Livin’ on a Prayer

The next stop on the market news train is Q1 earnings season, which begins in earnest next week, and the industry group kicking it off is…wait for it…banks. All eyes and ears will undoubtedly be on regional bank earnings and guidance from big bank CEOs, but the rest of the industry groups could be just as interesting to watch.

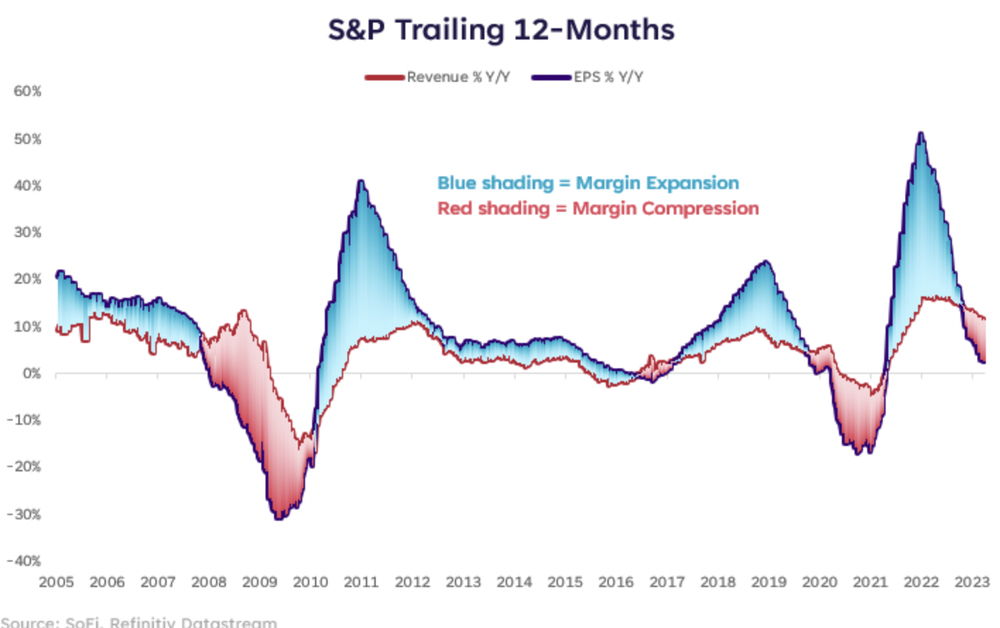

Aside from the fact that I am a Bon Jovi fan, this earnings season does feel a bit like we’re livin’ on a prayer that profit margins don’t contract too much. The story has been that profit margins are high enough to withstand a little pullback in revenue growth and increased costs from inflation — largely because consumers have thus far absorbed price increases.

A potential hole in that story is that consumers can change their minds on a dime, and they’ll only absorb price increases until they very abruptly won’t. The problem with that timing is that companies cannot react as quickly as consumers can change their behavior — which may result in too much inventory and the need to reduce prices in order to unload it later on. Lower prices mean lower revenue. Lower revenue without equally lower costs means lower earnings.

We’re Halfway There

As of now, Q1 earnings growth on the S&P 500 is expected to come in at roughly -6% y/y. After Q4’s -3.5% growth, we were halfway to what’s called an “earnings recession” (two consecutive quarters of negative growth), and if Q1 posts a negative result we’ll have fully checked the box. It’s worth noting that current estimates also call for -4% growth in Q2 2023 earnings, so the contraction is expected to continue.

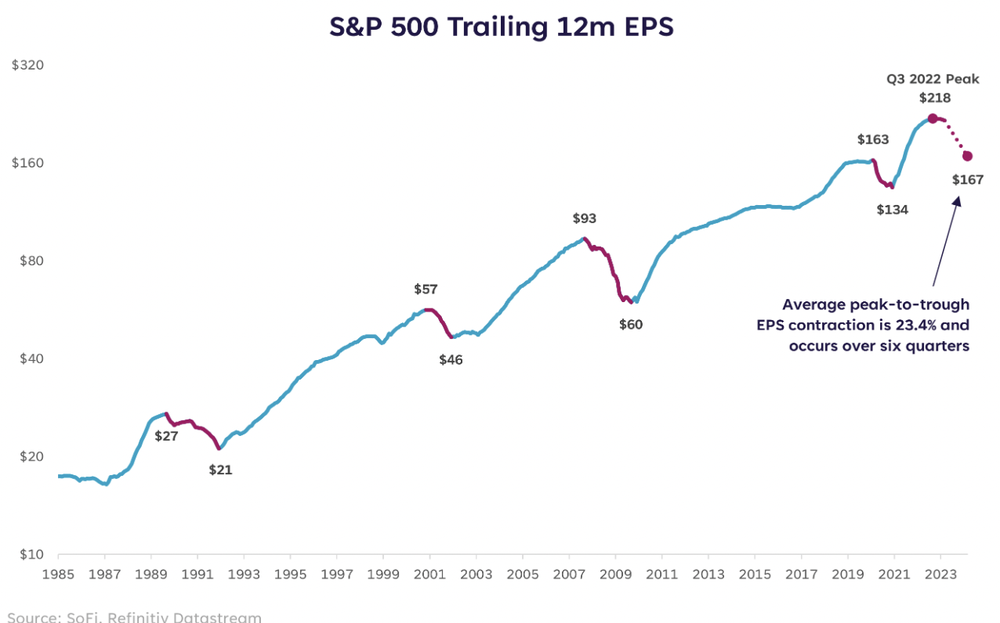

One of the important data sets to watch is trailing earnings on the S&P, where we can track the cycle peak in earnings per share (EPS), and monitor each earnings season for how much of a slowdown is occuring. Additionally, it’s useful to keep in mind how much the average earnings contraction is during a recessionary period, which we’ve calculated as -23% from peak to trough.

Still too early to know how steep the decline in earnings could be, but it appears that the peak was reached in Q3 2022 at $218/share. If, and only if, EPS declines the average percentage, the chart above shows what that level would look like.

Although I think the wider profit margins and heavy cost cutting that has already occurred in the tech sector could prevent the drop in earnings from being that dramatic, I do think current estimates for 2023 earnings are still a bit too high. Especially given the economic environment and lack of movement in estimates after the recent banking stress.

We’ve Gotta Hold on, Ready or Not

Generally, the recipe for a true contraction phase in the business cycle includes a bear market (-20% or more peak to trough), an earnings recession, and an economic recession (two consecutive quarters of negative GDP growth). Typically they occur in that order, too.

It’s true that we already saw a bear market in the S&P 500 and the Nasdaq in 2022, but that doesn’t mean the pullbacks are over. In fact, I still believe we could see a pullback that results in a peak-to-trough decline in the S&P of 30% or more (note: the peak I’m referring to is 4,796 on January 3, 2022).

Since we’ll have the verdict on a possible earnings recession in less two months, that would tell me we’re ripe for a market pullback to begin sooner rather than later. Time will tell, but this earnings season is a crucial part of the equation that is about to start unfolding.

After many weeks of caution and finding opportunities in safe havens such as short-term Treasuries, gold, money market funds, and defensive equity sectors, I’m still holding that line, but I do feel like the movements we’ve been preparing for are drawing nearer.

Learn More:

This article originally appeared on SoFi.com and was syndicated by MediaFeed.org.

Please understand that this information provided is general in nature and shouldn’t be construed as a recommendation or solicitation of any products offered by SoFi’s affiliates and subsidiaries. In addition, this information is by no means meant to provide investment or financial advice, nor is it intended to serve as the basis for any investment decision or recommendation to buy or sell any asset. Keep in mind that investing involves risk, and past performance of an asset never guarantees future results or returns. It’s important for investors to consider their specific financial needs, goals, and risk profile before making an investment decision.

The information and analysis provided through hyperlinks to third party websites, while believed to be accurate, cannot be guaranteed by SoFi. These links are provided for informational purposes and should not be viewed as an endorsement. No brands or products mentioned are affiliated with SoFi, nor do they endorse or sponsor this content.

Communication of SoFi Wealth LLC an SEC Registered Investment Advisor

SoFi isn’t recommending and is not affiliated with the brands or companies displayed. Brands displayed neither endorse or sponsor this article. Third party trademarks and service marks referenced are property of their respective owners.

Communication of SoFi Wealth LLC an SEC Registered Investment Adviser. Information about SoFi Wealth’s advisory operations, services, and fees is set forth in SoFi Wealth’s current Form ADV Part 2 (Brochure), a copy of which is available upon request and at www.adviserinfo.sec.gov. Liz Young is a Registered Representative of SoFi Securities and Investment Advisor Representative of SoFi Wealth. Her ADV 2B is available at www.sofi.com/legal/adv.

More from MediaFeed:

How do I know when it’s time to pull money out of the stock market?

When the stock market drops, some investors get antsy. Watching the market decline in real-time can be stressful. It may even seem like invested money is heading towards zero.

During drops in the market, it can be easy for investors to think that their hard-earned money is going up in smoke. A worried investor might reason that it’s better to lose a little now than to forfeit more later by sticking with the markets.

But, is it always a good idea to pull money out of the stock market when there’s a drop? There’s no one-size-fits-all answer for investors, here. (Investors in their 20s, for instance, may likely have different risk tolerance and timelines than those approaching retirement).

For younger investors, time in the market might beat timing the stock market. Here’s an overview of factors investors might think about when deciding whether to keep money in the stock market:

Maximusnd / istockphoto

When markets experience a sharp decline, certain investors might feel tempted to give in to FUD (fear, uncertainty, doubt) — aka, panic selling. Investors could assume that by selling now, they’re shielding themselves (and their money) from further losses down the road.

This logic, however, presumes that the market will continue to go down, which — given the volatility of prices and the impossibility of knowing the future — may or may not be the case.

Focusing on temporary declines might compel some investors to make hasty decisions that they may later come to regret. In the investment world, investors who rush to sell due to price changes are said to have “weak hands.” In a shaky market, having weak hands could lead to further losses.

After all, over time, markets tend to correct. Likewise, when the market is moving upwards, investors can sometimes fall victim to what’s known as FOMO (fear of missing out) — buying under the assumption that today’s growth is a sign of tomorrow’s continued boom.

An emotion-guided approach to the stock market, whether it’s the offloading or buying up of stocks, can stem from an attempt to predict the short-term movements in the market. This approach is called “timing the market.”

fizkes / istockphoto

Answering the question of “Should I pull my money out of the stock market?” will likely vary depending on an investor’s time horizon — or, the length of time they aim to hold an investment before selling. Popular opinion generally holds that time in the market can beat timing the stock market.

Put another way, keeping money in the market for a long period of time can help cut the risk of short-term dips or declines in stock pricing. Waiting it out, for some investors, could be a sound strategy.

Many experienced investors believe that it’s impossible to predict something as volatile and unruly as the stock market. Indeed, some investors think that trying to time the market creates higher risks and fewer rewards than keeping money invested in the market for longer periods of time.

An investor’s time horizon may play a significant role in determining whether or not they might want to get out of the stock market. Generally, the longer a period of time an investor has to ride out the market, the less they may want to fret about their portfolio during upheaval.

Compare, for instance, the scenario of a 25 year old who has decades to make back short-term losses with that of someone who’s about to retire and needs to begin cashing out their investment accounts.

Investors who plan on being in the market for a long time, such as young people investing for retirement, may simply want to wait it out. While there is no guarantee that markets will correct in a way that benefits each and every investor, even the sharpest market downturns, with time, can rebound.

Younger investors with long-term investment goals might want to keep their money in stocks during major market routs. But, what other options are available to investors besides pulling their money out of the stock market?

William_Potter / istockphoto

Some investors might want to stay in the stock market when it crashes, but others may opt to adjust where they’re alloting their investments. Here’s an overview of some alternatives to getting out of the stock market:

DepositPhotos.com

Investors could choose to rotate some of their investments into safe haven assets (like, gold). By rebalancing a portfolio so less holdings are impacted by market volatility, investors might reduce the risk of loss.

Reassessing where to allocate one’s asset is no simple task and, if done too rashly, could lead to losses in the long run. So, it may be helpful for investors to speak with a credible financial planner before making a big investment change that’s driven by the news of the day.

DepositPhotos.com

Instead of needing to shift investments into safe haven assets, like precious metals, some investors prefer to cultivate a well-diversified portfolio from the start.

In this case, there’d be less need to rotate funds towards “safer” investments during a decline, as the portfolio would already be split between assets with stability and risk.

Gold, silver and bonds are often thought of as some of the safe havens that investors first flock to during times of uncertainty.

During market turmoil, a significant portion of investors generally move to safe havens (also known as “risk-off” assets). Evidence of this comes from the fact that a market downturn itself is defined by a selloff in riskier assets (like stocks), which can then bring about a rise in value of risk-off assets. In the initial shock, however, sometimes all asset classes see a sharp decline — as people worried about their finances scramble for liquid cash.

One example of this turn to risk-off assets was seen in summer 2020, when the price of spot gold as measured against U.S. dollars had reached new record highs and silver had its best week in 40 years.

During this particular market, bond yields saw several new lows (the price of a bond is the inverse of its yield, meaning the lower the yield, the higher the price).

Investors who managed to shift to these safer havens at the beginning of the crisis may have begun to profit from market uncertainty. And, once trends have been strongly confirmed by the market, it can often create a self-reinforcing feedback loop.

As more investors notice a trend away from more volatile stocks, some will interpret it as a sign of further uncertainty, which could then create more rotation into presumably safer assets.

jansucko / istockphoto

Reinvesting dividends may also lead the long-term investor’s portfolio to continue growing at a steady pace, even when share prices decline temporarily. Knowing where and when to reinvest earnings is another factor investors may want to chew on when deciding which strategy to adopt.

(Any dividend-yielding stocks an investor holds must be owned on or before the ex-dividend date. Otherwise, the dividend won’t be credited to the investor’s account. So, if an investor decides to get out of the stock market, they may miss out on dividend payments.)

Sometimes, astute investors also choose to rebalance their portfolio in a downturn by buying new stocks. It’s difficult, though not impossible, to profit from novel trends that can come forth during a crisis.

Acquiring assets that benefit from the circumstances of a market crash may lead to gains. It’s worth noting that this investment strategy doesn’t involve pulling money out of the stock market — it just means selling some stocks to buy others.

For example, during the initial shock of the 2020 crisis, many stocks suffered steep declines. But, there were some that outperformed the market due to recent market shifts. Stocks for companies that specialize in work-from-home software, like those in the video conferencing space, saw an increase in value.

Cybersecurity stocks, similarly, held up due to increased market demand in that sector. Home workout equipment, like exercise bikes, became in high demand, leading related stocks higher. Some remote-based healthcare companies saw share prices rise.

And of course, pharmaceutical companies promising a cure for the pandemic virus saw outstanding rallies, as people believed that a successful product might bring an end to the crisis.

Some experienced investors noticed and took advantage of these trends, but for newer investors or those with low risk tolerance, attempting this strategy might not be a desirable option.

Sergii Zyskо / istockphoto

During downturns, it could be worthwhile for investors to examine asset allocations — or, the amount of money an investor holds in each asset.

If an investor holds stocks in industries that have been struggling and may continue to struggle due to floundering demand (think restaurants, retail, or oil in 2020), they may opt to sell some of the stocks that are declining in value.

Even if such holdings get sold at a loss, the investor could then put money earned from the sale of these stocks towards safe haven assets — potentially gaining back their recent losses.

utah778 / istockphoto

Cash can be an added asset, too. Naturally, the value of cash is shaped by things like inflation, so its purchase power can swing up and down. Still, there are advantages to stockpiling some cash. Money invested in other assets, after all, is — by definition —t ied up in that asset. That money is not immediately liquid.

Cash, on other other hand, could be set aside in a savings account or in an emergency fund — unencumbered by a specific investment. Here are some potential benefits to cash holdings:

First, on a psychological level, an investor who knows they have cash on hand may be less prone to feel they’re at risk of losing it all (when stocks fluctuate or flail).

A secondary benefit of cash involves having some “dry powder”— or, money on hand that could be used to buy additional stocks if the market keeps dipping. In investing, it can pay to a “contrarian,” running against the crowd. In other words, when others are selling (aka being fearful), a savvy investor might want to buy.

Pixabay

Attempting to time the market (when there’s no crystal ball) can be risky and stressful. For younger investors, keeping money in the stock market may carry advantages over time. One approach to investing is to establish long-term investment goals and then strive to stay the course — even when facing market headwinds.

Always, when it comes to investing in the stock market, there’s no guarantee of increasing returns. So, individual investors will want to examine their personal economic needs and short-term and future financial goals before deciding if or how to invest.

While managing money during a market downturn might seem tricky, getting started with investing doesn’t need to be stressful.

Learn more:

This article originally appeared on SoFi.com and was syndicated by MediaFeed.org.

SoFi Invest

The information provided is not meant to provide investment or financial advice. Investment decisions should be based on an individual’s specific financial needs, goals and risk profile. SoFi can’t guarantee future financial performance. Advisory services offered through SoFi Wealth, LLC. SoFi Securities, LLC, member FINRA/SIPC. The umbrella term “SoFi Invest” refers to the three investment and trading platforms operated by Social Finance, Inc. and its affiliates (described below). Individual customer accounts may be subject to the terms applicable to one or more of the platforms below.

External Websites: The information and analysis provided through hyperlinks to third party websites, while believed to be accurate, cannot be guaranteed by SoFi. Links are provided for informational purposes and should not be viewed as an endorsement.

Investment Risk: Diversification can help reduce some investment risk. It cannot guarantee profit, or fully protect in a down market.

Crypto: Bitcoin and other cryptocurrencies aren’t endorsed or guaranteed by any government, are volatile, and involve a high degree of risk. Consumer protection and securities laws don’t regulate cryptocurrencies to the same degree as traditional brokerage and investment products. Research and knowledge are essential prerequisites before engaging with any cryptocurrency. US regulators, including FINRA, the SEC, and the CFPB, have issued public advisories concerning digital asset risk. Cryptocurrency purchases should not be made with funds drawn from financial products including student loans, personal loans, mortgage refinancing, savings, retirement funds or traditional investments.

DepositPhotos.com

Featured Image Credit: gorodenkoff/ iStock.