Loan modification is a change to the terms and conditions of an existing loan agreement. Borrowers may request loan modifications if they are experiencing financial difficulties, and lenders may grant certain concessions to help accommodate borrowers facing economic hardship.

A loan modification can reduce a borrower’s monthly payment if the lender agrees to reduce the interest rate or extend the term of the loan. Lenders can also forgive principal and past due interest under a modified loan agreement. Below we describe how loan modifications work.

Related: What is a signature loan?

How Do Loan Modifications Work?

The way loan modifications work is a borrower and lender agree to change the terms and conditions of an existing loan agreement. A lender has no obligation to make any loan modifications, but a lender may offer certain concessions if a borrower is facing economic hardship.

Loan modifications can reduce a borrower’s monthly payment by giving the borrower a lower interest rate, a longer term of repayment, or both. Lenders in some cases may offer special concessions to cure a borrower’s default on personal loan obligations.

Lenders could report a delinquent account as current to the credit reporting agencies. Lenders could also grant borrowers a deferment that extends the term of the loan without imposing late fees. In some cases, lenders may forgive a portion of a borrower’s unpaid principal, which could have tax consequences if the lender forgave or canceled $600 of debt or more.

Reasons for a Loan Modification

Below we highlight common reasons for a loan modification:

Default on a Personal Loan

As mentioned earlier, lenders for a personal loan may offer concessions to cure a borrower’s default. If borrowers cannot afford their existing monthly payment but have the income to afford a lower payment, both parties in that case may agree to a loan modification to reduce the monthly payment.

Lenders in some cases may prefer to cure a default with an amicable loan modification rather than suing delinquent borrowers for breach of contract. Loans for personal use can help you consolidate debt, but failing to repay a debt consolidation loan can lead to severe delinquency. A loan modification can cure defaults before they enter the severe stage of prolonged delinquency.

Hardship

A borrower experiencing financial hardship may contact their lender and ask for temporary or permanent relief. The lender and borrower in that case could agree to new terms and conditions under a loan modification that may reduce the borrower’s monthly payment.

A borrower facing temporary hardship may request additional time to make a required payment. Lenders in that case could grant a deferment. A deferment is a postponement on required payments that can help borrowers avoid late fees and having their accounts reported to a credit bureau as delinquent.

Can You Get a Personal Loan Modified?

You can get a personal loan modified if your lender is willing to make some concessions. As mentioned earlier, a lender has no obligation to make any loan modifications but may offer certain concessions if a borrower is facing economic hardship.

There are certain disadvantages and advantages of personal loans, including their potential for helping consumers build credit as a pro and their potential to carry high finance charges as a con. One of the modifications a lender may agree to is reducing the borrower’s interest rate.

How Often Do Loan Modifications Get Approved?

A lender may offer two loan modifications in a rolling 12-month period for borrowers facing financial hardship. Such modifications could consist of account deferments. A deferment by itself doesn’t reduce the monthly payment, but a deferment gives borrowers more time to make required payments without facing late fees.

A deferment is the most basic loan modification a lender can offer to an existing loan agreement. Another loan modification lenders may consider is reducing the borrower’s interest rate. It’s common for loan modifications to get approved if a borrower is facing temporary hardship. This can happen any year, especially during recessions and global pandemics.

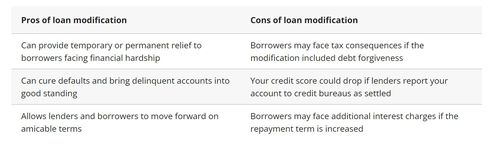

Loan Modification: Pros & Cons

Here are some pros and cons of loan modification:

Loan Modification Pros

Let’s review loan modification pros:

Amicable Agreement

Loan modification is generally an amicable agreement between the borrower and lender. The modification can provide borrowers with instant relief and allows lenders to retain customers through thick and thin.

Faster Processing

Loan modification is similar to refinancing, but modifying the terms on your existing account may offer faster relief than refinancing. That’s because loan modification is simply changing the terms of your existing loan while refinancing involves more steps of replacing the original loan with a new account.

Default Cure

Delinquent borrowers can negotiate loan modifications to cure a default. Borrowers who default on a personal loan could face costly legal action and a severe negative impact to their credit scores for failing to make required payments. Loan modification can serve as a remedy that gives delinquent borrowers a second chance to move forward in good standing.

Loan Modification Cons

Let’s review loan modification cons:

Credit Score

Your credit score could drop if lenders report your modified loan account to credit bureaus as being settled for less than the amount you originally owed. A lower credit score can make it harder for you to qualify for new credit and better terms for you.

No Cash Out Option

Loan modification features no cash out option, but homeowners with an existing mortgage can apply for a cash-out refinance loan as an alternative to loan modification. Loan modification doesn’t take advantage of the available equity homeowners may have in their homes, while a cash-out refinance loan allows homeowners to trade equity for cash.

Tax Consequences

Lenders may offer debt forgiveness as part of a loan modification agreement that provides relief to delinquent borrowers, but the IRS may consider that taxable income. As mentioned earlier, borrowers may face tax consequences if the lender forgave or canceled $600 or more of the borrower’s outstanding loan debt.

Is a Loan Modification Bad for Your Credit?

Loan modification may be good for your credit if it prevents a default on your account. Failing to make a required loan payment may constitute a default, and nonpayment delinquencies of 30 days or more could severely damage your credit.

Loan modification can also be bad for your credit if the modification forgives a portion of your debt. As mentioned above, your credit score could drop if lenders report your modified loan account to credit bureaus as being settled for less than what you owed.

The Takeaway

Financial hardship is not always predictable, but borrowing money on the best terms for you could be in your best interests. Borrowers in some cases may consider modifying the terms and conditions of their preexisting loan agreements if the financial responsibility becomes too difficult to bear.

Learn More:

This article originally appeared on LanternCredit.com and was syndicated by MediaFeed.org.

Lantern by SoFi:

This Lantern website is owned by SoFi Lending Corp., a lender licensed by the Department of Financial Protection and Innovation under the California Financing Law, license number 6054612; NMLS number 1121636. (www.nmlsconsumeraccess.org)

All rates, fees, and terms are presented without guarantee and are subject to change pursuant to each provider’s discretion. There is no guarantee you will be approved or qualify for the advertised rates, fees, or terms presented. The actual terms you may receive depends on the things like benefits requested, your credit score, usage, history and other factors.

*Check your rate: To check the rates and terms you qualify for, Lantern and/or its network lenders conducts a soft credit pull that will not affect your credit score. However, if you choose a product and continue your application, the lender(s) you choose will request your full credit report from one or more consumer reporting agencies, which is considered a hard credit pull and may affect your credit.

All loan terms, including interest rate, and Annual Percentage Rate (APR), and monthly payments shown on this website are from lenders and are estimates based upon the limited information you provided and are for information purposes only. Estimated APR includes all applicable fees as required under the Truth in Lending Act. The actual loan terms you receive, including APR, will depend on the lender you select, their underwriting criteria, and your personal financial factors. The loan terms and rates presented are provided by the lenders and not by SoFi Lending Corp. or Lantern. Please review each lender’s Terms and Conditions for additional details.

Many factors affect your credit scores and the interest rates you may receive. SoFi is not a Credit Repair Organization as defined under federal or state law, including the Credit Repair Organizations Act. SoFi does not provide “credit repair” services or advice or assistance regarding “rebuilding” or “improving” your credit record, credit history, or credit rating. For details, see the FTC’s website on credit (https://consumer.ftc.gov/credit-loans-debt)

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

Personal Loan:

SoFi Lending Corp. (“SoFi”) operates this Personal Loan product in cooperation with Even Financial Corp. (“Even”). If you submit a loan inquiry, SoFi will deliver your information to Even, and Even will deliver to its network of lenders/partners to review to determine if you are eligible for pre-qualified or pre-approved offers. The lenders/partners receiving your information will also obtain your credit information from a credit reporting agency. If you meet one or more lender’s and/or partner’s conditions for eligibility, pre-qualified and pre-approved offers from one or more lenders/partners will be presented to you here on the Lantern website. More information about Even, the process, and its lenders/partners is described on the loan inquiry form you will reach by visiting our Personal Loans page as well as our Student Loan Refinance page. Click to learn more about Even’s Licenses and Disclosures, Terms of Service, and Privacy Policy.

Personal loan offers provided to customers on Lantern do not exceed 35.99% APR. An example of total amount paid on a personal loan of $10,000 for a term of 36 months at a rate of 10% would be equivalent to $11,616.12 over the 36 month life of the loan.

Student Loan Refinance:

SoFi Lending Corp. (“SoFi”) operates this Student Loan Refinance product in cooperation with Even Financial Corp. (“Even”). If you submit a loan inquiry, SoFi will deliver your information to Even, and Even will deliver to its network of lenders/partners to review to determine if you are eligible for pre-qualified or pre-approved offers. The lender’s receiving your information will also obtain your credit information from a credit reporting agency. If you meet one or more lender’s and/or partner’s conditions for eligibility, pre-qualified and pre-approved offers from one or more lenders/partners will be presented to you here on the Lantern website. More information about Even, the process, and its lenders/partners is described on the loan inquiry form you will reach by visiting our Personal Loans page as well as our Student Loan Refinance page. Click to learn more about Even’s Licenses and Disclosures, Terms of Service, and Privacy Policy.

Student loan refinance loans offered through Lantern are private loans and do not have the debt forgiveness or repayment options that the federal loan program offers, or that may become available, including Income Based Repayment or Income Contingent Repayment or Pay as you Earn (PAYE).

Notice: Recent legislative changes have suspended all federal student loan payments and waived interest charges on federally held loans until 08/31/22. Please carefully consider these changes before refinancing federally held loans, as in doing so you will no longer qualify for these changes or other future benefits applicable to federally held loans.

Auto Loan Refinance:

Automobile refinancing loan information presented on this Lantern website is from Caribou. Auto loan refinance information presented on this Lantern site is indicative and subject to you fulfilling the lender’s requirements, including: you must meet the lender’s credit standards, the loan amount must be at least $10,000, and the vehicle is no more than 10 years old with odometer reading of no more than 125,000 miles. Loan rates and terms as presented on this Lantern site are subject to change when you reach the lender and may depend on your creditworthiness. Additional terms and conditions may apply and all terms may vary by your state of residence.

Secured Lending Disclosure:

Terms, conditions, state restrictions, and minimum loan amounts apply. Before you apply for a secured loan, we encourage you to carefully consider whether this loan type is the right choice for you. If you can’t make your payments on a secured personal loan, you could end up losing the assets you provided for collateral. Not all applicants will qualify for larger loan amounts or most favorable loan terms. Loan approval and actual loan terms depend on the ability to meet underwriting requirements (including, but not limited to, a responsible credit history, sufficient income after monthly expenses, and availability of collateral) that will vary by lender.

Life Insurance:

Information about insurance is provided on Lantern by SoFi Life Insurance Agency, LLC. Click here to view our licenses.

More from MediaFeed:

What happens to your personal loans when you die?

What happens to personal loans when the borrower dies? This answer may not be as straightforward as you might think.

Here’s some context. In this post, the term “personal loans” goes beyond the type of installment loan known as a “personal loan” and encompasses loans taken out by a person or people rather than by businesses. It is a complex subject with laws varying by state.

According to the Federal Trade Commission, debts do not in general go away because the debt holder has died. Typically, the debts are paid from the estate of the deceased person.

An estate includes the person’s real estate, cash, financial investments, vehicles and other assets. If there isn’t enough money in the estate, the debts often go unpaid although there are exceptions where someone else is personally responsible for the debt.

Related: Can you use your spouse’s income for a personal loan?

Ridofranz

If someone has a will, it should list an executor. The executor is responsible for paying the deceased person’s debts out of the assets in their estate among other duties. If there isn’t a will, the court may appoint someone as executor or state law may contain a process in which someone becomes responsible for debt settling.

DepositPhotos.com

State laws vary on how debt payments must be prioritized. Most commonly, funeral expenses are first, followed by estate administration costs and then taxes and medical bills. It’s important to seek guidance about state laws where the deceased person lived.

DepositPhotos.com

In community property states, a spouse may be personally responsible for outstanding debts and, in some states, other laws exist that make a spouse responsible for certain types of debts, such as healthcare expenses.

GaudiLab / istockphoto

People who can inherit debt include the following.

DepositPhotos.com

If you cosigned for someone’s debt and that person dies, you are typically responsible for that debt. This is not usually the case if you’re an authorized user on an account, such as a credit card.

If a debt collector tells you that you were a cosigner, but you believe that you were an authorized user only, the Consumer Financial Protection Bureau notes that you can ask the debt collector for evidence.

istockphoto/demaerre

The situation for jointly held debt owners is similar to that for cosigners. If you were on a joint account with someone who passed away, you remain an account holder and will likely be responsible for debt payments.

DepositPhotos.com

If you were in a position where you were legally responsible for handling the debt, such as an estate’s executor and you didn’t follow proper procedures, you might find yourself legally obligated to pay the debt.

sabthai / istockphoto

As noted, spouses living in community property states may be required to pay off a deceased spouse’s debts through commonly held assets. Community property states include Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington and Wisconsin—and Alaska, if spouses chose this method of property owning.

fizkes / istockphoto

?")

The type of debt can play a role in how it’s handled. Loan types include the following.

DepositPhotos.com

Cosigners and joint credit card holders will almost certainly be held responsible for credit card debt. If the deceased person had an individual account, then it would largely depend upon whether they lived in a community property state or not.

In a community property state, credit card debt is considered to be jointly held. In common law property states, the debt shouldn’t typically pass on to someone else.

kitzcorner // istockphoto

First, some context: Mortgages typically have a due on sale clause that means the loan must be paid in full before ownership can change hands; this isn’t applicable, though, if it’s transferred to an heir after a borrower’s death. (As with other kinds of debt, cosigners and co-borrowers would still owe the debt.)

If someone else inherits the house and is not a cosigner or co-borrower, then federal law allows the beneficiary to take over the mortgage—and the mortgage servicer must allow that, even if the person would not typically qualify for that mortgage loan.

DepositPhotos.com

If someone inherits a home where there is a balance on a home equity loan, that debt is typically inherited, as well. If multiple heirs each inherit a share of the home, the situation becomes more complicated and you may want to get legal advice, especially if there is disagreement among heirs about how to proceed.

tommaso79/ iStock

In general, the deceased’s estate will pay for medical bills with exceptions, including when there is a cosigner or it’s a community property state. More than half of the states also have something called filial responsibility laws. This means that adult children can be held responsible for supporting their parents who can’t afford to support themselves. This law is rarely enforced but is worth noting.

jittawit.21/istockphoto

Car loans should generally be paid off by the estate. If there aren’t enough funds (and there’s no co-signer and it’s outside of a community property state), then the person inheriting the vehicle can make payments. If that doesn’t happen, then the lender may repossess the vehicle, sell it, and return any excess funds over the outstanding loan amount to the estate.

ipuwadol

Federal student loans will be discharged (considered paid in full) on the date of the borrower’s death. This applies to federal loans taken out by the student as well as parent PLUS loans taken out by a student’s parent.

Private lenders, however, are not legally required to cancel student loans upon death, so the executor should check the agreement to see what terms and conditions are.

fizkes / istockphoto

Personal loans also pass onto the estate where they can be paid through the deceased person’s assets. Cosigners/co-borrowers/spouses in a community property state can still be liable for that debt. (Here’s more information about what a personal loan is and the different types of personal loans.)

simonapilolla / istockphoto

In this section, we’re once again using the term “personal loans” to mean a non-business debt, which may or may not be a personal loan as the phrase is typically used.

If the debt is on record, meaning that there is a contract involved, the borrower would typically still owe the money. It would become an asset in the deceased person’s estate and there could still be consequences for the borrower if the debt is not paid.

roman dragunov / istockphoto

You can ask to see a copy of the contract, which would allow you to see the specifics of a loan agreement.

DepositPhotos.com

If a transfer of money occurs with the expectation of repayment, that is considered a loan that should be paid back. If there is a question about whether something was intended as a loan or as a gift, from a legal standpoint, there should be evidence that can be presented to show that it was a loan. If there isn’t enough evidence, the court will often consider it a gift.

DepositPhotos.com

Why get a personal loan? There are plenty of reasons to apply for a personal loan, including to pay legal expenses associated with estate planning. These loans can be unsecured or secured (collateralized loans). If it’s the latter, here’s what can be used as collateral for a personal loan. These installment loans come with a specified interest rate and term with payments calculated so that you pay it off in full during the loan’s term. If you find that you didn’t need as long of a term, here’s information about paying personal loans early.

Damir Khabirov / istockphoto

In general, when a borrower dies, the situation is handled through the person’s estate, with cosigners, co-borrowers and spouses in community property states having responsibility for most kinds of debts. When a lender dies, the borrower typically still owes the money. Individual situations can become quite complex, so it makes sense to reach out for legal help

.

You can compare rates for personal loans at Lantern by SoFi.

Learn More:

This article

originally appeared on LanternCredit.comand was

syndicated by MediaFeed.org.

The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

Lantern by SoFi:

This Lantern website is owned by SoFi Lending Corp., a lender licensed by the Department of Financial Protection and Innovation under the California Financing Law, license number 6054612; NMLS number 1121636. (www.nmlsconsumeraccess.org)

All rates, fees, and terms are presented without guarantee and are subject to change pursuant to each provider’s discretion. There is no guarantee you will be approved or qualify for the advertised rates, fees, or terms presented. The actual terms you may receive depends on the things like benefits requested, your credit score, usage, history and other factors.

*Check your rate: To check the rates and terms you qualify for, Lantern and/or its network lenders conducts a soft credit pull that will not affect your credit score. However, if you choose a product and continue your application, the lender(s) you choose will request your full credit report from one or more consumer reporting agencies, which is considered a hard credit pull and may affect your credit.

All loan terms, including interest rate, and Annual Percentage Rate (APR), and monthly payments shown on this website are from lenders and are estimates based upon the limited information you provided and are for information purposes only. Estimated APR includes all applicable fees as required under the Truth in Lending Act. The actual loan terms you receive, including APR, will depend on the lender you select, their underwriting criteria, and your personal financial factors. The loan terms and rates presented are provided by the lenders and not by SoFi Lending Corp. or Lantern. Please review each lender’s Terms and Conditions for additional details.

Many factors affect your credit scores and the interest rates you may receive. SoFi is not a Credit Repair Organization as defined under federal or state law, including the Credit Repair Organizations Act. SoFi does not provide “credit repair” services or advice or assistance regarding “rebuilding” or “improving” your credit record, credit history, or credit rating. For details, see the FTC’s website on credit (https://www.consumer.ftc.gov/topics/credit-and-loans)

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

Personal Loan:

SoFi Lending Corp. (“SoFi”) operates this Personal Loan product in cooperation with Even Financial Corp. (“Even”). If you submit a loan inquiry, SoFi will deliver your information to Even, and Even will deliver to its network of lenders/partners to review to determine if you are eligible for pre-qualified or pre-approved offers. The lenders/partners receiving your information will also obtain your credit information from a credit reporting agency. If you meet one or more lender’s and/or partner’s conditions for eligibility, pre-qualified and pre-approved offers from one or more lenders/partners will be presented to you here on the Lantern website. More information about Even, the process, and its lenders/partners is described on the loan inquiry form you will reach by visiting our Personal Loans page as well as our Student Loan Refinance page. Click to learn more about Even’s Licenses and Disclosures, Terms of Service, and Privacy Policy.

Personal loan offers provided to customers on Lantern do not exceed 35.99% APR. An example of total amount paid on a personal loan of $10,000 for a term of 36 months at a rate of 10% would be equivalent to $11,616.12 over the 36 month life of the loan.

Student Loan Refinance:

SoFi Lending Corp. (“SoFi”) operates this Student Loan Refinance product in cooperation with Even Financial Corp. (“Even”). If you submit a loan inquiry, SoFi will deliver your information to Even, and Even will deliver to its network of lenders/partners to review to determine if you are eligible for pre-qualified or pre-approved offers. The lender’s receiving your information will also obtain your credit information from a credit reporting agency. If you meet one or more lender’s and/or partner’s conditions for eligibility, pre-qualified and pre-approved offers from one or more lenders/partners will be presented to you here on the Lantern website. More information about Even, the process, and its lenders/partners is described on the loan inquiry form you will reach by visiting our Personal Loans page as well as our Student Loan Refinance page. Click to learn more about Even’s Licenses and Disclosures, Terms of Service, and Privacy Policy.

Student loan refinance loans offered through Lantern are private loans and do not have the debt forgiveness or repayment options that the federal loan program offers, or that may become available, including Income Based Repayment or Income Contingent Repayment or Pay as you Earn (PAYE).

Notice: Recent legislative changes have suspended all federal student loan payments and waived interest charges on federally held loans until 05/01/22. Please carefully consider these changes before refinancing federally held loans, as in doing so you will no longer qualify for these changes or other future benefits applicable to federally held loans.

Auto Loan Refinance:

Automobile refinancing loan information presented on this Lantern website is from Caribou. Auto loan refinance information presented on this Lantern site is indicative and subject to you fulfilling the lender’s requirements, including: you must meet the lender’s credit standards, the loan amount must be at least $10,000, and the vehicle is no more than 10 years old with odometer reading of no more than 125,000 miles. Loan rates and terms as presented on this Lantern site are subject to change when you reach the lender and may depend on your creditworthiness. Additional terms and conditions may apply and all terms may vary by your state of residence.

Secured Lending Disclosure:

Terms, conditions, state restrictions, and minimum loan amounts apply. Before you apply for a secured loan, we encourage you to carefully consider whether this loan type is the right choice for you. If you can’t make your payments on a secured personal loan, you could end up losing the assets you provided for collateral. Not all applicants will qualify for larger loan amounts or most favorable loan terms. Loan approval and actual loan terms depend on the ability to meet underwriting requirements (including, but not limited to, a responsible credit history, sufficient income after monthly expenses, and availability of collateral) that will vary by lender.

Life Insurance:

Information about insurance is provided on Lantern by SoFi Life Insurance Agency, LLC. Click here to view our licenses.

bernardbodo / istockphoto

DepositPhotos.com

Featured Image Credit: DepositPhotos.com.