Slow Your Roll

It seems that every Fed meeting this year has felt like the most important Fed meeting. Today was no exception (although we’ll likely say the same in December). The Federal Open Market Committee (FOMC) raised their target rate by another 0.75% to an upper bound of 4.00%. The Fed Funds Rate hasn’t been at these levels since 2008.

Many market participants were looking for an indication that the Fed would slow its pace of hikes in subsequent meetings, and markets found some satisfaction in the statement that “…the committee will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments.”

Until Jerome Powell started speaking and reiterated that ongoing increases will likely be needed, and that they want to get to a level that is “sufficiently restrictive to return inflation to 2% over time.”

Realistically, I don’t think much has changed in their stance. If they had said they were nearing the end of the hiking cycle, I would’ve been concerned.

Inflation is not taken care of yet. The Fed’s job is to control prices and maintain employment, not to avoid recessions. We still have a Federal Reserve that is laser focused on solving the inflation problem regardless of the pain their actions may inflict on other parts of the economy.

If inflation stays too high, it would likely throw us into a recession on its own due to the pressure it puts on consumers and businesses. We can scream and shout as loud as we want about how we got to this predicament — and whose fault it is — it doesn’t really matter. We need to get out of it one way or another.

The Fed may slow the pace of hikes, but make no mistake: they’re not stopping.

BeLaboring the Point

One of the notable takeaways from today was that the Fed is acknowledging there is a chance the terminal rate will be higher than their expectations from just a couple months ago. As of this writing, the market was pricing in a terminal rate of 5.0% in May 2023, which is up from 4.75% in September.

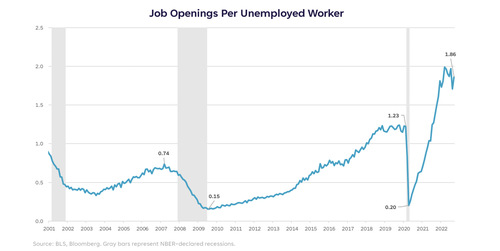

One reason the terminal rate expectations continue to rise is because of the stubbornly tight labor market. The ratio of open positions to unemployed workers went back up in September to 1.86.

It’s natural to think a strong labor market is good. And it is good…for workers. It’s not good for companies facing higher wage costs and a shortage of employees. Since wage growth is stickier than other inflation components, it’s likely to be with us for a while, and likely to pressure corporate margins as a result. When margins get pressured enough and companies have cut costs everywhere they can…they start laying off workers.

A labor market this tight has a buffer to soften further before it becomes concerning, so for now it’s just more confirmation that hikes can continue and that the level of rates can remain elevated for some time.

In my opinion, the rally we’ve experienced since early October is under threat as the market comes to grips (again) with the fact that this is a decidedly hawkish Fed. And a Fed that would rather go too far than not far enough.

Tight is Right

That all said, we’ve done some serious work on the tightening front. And we know there’s a lag between policy moves and economic effects. Financial conditions have tightened considerably since the start of this year, and this is probably one chart the Fed likes the looks of right now.

As tightening works its way through the real economy, there’s good reason to expect further softening in demand, housing, labor, manufacturing, and in turn, inflation. We can also comfortably expect that those forces are currently at play — we just haven’t seen them in the data yet.

Call me “Lower Liz,” but it’s possible that this meeting was a catalyst for giving back some (or all) of the October rally. That wouldn’t be the end of the world because it would mark the end of another bear market bounce. The more of them we put in the rearview, the closer we are to the real bounce. In order to know when that real bounce is taking shape, I think we still need to see meaningful softening in labor, and I’d expect that to show its face before the end of the year.

Learn More:

This article originally appeared on SoFi.com and was syndicated by MediaFeed.org.

Please understand that this information provided is general in nature and shouldn’t be construed as a recommendation or solicitation of any products offered by SoFi’s affiliates and subsidiaries. In addition, this information is by no means meant to provide investment or financial advice, nor is it intended to serve as the basis for any investment decision or recommendation to buy or sell any asset. Keep in mind that investing involves risk, and past performance of an asset never guarantees future results or returns. It’s important for investors to consider their specific financial needs, goals, and risk profile before making an investment decision.

The information and analysis provided through hyperlinks to third party websites, while believed to be accurate, cannot be guaranteed by SoFi. These links are provided for informational purposes and should not be viewed as an endorsement. No brands or products mentioned are affiliated with SoFi, nor do they endorse or sponsor this content.

Communication of SoFi Wealth LLC an SEC Registered Investment Advisor

SoFi isn’t recommending and is not affiliated with the brands or companies displayed. Brands displayed neither endorse or sponsor this article. Third party trademarks and service marks referenced are property of their respective owners.

Communication of SoFi Wealth LLC an SEC Registered Investment Adviser. Information about SoFi Wealth’s advisory operations, services, and fees is set forth in SoFi Wealth’s current Form ADV Part 2 (Brochure), a copy of which is available upon request and at adviserinfo. Liz Young is a Registered Representative of SoFi Securities and Investment Advisor Representative of SoFi Wealth. Her ADV 2B is available at sofi.

More from MediaFeed:

Your complete guide to surviving a recession

Recession warnings are everywhere. With interest rates rising, inflation hitting the highest levels in 40 years, and stocks plunging into bear market territory, most people are more than a little worried. Let’s face it, many of us are feeling the pain of the current economy every time we fill the tank, stock the fridge, or check our 401(k) balance.

But the reality is that, whether or not they fit the technical definition of a recession, these types of downturns are a normal (albeit painful) reality of economic cycles. When they happen, one of the most productive responses is to turn worry into action. Building a fortress around your finances can protect against tough times and put you in a better position when the economy bounces back.

So exactly what to do in a recession? These five steps can help you prepare for any type of economic slowdown, now and in the future.

Recommended: What is a Recession and Why Do They Happen?

DepositPhotos.com

Dramatic price increases across the board have already forced many consumers to cut back on their budget for basic living expenses such as groceries and travel. Now is also a good time to review bank and credit card statements to find other cost-cutting opportunities.

Maybe those streaming services that were a lifeline during COVID aren’t necessary any more. Or, it might make sense to put off some of those home improvements you were considering, keeping the equity in your home intact should you need it during the slowdown.

Revamping your budget can help you handle today’s higher prices and also help free up a few dollars for steps 2 and 3 below.

Extreme Media / istockphoto

Hard as it may be to find extra cash right now, it’s important to make sure you are putting something aside for unexpected expenses. Don’t feel overwhelmed by the advice saying you should aim for three to six months’ worth of living expenses. Saving that much right now may sound more discouraging than helpful, especially for people who saw their emergency funds dwindle during the pandemic. Keep in mind, anything you can save (even $25 a month) is good, and even small weekly deposits add up over time. Whatever you can afford, know that it’s worthwhile to prioritize emergency funds.

With emergency savings, you may get to take advantage of one of the few benefits of rising interest rates. Savings accounts may begin to pay more interest soon. What kind of savings account should you get? You might look for high-interest accounts offered by online banks as they often pay more than bricks-and-mortar financial institutions. Your goal, of course, is to get the best rate. If you are employed full time, check with your benefits department to see if any emergency savings programs are available through your work. Having some cash in the bank can be a key step when you are wondering how to handle a recession. It can be a hugely helpful safety net.

Rawpixel / istockphoto

Here’s the bad news about higher interest rates. The national average credit card rate rose above 17% for the first time in more than two years, according to a recent weekly rate report. The jump happened after the Federal Reserve increased interest rates. More rate hikes are expected throughout the year.

Check rates on all of your credit cards and other debts. Any variable rates may have already gone up. Next step? Pay as much as you can on your highest interest rate balances first to whittle down that debt; it’s the kind that can unfortunately snowball during tough economic times.

You might also look into balance transfer credit card offers. They can offer a period of no or low interest, during which you can pay down that debt. Another option is finding out how debt consolidation programs work.

Depositphotos

The current economic turmoil hits just as federal student loan repayments are set to begin again in September, after a more than two-year reprieve during the COVID-19 pandemic. Another extension is expected (and hoped for by many) but has not been announced. Nonetheless, payments are likely to start again sometime.

If you’ve taken advantage of the pause, this is the time to get ready for repayment, whenever it comes. Contact the servicers of your federal student loans to make sure you know the monthly payment due date and other details that you may have forgotten or that may have changed during the pause.

If you’re worried about affording repayments, look into alternatives. Forbearance, for example, allows a qualified borrower to suspend federal student debt payments for a period of time, although interest continues to accrue. Government-sponsored income-driven repayment programs are another option. They cap monthly loan payments at a percentage of what is defined as discretionary income. Still other borrowers may find refinancing student loans through a private lender can be an affordable option. It can be worthwhile to do the research to find out what exactly your options are to stay current on your loans.

fizkes / istockphoto

When it comes to your long-term investments such as 401(k)s and other retirement accounts, the key to surviving a down market is simple: Hold tight. Nothing good is likely to happen when you sell in a panic. Not only do you risk selling at a loss, but you’ll miss out when the market rebounds, as it inevitably does.

Take a look at the most recent downturn. The Standard & Poor’s stock market index plunged almost 31% in March 2020 when Covid first hit. Then the index almost doubled just a year later. Investors who sold in a panic didn’t see any of those record-breaking returns.

If rising expenses are making it impossible for you to keep up with 401(k) contributions, you may want to try to deposit the minimum necessary to get any matching funds your employer offers. That’s free money, and you don’t want to miss out.

Also try to avoid making any withdrawals from your retirement accounts. In most cases, if you’re younger than 59 ½, you’ll pay a 10% penalty plus taxes.

Even more important, a chunk of your money won’t be there to see the growth in your long-term savings account when the market rebounds.

SARINYAPINNGAM/iStock

Most recessions include high unemployment and mass layoffs. This slowdown is a little different. So far, the unusually strong labor market has protected the U.S. from rising unemployment, contributing to the one bright spot in the U.S. economy. Wages have also increased, but generally not enough to offset the current record inflation.

Economists warn the strong employment market may not last. That’s something to be ready for, especially if you work in an industry that typically suffers downturns in a recession. And employees who may be counting on finding a higher-paying position in this strong job market may find their window for doing so is closing. What’s more, in a worst-case scenario, some people could find themselves figuring out how to apply for unemployment.

Reducing debt and building emergency savings, as mentioned above, are two important steps you can take to prepare for the financial shock of a layoff. In addition, this is a good time to work to recession-proof your career: Update your resume, boost your network, and get the extra education, skills or training you may need to protect your livelihood.

Check out our Recession Survival Guide to learn more about living through a recession.

DepositPhotos.com

Economic downturns are never pleasant and often painful. But with some thoughtful planning and the steps outlined above, you can protect your finances and better position yourself when the economy bounces back.

Learn More:

This article originally appeared on SoFi.com and was syndicated by MediaFeed.org.

SoFi Checking and Savings is offered through SoFi Bank, N.A. 2022 SoFi Bank, N.A. All rights reserved. Member FDIC. Equal Housing Lender.

SoFi members with direct deposit can earn up to 2.00% annual percentage yield (APY) interest on all account balances in their Checking and Savings accounts (including Vaults). Members without direct deposit will earn 1.00% APY on all account balances in Checking and Savings (including Vaults). Interest rates are variable and subject to change at any time. Rate of 2.00% APY is current as of 08/12/2022. Additional information can be found here.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

SoFi’s Relay tool offers users the ability to connect both in-house accounts and external accounts using Plaid, Inc’s service. When you use the service to connect an account, you authorize SoFi to obtain account information from any external accounts as set forth in SoFi’s Terms of Use. SoFi assumes no responsibility for the timeliness, accuracy, deletion, non-delivery or failure to store any user data, loss of user data, communications, or personalization settings. You shall confirm the accuracy of Plaid data through sources independent of SoFi. The credit score provided to you is a Vantage Score based on TransUnion™ (the “Processing Agent”) data.

External Websites: The information and analysis provided through hyperlinks to third-party websites, while believed to be accurate, cannot be guaranteed by SoFi. Links are provided for informational purposes and should not be viewed as an endorsement.

nicoletaionescu / istockphoto

DepositPhotos.com

Featured Image Credit: DepositPhotos.com.