Assuming a mortgage means that the buyer of a home is able to take over the seller’s existing mortgage. When mortgage assumption is possible, it may help a buyer score a lower interest rate and save money in other ways as well. In times when interest rates are headed upward, an assumable mortgage can be quite a windfall.

But, reality-check time: Mortgages are only assumable in certain situations, and there are pros and cons to consider. If you’re home shopping and want to consider this option, read on to learn more, including:

- What is an assumable mortgage?

- How do I know if a mortgage is assumable?

- What are the benefits of an assumable home loan?

- What are the downsides of an assumable mortgage?

What Is an Assumable Mortgage?

The meaning of an assumable mortgage is that the buyer, when purchasing a home, takes over the existing mortgage held by the seller. This means the buyer assumes responsibility for the loan’s outstanding balance, its interest rate, and making payments for the entire loan term.

This can be an appealing option if, say, the seller’s mortgage was taken out with a considerably lower interest rate than is currently available. In this scenario, the buyer could stand to save thousands over the life of the mortgage loan.

However, a buyer may also need to finance the amount of equity the seller has in the home.

It’s important to note that not all mortgages are assumable. For those that are, it’s recommended that all parties know in advance what obligations they have when they agree to a mortgage assumption, just as with any other financial agreement.

What Types of Loans Are Assumable?

Typically, home loans that operate outside the federal government’s mortgage loan environment, such as conventional 30-year mortgages issued by private lenders, are not assumable. (How do you know if a conventional mortgage is assumable? It will likely be an adjustable-rate loan, and the seller will have to check with their lender to be sure.)

Certain kinds of mortgages that are insured by the government and issued by private lenders are, however, assumable. A seller usually must obtain lender approval for the assumption, or in the case of USDA loans, agency approval. And the buyer must qualify. These loans include:

- FHA loans: The Federal Housing Administration (FHA) insures these mortgages, which are popular with first-time homebuyers. With a minimum 3.5% down payment for borrowers with a credit score of 580 or higher, FHA mortgages are assumable.

- VA loans: Home loans guaranteed by the Department of Veterans Affairs (VA) are also assumable, and — perhaps surprisingly — the buyer does not have to be a veteran or in the military. Note: The seller of these loans may remain responsible for the mortgage if the buyer defaults.

- USDA loans: Loans guaranteed by the Department of Agriculture (USDA) are assumable only if the current owner is up to date on payments.

One last note about the options above: While assumable mortgages can be part of a wrap-around mortgage, they are not one and the same.

When a mortgage is assumed, the buyer pays the lender every month. With a wrap-around mortgage, which is a kind of owner-financing, the buyer pays the seller.

How to Get an Assumable Mortgage Loan

Here are some points to consider if you are contemplating assuming a mortgage:

- First, confirm that the loan is assumable. For most conventional mortgages, assumption is not an option.

- If assumption is possible, the homebuyer must apply for the assumable mortgage and be vetted for creditworthiness and the ability to meet all the contractual requirements. It’s vital that the buyer show that they have the financial assets needed to qualify for the loan.

- Recognize that the buyer will need to make up any difference between the amount owed and the home’s current value. This means that if the seller of a $300,000 home has a $100,000 mortgage that’s assumable, the buyer would need to be able to put down $200,000 to assume that loan. Obviously, this scenario could present a significant financial hurdle for many prospective homebuyers.

- If the mortgage lender or agency signs off on the deal, the property title goes to the homebuyer, who starts making monthly mortgage payments to the lender.

- If the lender denies the application, the home seller must move on, and the buyer would likely resume shopping elsewhere.

Why Do Assumable Mortgages Exist?

Actually landing an assumable debt can be beneficial for both a buyer and seller, but the mortgage lending industry may not make it easy to cut a deal. Why? Because as history attests, mortgage lenders may lose money on assumable mortgages.

In the late 1970s and early 1980s, when interest rates were at the highest levels in modern history, assumable mortgage deals were attractive to buyers who could take over a seller’s mortgage at the original loan interest rate. In many cases, this would yield a bargain vs. the then-current rate for a new mortgage. (How high did rates go? In October 1981, 30-year fixed-rate mortgages hit an eye-watering peak of 18.45%.)

Mortgage companies, however, could see that they would lose money if home buyers chose a lower-rate assumable loan over a higher-rate new mortgage loan. That’s one reason mortgage companies began inserting “due on sale” clauses, which mandated full repayment of the loan for most home transactions.

As the FHA and VA began issuing more mortgage loans to homebuyers, they offered more relaxed rules allowing assumption transactions. Mortgages could transfer to the homebuyer as long as they demonstrated the ability to repay the remaining home loan balance, usually after a thorough credit check.

How Do Assumable Mortgages Work?

With an assumable mortgage, the buyer will become the holder of the mortgage originally taken out by the seller. The buyer, as mentioned above, may have to clear certain qualification hurdles to do so.

It’s also important to note that, as briefly mentioned above, the homebuyer must make up any difference between the amount owed on the mortgage and the property’s current value. That could mean the buyer pays cash to make up the difference or takes out a second mortgage.

An example: Say a house is valued at $350,000, and the home seller has a $225,000 balance on the home’s original mortgage. Under the terms of most assumable mortgage loans, the homebuyer would need to deliver $125,000 at closing to cover the difference between the original mortgage and the current estimated value of the home, usually determined by an appraisal.

Another important aspect of how assumable mortgage loans work are the two models possible: a simple mortgage assumption or a novation-based mortgage assumption.

Simple Assumption

In a typical simple mortgage assumption, the buyer and seller agree to engage in a private transaction.

- This means that the mortgage lender is not necessarily aware of the transfer of the mortgage and therefore the new buyer does not go through the underwriting process with the lender.

- The home seller usually just transfers the title of the property to the buyer after the buyer agrees to take over the remaining mortgage payments.

- If the buyer misses monthly payments or defaults on the original mortgage loan, the lender could hold both parties responsible for the debt, and the credit scores of both buyer and seller could be significantly damaged if the debt isn’t repaid. In this scenario, an assumable mortgage home for sale could wind up being problematic for both parties.

Novation-Based Assumption

Unlike a simple mortgage assumption, where mortgage underwriting usually isn’t directly involved, an assumption with novation means the lender is involved.

- The lender vets the buyer and agrees to the loan transfer.

- This means the buyer agrees to assume total responsibility for the existing mortgage debt and remaining payments.

- Under those terms, the original mortgage lender releases the home seller from liability for the remaining mortgage loan debt. The documentation, such as a deed of trust (if used), will be in the buyer’s name alone.

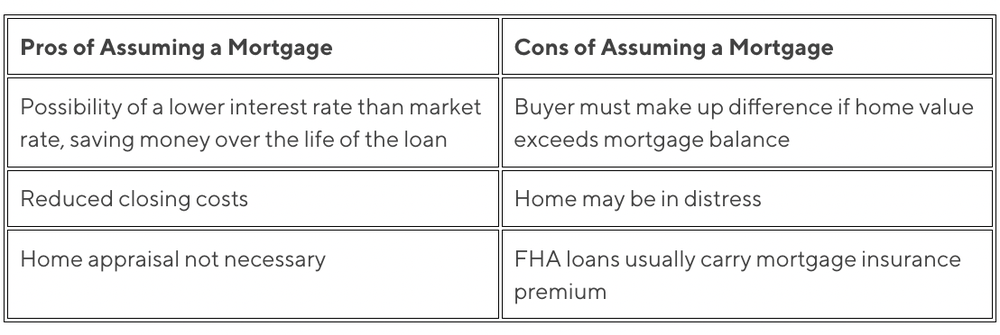

Pros and Cons of Assumable Mortgages

Assumable mortgage loans have upsides and downsides.

Upsides of an Assumable Mortgage

First, consider these pluses:

- A lower rate may be possible. The buyer may save significant money on the loan if the original mortgage’s interest rate is lower than current rates.

- Closing costs are curbed. The buyer might also benefit because closing costs are minimized in private home sale transactions between a buyer and a seller.

- No appraisal is needed. With no need to get a new mortgage on the property, a home appraisal isn’t required for a mortgage assumption, which can save time and money. The buyer could request an appraisal as part of the general home purchase agreement, however.

Downsides of an Assumable Mortgage

Now, the minuses:

- Upfront cash may be required. To meet the terms of an assumable mortgage, the buyer may need to have a substantial amount of upfront cash or take out a second mortgage to close the deal. This usually occurs when the property’s value is greater than the mortgage balance. The seller has perhaps built up considerable equity over the years.

- Second mortgages can be problematic. Second mortgages aren’t always easy to obtain, as mortgage lenders may be reluctant to issue a second home loan when the original mortgage still has a balance due. And a second mortgage probably carries closing costs, meaning the seller needs to shell out more cash.

- The property may be in distress. In some cases, the home seller may be eager to get out of a home that is proving to be too expensive for their budget. Simply put, they might be behind on payments. In that event, the mortgage lender may require the mortgage to be made current (meaning getting up to date on payments) before it will approve an assumable mortgage.

- FHA loans carry an add-on. If the home seller put down less than 10% of the home’s cost when getting an FHA loan, there will be a mortgage insurance premium for the entire loan term. This would add to the buyer’s monthly costs.

Here’s how this intel stacks up in chart form:

Examples of Assumable Mortgages

If you’re hoping to find an assumable mortgage, it will most likely be a government-insured or -issued loan, as mentioned above; perhaps one offered as a first time homebuyer program. Here’s a bit more about these mortgages and how a loan assumption would work:

- Federal Housing Authority (FHA) loans: These government loans, which are insured by the FHA, may be assumable. Both parties involved in a mortgage assumption, however, must qualify in certain ways. For instance, the seller must have been living in the home as a primary residence for a period of time, and the buyer needs to be approved via the usual FHA loan application process.

- Veterans Affairs (VA) loans: If a seller has a loan backed by the VA, it may indeed be assumable. A buyer who wants to take over the loan can apply for a VA loan assumption and doesn’t need to be a current or former member of the military service.

- U.S. Department of Agriculture (USDA) loans: To assume a USDA loan on a rural property, a buyer will have to show an adequate income and credit to be approved by the USDA.

Who Are Assumable Mortgages For?

Assuming a mortgage can be a good option for those who are property shopping in a time of rising interest rates and would like to take over the seller’s lower-rate loan. This can help save money, and it can also spare the buyer some of the time, energy, and money needed to apply for a new loan.

In addition, an assumable mortgage may work best for buyers with access to cash, as they will probably need to cover the difference between the mortgage amount and the value of the home they are buying.

Who Are Assumable Mortgages Not For?

Those purchasing a home that currently has a conventional mortgage will most likely not be able to take over that loan.

Additionally, if a mortgage is assumable, it’s important to recognize this scenario: If there’s a considerable gap between the mortgage amount and the property’s value, the buyer needs to bridge that. That means either ponying up a chunk of cash or finding a second mortgage, which may not be financially feasible for some prospective homebuyers.

The Takeaway

Assumable home loans are generally difficult to find and to close, and may require the buyer to take on the onerous task of qualifying for a second mortgage. But if the buyer finds that assuming the mortgage will save money over getting a new mortgage (primarily through a lower rate), an assumable mortgage could be a good way to go.

This article originally appeared on SoFi.com and was syndicated by MediaFeed.org.

Please understand that this information provided is general in nature and shouldn’t be construed as a recommendation or solicitation of any products offered by SoFi’s affiliates and subsidiaries. In addition, this information is by no means meant to provide investment or financial advice, nor is it intended to serve as the basis for any investment decision or recommendation to buy or sell any asset. Keep in mind that investing involves risk, and past performance of an asset never guarantees future results or returns. It’s important for investors to consider their specific financial needs, goals, and risk profile before making an investment decision.

The information and analysis provided through hyperlinks to third party websites, while believed to be accurate, cannot be guaranteed by SoFi. These links are provided for informational purposes and should not be viewed as an endorsement. No brands or products mentioned are affiliated with SoFi, nor do they endorse or sponsor this content.

Communication of SoFi Wealth LLC an SEC Registered Investment Advisor

SoFi isn’t recommending and is not affiliated with the brands or companies displayed. Brands displayed neither endorse or sponsor this article. Third party trademarks and service marks referenced are property of their respective owners.

Communication of SoFi Wealth LLC an SEC Registered Investment Adviser. Information about SoFi Wealth’s advisory operations, services, and fees is set forth in SoFi Wealth’s current Form ADV Part 2 (Brochure), a copy of which is available upon request and at www.adviserinfo.sec.gov. Liz Young is a Registered Representative of SoFi Securities and Investment Advisor Representative of SoFi Wealth. Her ADV 2B is available at www.sofi.com/legal/adv.

What is mortgage fraud? Mortgage fraud refers to lying or omitting information to fund or insure a mortgage loan. It results in billions of dollars in annual losses nationwide.

In 2021, fraud risk increased 37% over 2020 levels, CoreLogic found, and the fraud rate averaged 1 in 120 loans — 1 in 23 for investment purchases. The top three states for mortgage application fraud risk the year before? New York, Nevada, and Florida.

The FBI investigates two distinct areas of mortgage fraud: fraud for profit and fraud for housing.

fizkes / iStock

The FBI says that those who commit this type of mortgage fraud are often industry insiders. Current investigations and reporting indicate that a high percentage of mortgage fraud involves collusion by bank officers, appraisers, mortgage brokers, attorneys, loan originators, and other professionals in the industry.

The FBI points out that fraud for profit is not about getting a home, but manipulating the mortgage process to steal cash and equity from lenders and homeowners.

fizkes / iStock

It’s not only industry insiders who can look to milk the system. With fraud for housing, the perpetrators are borrowers who take illegal actions in order to acquire or maintain ownership of a house.

They could do this by lying about income or presenting false information about assets on their loan application, for example.

Related: Why most people don’t get mortages from banks anymore

DepositPhotos.com

Borrowers who know they are not really mortgage-ready — perhaps because of a poor credit history, a low credit score, or a nothing-to-brag-about salary that would likely get them the thumbs down from a lender — may be driven to try to enhance their chances of getting a loan, even by illegal means.

As for industry professionals, be it appraisers, real estate agents, mortgage brokers, or anyone who has a role in the home buying and selling process, they could be motivated by the almighty dollar. If they can look the other way to get the transaction done, or manipulate facts so they get their piece of the action, they may do so.

DepositPhotos.com

Mortgage fraud is serious. It’s typically a felony. Conviction for federal mortgage fraud can result in a federal prison sentence of 30 years; state convictions can last a few years. If the crime is a misdemeanor and the amount involved is less than $1,000, there can be a one-year sentence.

A conviction on a single count of federal mortgage fraud can result in a fine of up to $1 million. State fines can range from a few thousand dollars for a misdemeanor to $100,000 or more for a felony.

Expect to pay restitution to compensate the victims and to be on probation following jail time.

Mortgage fraud comes in many flavors. Scammers are big on creativity. The FBI has a list of mortgage scams to watch out for. Here are a few of theirs and others to keep in mind.

Damir Khabirov / iStock

There’s nothing innately evil about flipping properties. In fact, adding investment properties to your portfolio can be a way to build wealth if you’re good at it. But then there’s the sinister side of flipping.

It goes something like this: A property is purchased below the market price and immediately sold for profit, typically with the help of a shady appraiser who puffs up the value of the property. This is illegal.

DepositPhotos.com

The FBI explains how this works: An investor may use a straw buyer, false income documents, and false credit reports to obtain a mortgage loan in the straw buyer’s name.

After closing, the straw buyer signs the property over to the investor in a quit-claim deed, which relinquishes all rights to the property and provides no guarantee to title. The investor does not make any mortgage payments and rents the property until foreclosure takes place several months later.

AaronAmat / iStock

It’s one thing to borrow something blue on your wedding day, and quite another to borrow or rent the assets of your best friend or loved one to make yourself look better in the eyes of a lender. You “borrow” the asset, maybe a hefty chunk of cash, and after the mortgage closes, you give it back to your partner in crime.

fizkes / istockphoto

Appraisers have the keys to the kingdom. They state the fair market value of a home. Crooked appraisers can do a couple of things that are illegal. They can undervalue the property so that a buyer gets a “deal,” or more often, they overstate the value of the property. The goal is to help a buyer or seller, or a homeowner planning to refinance or tap home equity.

ronstik / iStock

Identity theft is an epidemic. According to the Federal Trade Commission, in 2020, it received about 1.4 million reports of identity theft, double the number from 2019.

Scammers use financial information like Social Security numbers, stolen pay stubs, even fake employment verification forms to get a fraudulent mortgage on a property they do not own. If you’ve been a victim, report identity theft as soon as possible.

DepositPhotos.com

Talk about kicking somebody when they’re down. Predators seek out those who are in foreclosure or at risk of defaulting on their loan and tell them that they can save their home by transferring the deed or putting the property in the name of an investor. It can sound rational when you’re desperate.

The perpetrator cashes in when they sell the property to an investor or straw borrower, creating equity using a fraudulent appraisal and stealing the seller proceeds or fees paid by the homeowners. The homeowners are typically told that they can pay rent for at least a year and repurchase the property when their credit has improved.

But that’s not how the story goes. The crooks don’t make the mortgage payments, and the property will likely wind up going into foreclosure. Heavy sigh.

DepositPhotos.com

This may as well be in a movie, because nothing is real with this scheme. The FBI describes an air loan as a nonexistent property loan where there is usually no collateral.

Brokers invent borrowers and properties, establish accounts for payments, and maintain custodial accounts for escrow. They may establish an office with a bank of phones, each one used as the fake employer, appraiser, credit agency, and so on, to deceive creditors who attempt to verify information on loan applications.

tommaso79 / istockphoto

A lie can be what you leave out as much as what you say. Given the nature of how self-employed people file taxes, some do not report their full income on their taxes. When it comes to a “stated income” loan, a borrower claims a certain amount of income, and an underwriter makes a decision based on that figure to give them a loan or not.

If the borrower tells a little white lie about their income, it’s not little at all. It’s mortgage fraud.

istockphoto

You can receive part of a down payment for a home, but the gift is not to be repaid. In fact, when you plan to use gift funds, you’ll need to provide a gift letter that proves the money is not a loan to be repaid.

You may also be asked to provide documentation to prove the transfer of the gift into your bank account. This may include asking the donor for a copy of their check or bank account statement.

If that gift is to be repaid, it is mortgage fraud. It can also put your loan qualification at risk, as all loans need to be factored into your debt-to-income ratio.

DepositPhotos.com

When it comes to buying or selling a house, there are a lot of moving parts, a lot of cooks in the kitchen. It’s a good idea to, above all, be truthful about everything, and if anyone along the way seems to be pushing you in any other direction, you could pay dearly for taking that bad advice.

You can play the game straight, but what about all the others involved in the process? It’s smart to get referrals for companies and real estate and mortgage pros that you’ll be working with, and to check state and local licenses.

Was your property evaluation, or appraisal, on target? It might be helpful to look at other homes that are similar to see what they have sold for, and recent tax assessments of nearby homes.

Guard your John Hancock. Be careful what you sign, and never sign a blank document or one containing blank lines.

Another no-go is signing over the house deed “temporarily.” This could be a set-up. Someone may be asking you to sign over your house deed as part of a scheme to avoid foreclosure. Know that chances are you’ll lose your house permanently.

fizkes/ iStock

What do you do if you’re the victim of mortgage fraud? Your local police department may take a report. Your state attorney general’s office may be another good resource.

The FBI, however, is the agency that handles most mortgage fraud investigations. You can go to tips.fbi.gov to report a crime. Other federal agencies also investigate mortgage fraud, but the FBI is likely the best first option.

SeventyFour/ istockphoto

Mortgage fraud isn’t rare, and both industry insiders and borrowers can be involved. It’s smart to approach the process of getting a home loan with care, asking your lender questions, visiting this help center for home loans and using a mortgage calculator tool to gauge the effect of different down payments.

Learn More:

This article originally appeared on SoFi.com and was syndicated by MediaFeed.org.

SoFi Loan Products

SoFi loans are originated by SoFi Bank, N.A., NMLS #696891 Opens A New Window.(Member FDIC), and by SoFi Lending Corp. NMLS #1121636 Opens A New Window., a lender licensed by the Department of Financial Protection and Innovation under the California Financing Law (License # 6054612) and by other states. For additional product-specific legal and licensing information, see SoFi.com/legal.

SoFi Home Loans

Terms, conditions, and state restrictions apply. Not all products are available in all states. See SoFi.com/eligibility for more information.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

DepositPhotos.com

svetikd

Featured Image Credit: BongkarnThanyakij/istockphoto.