Nightmare on Rate Street

It’s been hard to escape the headlines about mortgage rates hitting 8%, and even harder to escape conversations about the housing market, regardless of whether or not you’re actively looking to buy or sell.

Like with most datasets, there are positive and negative ways to interpret the current housing indicators. This post will focus on some recent moves that signal caution, but there remain occasional bright spots, including the fact that the housing market has not (yet) crashed, despite many warnings that it would.

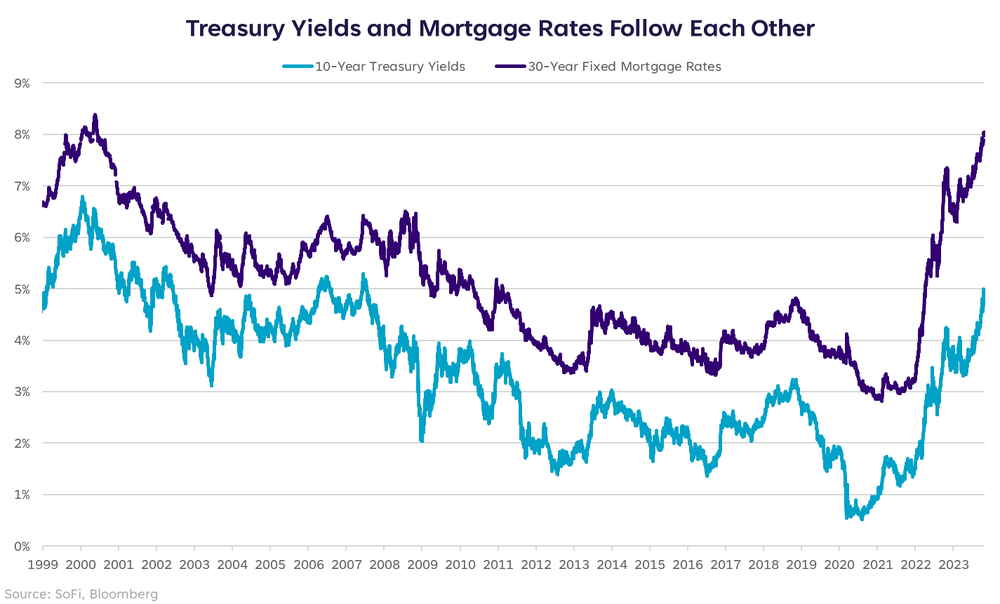

The chart below illustrates the relationship between 10-year U.S. Treasury yields and 30-year fixed mortgage rates. Given the sharp rise in yields over the last few months, it’s no surprise that mortgage rates followed a similar trend. What’s interesting is how large the spread has become between the two.

Most people don’t try to offset their mortgage rates with 10-yr Treasury yields, but the premium a consumer has to pay above the so-called “risk-free” rate is considerably higher than usual right now. No matter which way you slice and dice it, this is constricting capital, and cooling activity in the residential housing sector.

Although mortgage rates are lower than the astronomical levels of the 1980s (when they hit a high of 18.6% in October 1981), an 8% mortgage is the highest level consumers have seen in over 23 years.

Rocky Housing Picture Show

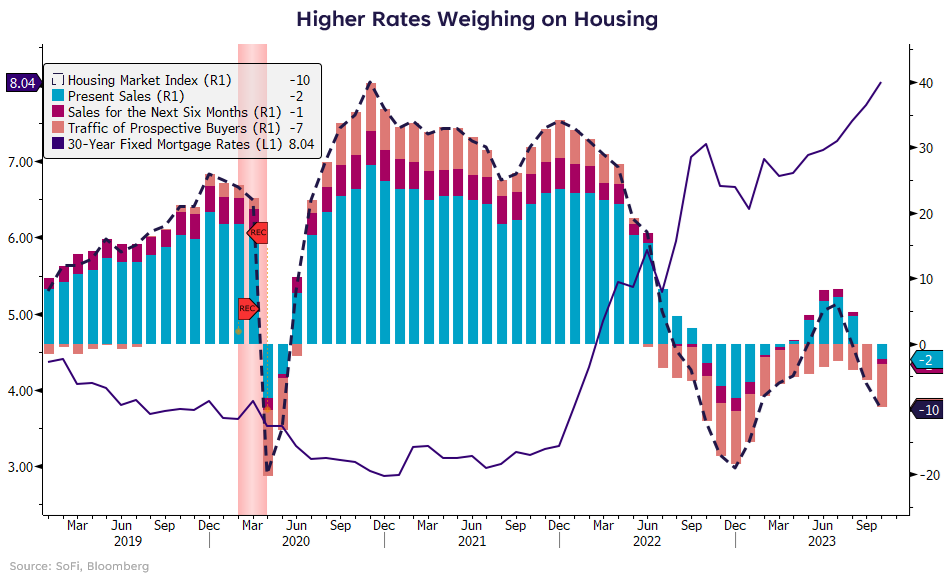

Mortgage rates are the obvious indicator, but it’s important to know what some of the tangible activity metrics are telling us in response to more expensive financing.

As mortgage rates rose, the data clearly showed a slowdown in current sales, future expected sales, and even traffic of prospective buyers. There was a brief revival of activity in June and July of this year — which, in my opinion, was the result of strong seasonal factors, falling inflation readings, and the stock market rising through the end of July, giving consumers good “feels” about spending.

Since then, the trend has returned to a downward slope, with the traffic of prospective buyers having remained negative since mid-2022. Activity and appetite for home buying have clearly taken a hit as a result of the higher cost of borrowing.

Night of the Living Supply

If you happen to be one of the consumers looking to buy or sell a home, you may be wondering how all of this can be true, while home prices are still historically high.

The operative word that I think will go down as defining this economic cycle is “lags”. Home prices take a while to respond to activity data, especially during a time when existing homes aren’t changing hands as frequently because no one wants to give up their sub-4% mortgage rate. It’s hard to mark-to-market if the market doesn’t have enough activity.

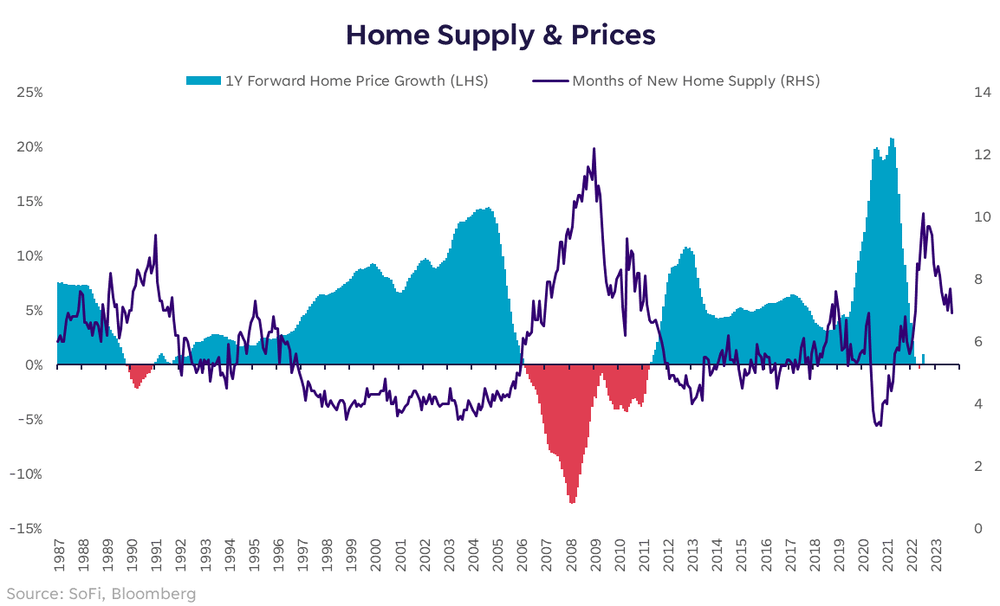

One of the indicators that leads home prices is new home supply, and home prices lag this data by about one year. In other words, as new home supply increases, home prices should fall — but not until roughly one year later. Likewise, as supply falls, home prices should increase.

One confusing element here is that the supply line has been a little jumpy. Supply decisively increased between late 2020 and mid-2022, but has fallen since — likely keeping prices supported. If rates stay elevated, supply may pile up, putting pressure on prices as time rolls on.

The other confusing element is that this chart shows home price growth near 0%, leading us to believe that prices have come down. But they haven’t, they’ve just stopped rising as quickly. Since December 2019, national home prices have increased more than 43% (latest data available is July 2023).

Despite an occasional bright spot in housing data, there are mounting concerns and indicators otherwise. Housing is one of the most important cyclical indicators for our economy, and is strongly correlated to the health of the consumer and their appetite to spend. It’s been a confounding element for many economists and analysts as it displayed seemingly unyielding strength in the face of tightening, but a tone shift may be afoot.

This article originally appeared on SoFi.com and was syndicated by MediaFeed.org.

Communication of SoFi Wealth LLC an SEC Registered Investment Adviser. Information about SoFi Wealth’s advisory operations, services, and fees is set forth in SoFi Wealth’s current Form ADV Part 2 (Brochure), a copy of which is available upon request and at adviserinfo.sec. Liz Young is a Registered Representative of SoFi Securities and Investment Advisor Representative of SoFi Wealth. Her ADV 2B is available at sofi.

More from MediaFeed

5 home loans that may include home renovation costs

Did you know you can use a home loan for renovations? Renovation home loans cover the cost of purchasing and renovating a home. If you’re familiar with construction loans, renovation loans are similar. Also called “one-close” loans or renovation mortgages, renovation loans can offer buyers simplified financing for transforming a fixer-upper into an attractive, modernized home.

A renovation home loan combines the cost of a home purchase and money for renovations in one mortgage. There’s only one closing and one loan when buying a new home or refinancing an existing home. The lender has oversight of the renovation funds, including the budget, vetting of the contractor, and disbursement of funds for renovation work as it is completed.

The borrower, their property, and their lender must all meet criteria set out by the remodel home loan program to qualify, which can present a challenge. Qualifying lenders in particular can be hard to find. That’s because most lenders must maintain a custodial account for the renovations over the course of an entire year, which requires extra work and resources. However, if you can find a lender that can handle the process, renovation loans can be a convenient way to improve a promising fixer-upper.

Hispanolistic/istockphoto

Most mortgages will not include renovations in the loan amount. Renovation mortgages are niche products serviced by a fraction of lenders. Buyers and properties must also meet certain requirements, which we’ll outline below.

There are several different types of home loans you can apply for that are eligible for adding renovation costs to the mortgage.

skynesher/istockphoto

An FHA 203(k) is a mortgage serviced by the Federal Housing Authority in which the cost of repairs is combined with the mortgage amount. It’s different from a traditional FHA loan that does not include improvement expenses, but qualifications (credit score, down payment, etc.) are very similar.

Interest rates and terms are also similar to what you see in a standard FHA loan. However, you can expect additional lender fees to cover the extra oversight needed on a renovation loan.

The amount you can borrow is equal to either the value of the property plus the cost of renovations or 110% of the projected value of the property after rehabilitation. Borrowers must use an FHA-approved lender for this type of mortgage.

Eligible properties must be one to four units. Repairs can include those that enhance the property’s appearance and function, the elimination of health and safety hazards, landscape work, roofing, accessibility improvements, energy conservation, and more. A limited 203(k) is also available for repairs costing $35,000 or less.

Andrii Dodonov/istockphoto

The Homestyle Renovation loan from Fannie Mae takes into account the value of the property after renovations are complete. The amount of allowable renovation money can equal 75% of the value of the property after renovations are complete.

In the world of home loans, the loan-to-value ratio (LTV) is the percentage of your home’s value that is borrowed. Many lenders limit your LTV to 80% to 85%.

A HomeStyle loan allows an LTV of up to 97%. This means it’s possible to put as little as 3% down. Some investment properties are also eligible for this type of loan. Renovations are eligible as long as they are permanently affixed to the property. Work must be completed within 15 months from the closing date of the loan.

Feverpitched/istockphoto

The Freddie Mac CHOICERenovation program is virtually identical to the Fannie Mae HomeStyle program. This renovation loan is for buyers who want a loan with more flexibility than an FHA renovation loan.

Like HomeStyle, renovations that are permanently affixed to the property are eligible in one- to four-unit residences, one-unit investment properties, second homes, and manufactured homes. The maximum allowable renovation amount is 75% of the “as-completed” appraised value of the home — meaning the appraised value of the home before renovations but accounting for all planned changes. The maximum loan-to-value (LTV) ratio is 95% (97% for HomePossible or HomeOne loans).

The Freddie Mac CHOICEReno eXPress Mortgage is an extension of the CHOICERenovation mortgage. The CHOICEReno eXPress mortgage is a streamlined mortgage for smaller-scale home renovations. Renovation amounts are limited to 10% or 15% of the “as-completed” appraised value of the home. Borrowers need to work with an approved lender to apply for one of these programs.

Nastco/istockphoto

A USDA Purchase with Rehabilitation and Repair Loan assists moderate- to very-low-income households in rural areas with repairs and improvements to their homes. Buyers can secure 100% financing with this loan.

For very low-income borrowers, there’s a separate loan you can qualify for with a subsidized, fixed interest rate set at 1% with a 20-year term. This makes borrowing incredibly affordable.

To apply, you must have a household income that qualifies as low to moderate in your county per USDA standards. The property must be your primary residence (no investments), and rehab funds cannot be used for luxury items, such as outdoor kitchens and fireplaces, swimming pools and hot tubs, and income-producing features.

Manufactured homes, condos, and homes built within the last year are not eligible.

(Learn more: Home Affordability Calculator)

skynesher/istockphoto

The VA allows qualified service members to bundle repairs and alterations with the purchase of a home. As with all VA loans, 100% financing is available on these low-interest loans.

Alterations must be those “ordinarily found” in comparable homes. Renovations are also required to bring the property up to the VA’s minimum property standards.

The loan amount can include the “as completed” value of the home as determined by a VA appraiser. Leftover money from the home loan after renovations are complete is applied to the principal.

KatarzynaBialasiewicz/istockphoto

While a renovation home loan is a great way to finance a renovation, it’s not your only option for borrowing money for home improvements. Nor is it the most flexible. Alternative loans — such as cash-out refis, home renovation personal loans, and home equity loans -– have a lot more flexibility.

Cash-out Refinance

A cash-out refinance is where you replace your old mortgage with a new mortgage, and the equity (here, the “cash”) is refunded to the homeowner. You will have closing costs with a new mortgage, but you won’t have separate financing costs for the money you’re using for renovations.

Personal Loan

Personal loans are often used for a home remodel or renovation. Because the funds are not secured by your property, you’ll likely have to pay a higher interest rate. The bright side of funding this way means you won’t lose your home if you stop paying back the loan.

This type of loan comes with a shorter repayment period, higher monthly payment, and lower loan amount. You can find these loans through banks, credit unions, and online lenders.

Home Equity Loan

A home equity loan is a secured loan that uses your home as collateral. That means the lender can foreclose on the home if you stop paying the loan, and so interest rates are typically lower. A home equity loan also comes with a longer repayment period than a personal loan.

Home Equity Line of Credit (HELOC)

A HELOC is a line of credit that lets homeowners borrow money as needed, up to a predetermined limit. As the balance is paid back, homeowners can then borrow up to the limit again through the draw period, typically 10 years. The interest rate is usually variable, and the borrower pays interest only on the amount of credit they actually use.

After the draw period ends, borrowers can continue to repay the balance, typically over 20 years, or refinance to a new loan.

Private Loan

A private loan is a loan made without a financial institution. Loans made from a family member, friend, or peer-to-peer source are considered private loans. Qualification requirements will depend on the individual or group lending the money. There are some serious drawbacks to obtaining funding from a private source, but these loans can help some borrowers in buying a home.

Government or Nonprofit Program

It is possible to finance the cost of remodeling with the help of government programs. Federal programs like HUD have financing options for renovations, as do some state and local government agencies.

(Learn more at: Personal Loan Calculator)

damircudic/istockphoto

Homeowners have a lot of options for financing renovations, especially in an era when home equity is higher than ever before. Renovation home loans allow borrowers to purchase and renovate a property with one loan, but that’s not the only way you can remodel a fixer-upper. Some alternatives to renovation home loans include home equity loans, HELOCs, and personal loans.

This article originally appeared on SoFi.com and was syndicated by MediaFeed.org.

SoFi Mortgages

Terms and conditions apply. Not all products are offered in all states. See SoFi for more information.

SoFi Loan Products

SoFi loans are originated by SoFi Bank, N.A., NMLS #696891 Opens A New Window.(Member FDIC). For additional product-specific legal and licensing information, see SoFi. Equal Housing Lender.

Non affiliation: SoFi isn’t affiliated with any of the companies highlighted in this article.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

artursfoto/istockphoto

deepblue4you/istockphoto

Featured Image Credit: Joe Hendrickson/istockphoto.