLC, member FINRA/SIPC. Neither SoFi nor its affiliates is a bank.

DepositPhotos.com

Featured Image Credit: Fly View Productions/istockphoto.