Too Early or Too Wrong?

It’s no secret that bears have found themselves on the wrong side of the market — and in many ways, the economy — so far this year. I count myself as one of them, and nobody likes feeling wrong. It’s my job to use a combination of data, experience, theories, intuition, and history as a basis for making calls, and it’s been endlessly frustrating and humbling to watch things happen differently than I expected. For many months.

The conundrum of this situation is multi-layered. If you believe there will still be trouble ahead and hold your line, the more time that passes without said trouble, the more people will say you’re wrong, not early.

If you change your mind too soon, people will say you’re a flip-flopper who lacks conviction. If you change your mind too late, people will say you capitulated, followed the herd, and gave in.

If you’re a bear for six months and wrong, people will call you stubborn and a permabear. If you’re a bull for six months and wrong, people will call you delusional and say you’re talking your own book.

If you’re right, you’re a hero. But you have to be right at the exact right time. And even when you are, your moment in the spotlight is fleeting.

All of this has brought me to the conclusion that there is no such thing as a state of right or wrong. Even if you’re “right” in one moment, you could be wrong in the next. And there will always be people who think you’re wrong, no matter the circumstances. So we might as well get used to it.

The Right Kind of Trouble

I try to stay out of trouble as much as possible, but if I’m going to get into it, I want it to be good trouble. Good trouble to me is having a somewhat controversial opinion I have strong conviction in, that comes from a place of intellectual honesty and can be backed up by data. It gets me in “trouble” with those who disagree, but it’s good trouble because I believe in the logic of it and am willing to be patient as it plays out.

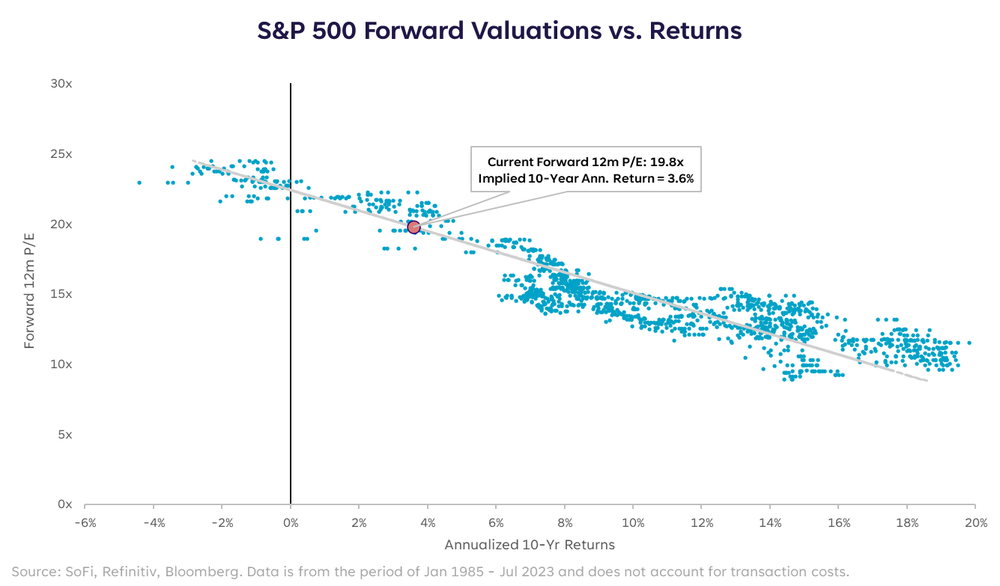

One of those opinions I currently hold is that the outlook for returns from this level of valuations is grim. I am certainly not the only one who thinks this, but the number of investors who believe valuations are justified seems to be growing by the day.

Justified or not, the reality of the chart below is that a forward P/E ratio of nearly 20x suggests that the next 10 years of returns on the S&P 500 will be below average.

The average annual return on the S&P is ~7%. Rarely does a year finish at or around the average, but the long-term expectation for an investor to realize on an annualized basis is generally in that range.

Getting to that average occurs with a combination of ups and downs, some more violent than others, all of them unpredictable. Point being, if from this level of P/E we can only expect a 3.6% annualized return over the next 10 years, there’s more likely to be a pullback in our near future than a blistering rally. Especially after YTD returns of nearly 18% already.

The opinion I stand by in this period is that the price you pay for stocks matters. In fact, I believe it matters more now than ever given where the fed funds rate is, and the sharp rise in borrowing costs as a result. It costs more to finance growth today than it did one year ago. If growth costs more, it needs to offer comparable opportunity.

But has the opportunity really increased that much? Sure, AI gives us a new set of opportunities to follow over the coming years, but does it justify 40% return over seven months? The Nasdaq 100 is up over 40% YTD, much of which was driven by AI-related enthusiasm. Even if that serves as a forward looking mechanism, it suggests that AI has to produce 40% more strength/growth/innovation for those companies (in aggregate) over the next six-to-12 months.

I just don’t think themes materialize that fast.

The Wrong Kind of Time

Regardless of the fact that I think market risks are simply delayed, not dead, the current state of affairs looks less risky than I expected.

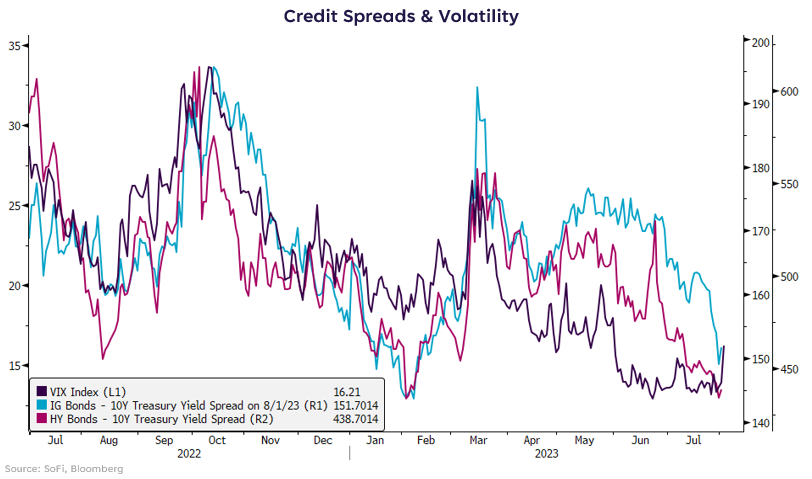

When we look at common risk indicators such as credit spreads and the VIX index, things look decidedly cool, calm, and collected.

In times of increased uncertainty, the VIX tends to hover above 20. In times of certain stress, the VIX tends to spike to 40 or higher. Since the end of March, the VIX has bounced around in a range from 13-18, hardly screaming “stress.”

High-yield credit spreads can be used as a proxy for risk appetite. The tighter the spread, the higher the appetite, and vice versa. In times of stress, HY can exhibit a spread over the 10-year Treasury yield of 1000 basis points or more. This measure has been under 600 basis points all year. If you’re expecting a stressful credit event to rock markets, there’s no sign of it in spreads at this point.

My intuition and knowledge tells me to bend, not break. There are imbalances and inconsistencies in this market that don’t allow me to become a bull and still feel honest with myself. But I recognize that there are multiple indicators telling me I’m wrong. And I very well may end up being “wrong” in the end. The end is coming, and we’ll find out. When we do, and if it becomes clear that we can re-normalize policy, re-steepen the yield curve, and re-start the growth engine without resetting valuations…I will admit defeat. I still don’t think this is the end.

This article originally appeared on SoFi.com and was syndicated by MediaFeed.org.

Are you saving enough money every month?

You likely already know it can be wise to save money every month. Whatever your income or age, putting money aside for the future can help you maintain financial stability and achieve your goals.

But how much of your paycheck should you save each month? Financial experts often recommend putting at least 20% of your monthly take-home income into savings for future financial goals, such as buying a home and funding your retirement.

Exactly how much you should save each month, however, will depend on your income, current living expenses and financial obligations, as well as your goals.

Here are some guidelines to help you figure out how much of your income you may want to set aside each month, plus some simple ways to jump start (or build) your savings.

erdikocak/istockphoto

It can be difficult to know how much money you should save each month without having a sense of what you are saving for. Setting a few financial goals can also help motivate you to save, rather than spend all of your income.

There are some savings goals that can make sense for everyone. If you don’t already have at least three to six-months worth of living expenses stashed in an emergency fund, for example, that can be a good place to start.

Without a solid contingency fund, any financial set-back -– such as a job layoff, large medical bill, or costly home or car repair — can throw you off balance and cause you to rely on high interest credit cards.

Many people will also want to save for retirement. At the very least, savers may want to take advantage of company matches offered in their workplace retirement plan by contributing the maximum amount the company matches.

After emergency savings and retirement, goals may start to look different from person to person. One person may want to save up for a down payment on a home, another may want to save up to start a business, and yet another may be interested in college savings.

(Learn more atHome Affordability Calculator)

javi_indy/istockphoto

A rule of thumb that is sometimes used in personal financial planning is a spending/saving breakdown of 50/30/20. Using this guideline, you would spend 50% of your take-home income on essentials (including minimum payments towards debts), 30% on nonessential (or “fun”) spending, and 20% on savings goals, including debt payments beyond the minimum.

To use the 50/30/20 method to determine how much you should save, you can simply calculate 20% of your monthly after-tax pay. For example, if you earn $3,000 each month after taxes, $600 would go towards savings or other short term financial goals.

You may want to keep in mind that your 20% savings goal can include the money you’re saving for retirement. You can determine how much you’re putting toward retirement each month by looking at your pay stub or electronic payment record. If your employer is automatically depositing money into your 401(k), you may be able to put less into savings each month.

While the 50/30/20 can be a helpful guideline, how much you should — and can afford — to save each month will ultimately depend on your individual circumstances, such as your current income, monthly expenses, and future goals.

If the cost of living is high in your area, for example, you may not be able to swing 20% savings each month.

On the other hand, if you make a significant amount more than you need to live on each month, you may want to put away more than 20%, especially if you’re working towards a large short-term savings goal, such as buying a home in the next couple of years.

Riska/istockphoto

The best account for building savings will depend on what you are saving for.

If you are saving up for retirement, for example, you’ll likely want to use a designated retirement account, like a 401(k) or IRA, since they allow you to contribute pre-tax dollars (which can help lower your annual tax bill).

You may want to keep in mind, however, that there are annual contribution limits to retirement funds.

For an emergency fund or other short-term savings goals (within three to five years), you may want to open a separate savings account, such as a high-yield savings account, money market account, or a checking and savings account. These savings vehicles typically offer more interest than a traditional savings account, yet allow you to easily access your money when you need it.

(Learn more atPersonal Loan Calculator)

shapecharge/istockphoto

Below are some strategies that can help make it easier to start — and build — your monthly savings.

Automating Savings

One great way to make sure you stick to a money-saving plan is to automate the process. You may want to set up a recurring transfer from your checking into your savings account on the same day each month, perhaps the day after your paycheck clears. Even setting aside just a small amount of money each month now can, little by little, add up to a significant sum in the future.

Putting Spare Change to Work

There are apps that will automatically round-up any amount paid on a credit or debit card and then put that little bit of extra money into savings accounts or even invest it. This “pocket change” can add up over time.

Using Windfalls Wisely

If a lump sum of cash, such as a bonus or monetary gift, comes your way, you may want to consider funneling all or part of it right into savings.

Or, if you get a percentage raise on your salary, you might want to boost your automatic monthly transfer from checking to savings by the same percentage.

Reviewing Your Budget

If you feel like your budget is too tight to save anything at the end of the month, you may want to review your monthly and habitual expenses.

You can do this by combing through your checking and credit card statements and receipts for the past few months. Or, you may want to actually track your spending for a month or two.

You can then come up with a list of spending categories and determine how much you are spending on average for each.

Once you can see exactly where your money is going each month, you may find places where you can fairly easily cut back, such as getting rid of streaming subscriptions you rarely watch, quitting the gym and working out at home, or cooking more and getting take-out less often.

Ridofranz/istockphoto

The right amount to save each month will be unique to you and includes factors such as your financial goals, how much you earn, and how much you spend each month on essential expenses.

One of the most important keys to saving is consistency. No matter how much of your income you choose to set aside each month, depositing small amounts regularly can build to a large sum over time to achieve your goals.

This article originally appeared on SoFi.com and was syndicated by MediaFeed.org.

SoFi® Checking and Savings is offered through SoFi Bank, N.A. ©2023 SoFi Bank, N.A. All rights reserved. Member FDIC. Equal Housing Lender.

The SoFi Bank Debit Mastercard® is issued by SoFi Bank, N.A., pursuant to license by Mastercard International Incorporated and can be used everywhere Mastercard is accepted. Mastercard is a registered trademark, and the circles design is a trademark of Mastercard International Incorporated.

SoFi members with direct deposit can earn up to 4.40% annual percentage yield (APY) on savings balances (including Vaults) and 0.50% APY on checking balances. There is no minimum direct deposit amount required to qualify for the 4.40% APY for savings. Members without direct deposit will earn up to 1.20% annual percentage yield (APY) on savings balances (including Vaults) and 0.50% APY on checking balances. Interest rates are variable and subject to change at any time. These rates are current as of 7/11/2023. There is no minimum balance requirement. Additional information can be found at SoFi.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

Tax Information: This article provides general background information only and is not intended to serve as legal or tax advice or as a substitute for legal counsel. You should consult your own attorney and/or tax advisor if you have a question requiring legal or tax advice.

fizkes/istockphoto

aquaArts studio/istockphoto

Featured Image Credit: tdub303/istockphoto.