The Federal Reserve decided not to hike rates at the June FOMC meeting, after hiking at every meeting since Jan 2022, though they indicated that two more hikes were expected by year-end. Resilient economic data is the explanation for more hikes on the horizon, with jobs gains again coming in above estimates for the 14th straight month. Treasury yields moved higher as implied rate volatility fell to its lowest level in months, while stocks moved higher across major size and style categories. Stock gains were largely driven by expanding valuation multiples, as earnings estimates revisions were down marginally. (Learn more at How Many Credit Cards Should I Have?).

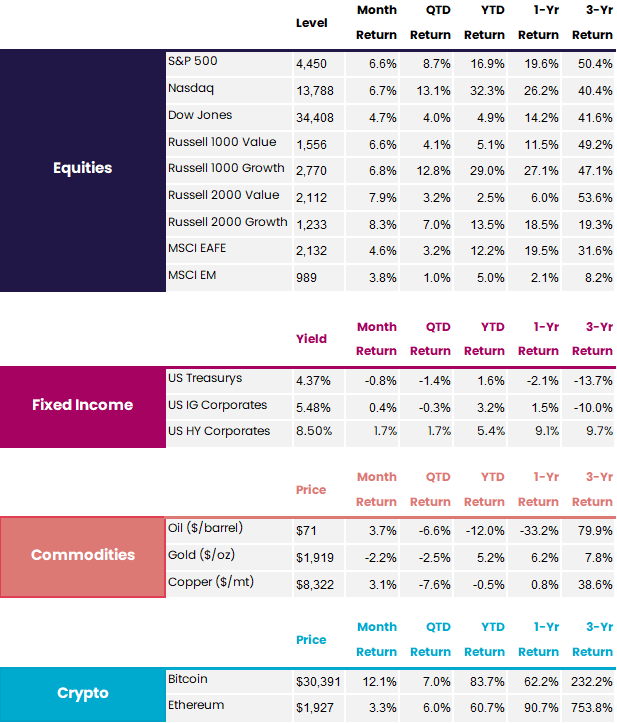

Macro

- The Federal Reserve left the fed funds rate unchanged on Jun 14, though FOMC officials indicated on average, they expect two more hikes by year-end.

- 339k jobs were added in May, above the consensus estimate of 195k, while the unemployment rate rose from 3.4% to 3.7%.

- The May ISM Services index declined to 50.3, below the estimate of 52.4, on the back of weakening New Orders.

- Consumer confidence rose in June according to both the University of Michigan & Conference Board, notably surpassing expectations.

- Q1 GDP & GDI were revised up to 2.0% & -1.8%, respectively, significantly above the prior releases of 1.3% & -2.3%, though still sending conflicting signals.

Equities

- Bottom-up EPS estimates for the S&P 500 in 2023 fell from $220 to $219 in June, while top-down strategist estimates fell from $215 to $214.

- All S&P 500 sectors had positive returns in June, the first such month since Nov 2022.

- The S&P 500 forward 12m P/E surpassed its five-year average for the first time since April 2022.

- Small-cap stocks outperformed large-caps for the first time since Feb 2023.

- Falling as low as 12.91 on Jun 22, the VIX ended the month at 13.59, the lowest since Jan 2020.

Fixed Income

- 2Y & 10Y Treasury yields finished June at 4.90% & 3.84%, respectively, as market pricing shifted in response to Fed guidance & resilient econ data.

- The 2Y10Y yield curve inversion deepened from -76bps to -106bps at the end of the month.

- HY bonds outperformed Treasurys & IG bonds for the third month in a row, the longest such streak in over two years.

- Implied Treasury volatility declined to its lowest level since Feb 2023.

Crypto

- BlackRock and Fidelity Investments filed to launch spot Bitcoin ETFs, which if approved, would be the first spot crypto ETFs in the US.

Don’t Call It a Comeback

At different points this year, it looked like central banks were ready to ease up on their inflation fights. Canada had seemingly ended their hiking cycle in January, the UK & EU moderated their rate hike pace to 25bps in January & May, respectively, and Australia & the US chose to forgo hiking in April & June, respectively, in order to assess the cumulative impact of previous tightening.

One by one, however, central banks have dashed hopes for dovishness. Canada resumed hikes and the UK hiked by 50bps in June, the ECB indicated the tightening cycle would likely extend further into the year, Australia hiked in May & June, and despite pausing in June the Fed indicated that the median expectation was for two more hikes by year-end. Taken altogether, these hawkish messages pushed short-term government yields higher.

Naturally, expectations for where rates will end the year moved up in June as well. Market participants effectively expect one more 25bp hike in Canada & the EU, two more in the US & Australia, and three more in the UK. These moves point to the resilience of growth & inflation data in the face of the sharpest tightening cycle in decades.

Economic Weakening, but When?

For whatever reason, central banks have been unable to slow their economies down enough to be confident that inflation is on its way back to target. Take the Fed for example: despite hiking by 500bps and expecting a period of below-trend growth, they revised their 2023 Q4/Q4 GDP growth projection from +0.4% to +1.0% on Jun 14. Still below trend, but higher than their earlier projections.

Reasons may be mounting, however, that their revision may be overly pessimistic. When the Fed released their June projections, the latest Q1 GDP print was +1.3%, yet on Jun 29 it was revised up to +2.0%. Additionally, the Atlanta Fed’s GDPNow model showed Q2 GDP growth tracking at 2.2% as of Jun 30. If those estimates come to fruition, Q3 & Q4 GDP growth would both have to be 0% for the Fed’s year-end outlook to be correct.

The implications of this are significant. If their GDP projection is too pessimistic, it wouldn’t be surprising for that to trickle into their outlooks on unemployment & inflation. Assuming the Fed remains committed to battling inflation, revising their economic projections higher only raises the odds of them hiking further or waiting longer before cutting. And as many have been saying for the last 12-18 months, the more the Fed tightens, the greater the risk of something breaking. While March upheaval looks mostly behind us, that doesn’t mean something else isn’t ahead of us.

This article originally appeared on SoFi.com and was syndicated by MediaFeed.org.

Please understand that this information provided is general in nature and shouldn’t be construed as a recommendation or solicitation of any products offered by SoFi’s affiliates and subsidiaries. In addition, this information is by no means meant to provide investment or financial advice, nor is it intended to serve as the basis for any investment decision or recommendation to buy or sell any asset. Keep in mind that investing involves risk, and past performance of an asset never guarantees future results or returns. It’s important for investors to consider their specific financial needs, goals, and risk profile before making an investment decision.

The information and analysis provided through hyperlinks to third party websites, while believed to be accurate, cannot be guaranteed by SoFi. These links are provided for informational purposes and should not be viewed as an endorsement. No brands or products mentioned are affiliated with SoFi, nor do they endorse or sponsor this content.

Communication of SoFi Wealth LLC an SEC Registered Investment Advisor

SoFi isn’t recommending and is not affiliated with the brands or companies displayed. Brands displayed neither endorse or sponsor this article. Third party trademarks and service marks referenced are property of their respective owners.

Communication of SoFi Wealth LLC an SEC Registered Investment Adviser. Information about SoFi Wealth’s advisory operations, services, and fees is set forth in SoFi Wealth’s current Form ADV Part 2 (Brochure), a copy of which is available upon request and at here. Liz Young is a Registered Representative of SoFi Securities and Investment Advisor Representative of SoFi Wealth. Her ADV 2B is available at here.

Have you fallen for any of these huge American money scams?

Scammers have been around forever, and the only thing that changes from year to year, it seems, is the technology they use to pull off their scams. While many of these con artists still use the phone, the mail or even in-person tactics to try to part you from your hard-earned money, most scams these days are pulled off digitally — reaching you through your email, text messages and fake websites.

According to the Better Business Bureau, nearly 75 percent of consumers lost money to a purchase scam in the first eight months of 2021. And the amount consumers lose every year continues to rise, from an average of $76 in 2019 to $102 in 2021.

To help folks battle these scammers, we’ve rounded up some of the biggest, most common scams hitting American consumers this year with tips to help you avoid them and a guide on how to report scams if you do become a victim.

According to the Federal Trade Commission, some of the most common bank scams include the following. (Learn more at 3 reasons why your bank account is frozen)

Editor’s note: Updated July 2

PRImageFactory / iStock

Many con artists try to get between you and your dollars by tricking you into sending them funds directly. Scammers typically start off by sending you a fake check in the mail, but because they’ve sent you “too much” money, they reach out instructing you to deposit the full check into your bank account and send the overpaid portion back to them via check or wire transfer. As a rule of thumb, you should contact your bank before depositing checks from anyone you don’t recognize.

fizkes / iStock

In this scam, a company sets up automatic withdrawals from your bank account in order for you to “qualify” for a free trial or to collect a prize. Some companies will also legitimately charge you for a purchase but will continue charging you each month because your purchase signed you up for some obscure product or service that requires monthly billing. Consider protecting your banking information by using a credit card instead. Unauthorized charges are easier to dispute, and you don’t provide anyone with direct access to your money.

SB Arts Media / iStock

It’s hard to imagine a worse scam than stealing money in the name of people in need, but it’s a tried-and-true grift we should all be on the lookout for, especially around the holidays or after emergencies/natural disasters. Scammers pose as a real charity (or one that sounds real) and call, mail or email asking that you help with some recent tragedy. Instead of making a donation pledge right then and there, it’s smart to tell them you’ll contact them through the organization’s official website or phone number noted there.

DepositPhotos.com

Also popular around the holidays are “grandparent scams” where scammers call older adults pretending to be a grandchild or other relative. They claim they are in trouble and need help, often asking that you wire them money or send them a gift card so they’ll have the cash they need. If this happens to you, it’s smart to tell the caller you need to call them back. That will allow you to contact your relative directly to confirm if the request was real or fake.

DepositPhotos.com

A cross between charity and grandparent scams, imposter scams typically work something like this: A caller tries to persuade you to give money to their organization or government agency (think police and firefighter funds). As they’re often able to fake their caller ID, the grift may seem legitimate. Instead of contributing over the phone, it’s a good idea to directly contact the organization the person claims to be associated with and make a donation that way if you’re so inclined. You can read more about imposter scams.

Diy13 / iStock

Dealing with legitimate debt collectors can already be stressful, but there are guidelines they must adhere to which can make identifying a scammer easier. An overly aggressive “debt collector” may be a scammer in disguise. These warning signs can help you further recognize if you’re being targeted, and these sample letters can be used to request more information if you’re still questioning the legitimacy of someone contacting you about a debt.

depositphotos.com

It’s estimated that more than $40 billion in unclaimed money is out there waiting to be claimed by its rightful owners, mostly languishing with state governments. Some companies may offer to help you find and recover unclaimed money for a percentage of the found funds. Paying these fees is pointless, since you can search for unclaimed property and reclaim it for free (or perhaps for a small processing fee) on official databases.

B4LLS / iStock

For people who are behind on their mortgage payments, this can be a truly frightening scam. These con artists often offer to save you from foreclosure, but they require upfront fees for their “services,” such as loan modification. Sometimes they’ll even ask for you to sign over the title or rights to your property on paperwork you don’t understand. If you’re contacted with mortgage promises that sound too good to be true, it’s a good idea to contact a HUD-approved housing counselor who can help you avoid scams and review your actual payment options.

Ausettha / istockphoto

These scams target homebuyers whose mortgage closing date is approaching. They attempt to separate the homebuyer from their down payment and/or closing costs by pretending to be a realtor, title company, escrow company or other mortgage-related company or entity.

Like with so many other scams, it’s important to communicate directly with people and companies you already know who can verify if these information requests are legitimate. The Consumer Financial Protection Bureau has put together some helpful information to help you protect your closing funds.

nortonrsx / iStock

If you ever receive a letter asking you for money or personal information in order to receive a prize from a lottery or sweepstakes, or in order to claim an offer of a high value item like a car or a vacation, it could be a scam. The U.S. Postal Service has identified common postal or mail fraud schemes to help you avoid some of the most common ones.

fizkes / iStock

Targeting the heartbroken is another tried-and-true con that scam artists just love. Typically, the scammer tries to trick you into being romantically interested in them so they can ask you for money or get you to share personal information like credit card numbers, bank account details and even your Social Security number. These romances can lead to financial ruin, so stay alert and don’t send money or gifts to a love interest that you haven’t met in person.

Fizkes / iStock

If you think you’ve been a victim of a scam, you can report it by:

- Submitting an online complaint with the Federal Trade Commission

- Contacting your local police department or sheriff’s office

- Reporting it to your state’s attorney general

fizkes / iStock

Though scams abound, you’re not completely vulnerable. There are plenty of things you can do to help protect yourself against scams and scammers. Here are some of our favorites.

Depositphotos

In general, credit cards can offer significantly better fraud protections than debit cards, which are directly connected to your bank account. Plus, a lot of credit cards also offer additional services like purchase protection, price protection and extended warranties.

Mobile apps (think Apple Pay and Google Pay) offer advanced technologies, like fingerprint authentication and “tokenization” (credit card account numbers are replaced by randomly generated numbers) to provide added layers of security. Similarly, virtual credit cards similarly allow online shoppers to mask their financial accounts.

DepositPhotos.com

No matter how you prefer to pay for purchases, checking your bank and credit card statements regularly for suspicious or erroneous charges can help you spot fraudulent activity right away. You may want to do this daily during periods of high usage, like around the holidays when it’s easier for fraudulent charges to slip through.

Rawpixel / iStock

Many banks and other financial institutions offer free transaction alerts each time a new change hits your account. Like reviewing your statements, these alerts can help you spot suspicious activity right away.

DepositPhotos.com

If you do spot something unusual when reviewing statements or alerts, it’s a good idea to contact your financial institution right away. You’ll be able to immediately cancel your compromised card(s) and get replacements so you can get on with your life and hopefully avoid further issues.

SeventyFour/ istockphoto

If you get a call asking for your payment information or other personal information, it’s smart to just hang up and call the company directly so you can avoid potential fraud.T his goes for your address, phone number and especially your Social Security number.

DepositPhotos.com

Is your smartphone, tablet or laptop password-protected? If not, it can be an important first line of protection against fraud, so it’s definitely something to consider. If you’re unsure how to do it, enlist the help of a trusted friend or relative (but it’s still smart to set your own password that they are not privy to).

Also, you may want to keep in mind that browsers like Firefox, Google Chrome and Safari issue updates to protect against scams, so it’s wise to ensure you have the latest version of whatever browser you use. You may also want to consider purchasing antivirus software to keep your computer clean and safe.

DepositPhotos.com

If you like to use your phone for shopping or banking while sitting at your local coffee house and using their Wi-Fi, you may want to reconsider that. Public Wi-Fi networks are well known spots where hackers and scammers steal personal information. That’s why a virtual private network (VPN) can be a smart choice for connecting to the internet when you’re away from home. It’s much harder to pick up information you may transmit than it is over a public network.

DepositPhotos.com

Shopping only at reputable and recognized retailers, especially online, can help you avoid some of the fraud headaches abounding out there. If you are concerned about an unfamiliar retailer you want to transact with, consider researching them on the Better Business Bureau website. You can also check out their site state using Google’s Transparency Report tool.

DepositPhotos.com

Does that ATM or gas pump look a little weird? It’s not uncommon for scammers to install skimmers in places where consumers swipe their credit and debit cards. These devices snatch your payment information, including PIN codes whenever used. Take a close look at whatever reader you’re using to swipe your card. If it looks suspicious, report it to the establishment.

DepositPhotos.com

Did you get a weird notice from your bank or pharmacy? How about a text message from AT&T that your phone bill has been paid as a “gift”? It’s possible the unsolicited offer you receive is a “phishing” scheme. Scammers often pose as a legitimate company or website in order to get you to click on a link that either asks for personal info or downloads malware on your device. They can use emails or even texts to try to get you to bite. If it looks fishy, avoid clicking on any links or downloading any attachments.

DepositPhotos.com

Putting this advice into practice can definitely help keep you safe and your money in your pockets, but it can’t guarantee you won’t become a victim. Here are some additional things to keep in mind that can help boost your overall awareness.

Michael Krinke

Keeping things simple is almost always a good idea, and that’s true of avoiding scams as well. If you’re shopping online, it’s super smart to check that the website url starts with HTTPS instead of just HTTP when you’re checking out.

That means it has a Secure Sockets Layer certificate, meaning all your data will be encrypted. On secure sites, you’ll see a little padlock icon in your browser’s address bar.

RobertAx / iStock

Scam artists really aren’t known for their stellar online reviews, so if a company you’re considering buying from has a bunch of bad reviews (or no reviews at all), you may want to strongly consider taking your business elsewhere.

HAKINMHAN/ iStock

Is the website you’re considering making a purchase from riddled with misspelled words and grammatical errors? Typos can be a sign of scammers, so if what you’re reading looks a little off, you might want to reconsider purchasing from that site. It’s also good practice to check website urls for little differences (think Bestbyy.com instead of BestBuy.com).

Pheelings Media / iStock

The strength of your password can be very important, but what’s considered “strong?” Passwords that are hard to crack generally have a random mix of letters, numbers and symbols, but long phrases like song lyrics that are easily remembered can also be used. Also, keep in mind that a password used on more than one site actually makes you more vulnerable, so take the time to customize your logins.

istockphoto

If you’re shopping in a brick-and-mortar store, it’s smart to keep your purse and/or wallet close and secure at all times. This may mean moving your wallet to your inside pocket and wearing your purse strap over your head, especially during the holidays when stores are busier. In fact, traveling light can be the smartest way to ensure you don’t have your purse or wallet stolen. What’s traveling light? Consider carrying just one card with you into the store and leaving your cash and checkbook at home.

chabybucko

While there will likely always be someone willing to cheat others out of their money, there are obvious ways you can help protect yourself. Staying alert and following your instincts can help, but implementing security measures and keeping some key tips in mind can make it harder for thieves to get at your dollars.

This article

originally appeared on SoFi.comand was

syndicated by MediaFeed.org.

SoFi Money

SoFi Money is a cash management account, which is a brokerage product, offered by SoFi Securities LLC, member FINRA / SIPC . Neither SoFi nor its affiliates is a bank. SoFi Money Debit Card issued by The Bancorp Bank. SoFi has partnered with Allpoint to provide consumers with ATM access at any of the 55,000+ ATMs within the Allpoint network. Consumers will not be charged a fee when using an in-network ATM, however, third party fees incurred when using out-of-network ATMs are not subject to reimbursement. SoFi’s ATM policies are subject to change at our discretion at any time.

External Websites: The information and analysis provided through hyperlinks to third party websites, while believed to be accurate, cannot be guaranteed by SoFi. Links are provided for informational purposes and should not be viewed as an endorsement.

Third Party Brand Mentions: No brands or products mentioned are affiliated with SoFi, nor do they endorse or sponsor this article. Third party trademarks referenced herein are property of their respective owners.

AleksandarGeorgiev

DepositPhotos.com

Featured Image Credit: Huang Evan/istockphoto.