The interest rate of a business loan can vary widely and will depend on the market, the type of loan, and the lender. On average, however, the annual percentage rate (APR) for a traditional bank loan starts around 6%. For alternative, online loans, the average APR can range anywhere from 6% to 99%.

The actual rate a lender will offer will also be based on your qualifications as a borrower, such as your personal and business credit score, annual revenue, debt-to-income ratio, cash flow, number of years in business, and whether or not you’re able to secure the loan with collateral.Here’s what you need to know about business loan interest rates and how to get the best loan at the lowest cost for your business.

5 Factors That Determine Business Loan Interest Rates

Below are some of the key factors that influence small business loan rates.

1. General Interest Rates

One of the biggest factors that affects what interest rate you’ll get on a small business loan is the current market rate. The current market rate is determined by the supply and demand in financial markets, central banks (such as the Federal Reserve), prevailing economic conditions, and inflation expectations.

The market rate is the same regardless of which lender you choose, your personal credit history, and the type of loan you receive.

2. Lenders

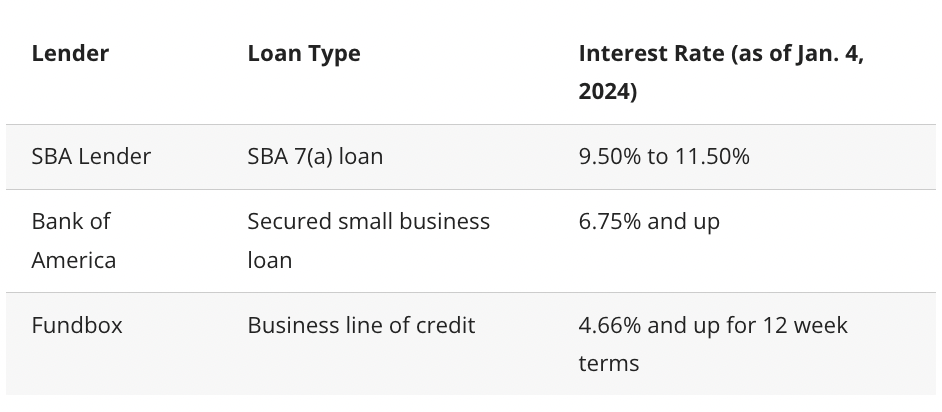

When you compare interest rates from different lenders, you’ll generally find that banks and SBA lenders typically offer some of the lowest rates. These loans can be difficult to qualify for, however, and the application and approval process can take several months to complete.

When comparing small business loans from different lenders, it’s helpful to look at the APR (if available) — this number includes not just the interest rate, but also the associated loan fees. This allows you to compare loan rates apples to apples.

To give you a snapshot of how interest rates can vary, here’s a sampling of lenders and the rates they’re currently offering as of January, 2024.

3. Types of Loans

There are many types of small business loans on the market, and each has their own interest rate range. Here’s a look at the historic average interest rates for common types of business loans:

Bank Small Business Loans

A traditional bank term loan can be more difficult to qualify for, but if you do, you’ll see they have some of the better interest rates on business loans — averaging 3% to 7%. Currently, though, rates start at 6.75% and go up from there due to market rates.

If you have strong credit, successful revenue, your business has been in operation for a few years, and you don’t need the funds right away, a traditional bank or credit union may provide you with the best terms.

Online Term Loans

The interest rates tend to run higher for online business loans — averaging in the neighborhood of 11% to 44%. However, it’s typically easier to qualify for this type of business loan than it is for bank term loans or SBA loans. As a result, online term loans can be a good option if your business has poor credit or hasn’t been in operation for very long. Online lenders also offer short-term loans that are not typically available from other sources.

SBA Loans

The Small Business Administration (SBA) guarantees SBA loans, which are offered by banks it partners with to help serve small businesses.

Like bank loans, SBA-backed loans come with attractive interest rates for business loans — historically in the range of 5.50% to 8%. Like bank loans, though, SBA loans can be difficult to qualify for. However, these loans come with some of the best repayment periods — some as long as 25 years.

Business Lines of Credit

With a business line of credit (LOC), a lender gives you access to a specific amount of cash, which you can draw from whenever you want and use to cover whatever business expenses you need. A line of credit can be a great option for small businesses facing frequent cash flow issues. It can also be a good thing to have in your back pocket in case of emergencies.

Advertised rates for lines of credit are almost always low, but your business’s characteristics will determine how much you’ll pay. Historically, the APR for a business LOC can start around 11%, but they can go much higher. Like a credit card, though, you only pay interest on what you use.

Invoice Factoring

Invoice factoring is a short-term financing method that allows businesses to sell unpaid customer invoices to an invoice factoring company. You can often get up to 85% of your unpaid invoices up front. The factoring company then collects payment from your customers and gives you the remaining balance — minus fees. While these fees can be hefty — in the range of 13% to 60% — invoice factoring can help a business get past difficult financial times.

Merchant Cash Advances

A merchant cash advance (MCA) allows your business to exchange your future earnings for immediate cash. With an MCA, you receive a lump sum of cash from an MCA provider, which you pay back using a percentage of your daily sales. MCAs are typically easier to qualify for than traditional business loans, but tend to come with higher costs. Instead of interest rates, MCAs come with factor rates — often around 1.20 to 1.50.

To determine the total cost of an MCA, you multiply the total amount of cash advanced to you by the factor rate. For example, If you get $20,000 and have a factor rate of 1.25, the total cost is $25,000 ($20,000 x 1.25), which includes the $20,000 advanced to you and $5,000 in fees.

4. The Business’s Finances

No matter what type of lender you work with or what type of loan you pursue, your business’s finances will likely be thoroughly studied by an underwriter when you apply for a small business loan.

Here are some things lenders typically will look at when considering whether or not to give you a loan and, if so, at what rate.

Credit Scores: Personal and Business

Each lender has its own criteria for establishing interest rates, but personal and business credit scores are usually one of the main determining factors.

If your business is new and doesn’t have a strong credit history, lenders will likely look at your personal credit profile. Generally, a higher score will help you get a lower interest rate. Lenders often require a minimum personal credit score to qualify for financing. Banks may look for scores of 680 or higher, while online lenders may accept scores in the 500s.

Lenders will also look at your business’s credit score. Instead of ranging from 300 to 850, business credit scores range from 1 to 100, as follows:

- Good: 80-100

- Fair: 50-79

- Bad: 0-49

If you have a “good” credit score, this means that you are making your payments on time and possibly in advance. If this is the case, you can expect to receive some of the best rates.

Business Income

How much money you bring in year to year can be a key factor in determining whether you will get approved for a loan, how big of a business loan you can get, and what the interest rate will be.

A business with a strong, predictable revenue stream has a good chance of getting approved for a high loan amount with a low interest rate. If you’re just starting out and your monthly revenue is still picking up steam, you may have trouble taking out certain types of business loans.

Time in Business

The amount of time you’ve been in business also impacts the interest rate a lender will offer you. If your business is new, you will likely pay more in interest, even if your cash flow is better than more established companies. The magic number many banks want to see is often two years. It’s not uncommon for a new business to fail shortly after they’ve opened, so the fact that you’re still standing after two years is a good sign to a lender.

Quantity of Collateral

Lenders often require borrowers to put up a fixed asset (like property or equipment) to secure a loan. This reduces risk for the lender because if you default on the loan, they can seize your collateral and sell it to make up for some of the money they’ve lost.

If you’re applying for an SBA loan or bank loan, for example, lenders will want to know what kind of collateral your small business has to offer and the value of that collateral. It’s possible to get a loan without collateral, but these loans, called unsecured loans, typically come with higher interest rates.

5. Industry

Some businesses are statistically more likely to fail than others. For example, first-year failure rates tend to be higher for companies in food service, finance/insurance, real estate, and professional/technical services.

If your business is considered a risky business to lend to, you may receive a higher rate. In addition, some lenders have certain industries that they won’t lend to (such as firearms businesses) that could affect their reputation.

Fixed vs. Variable Interest Rates

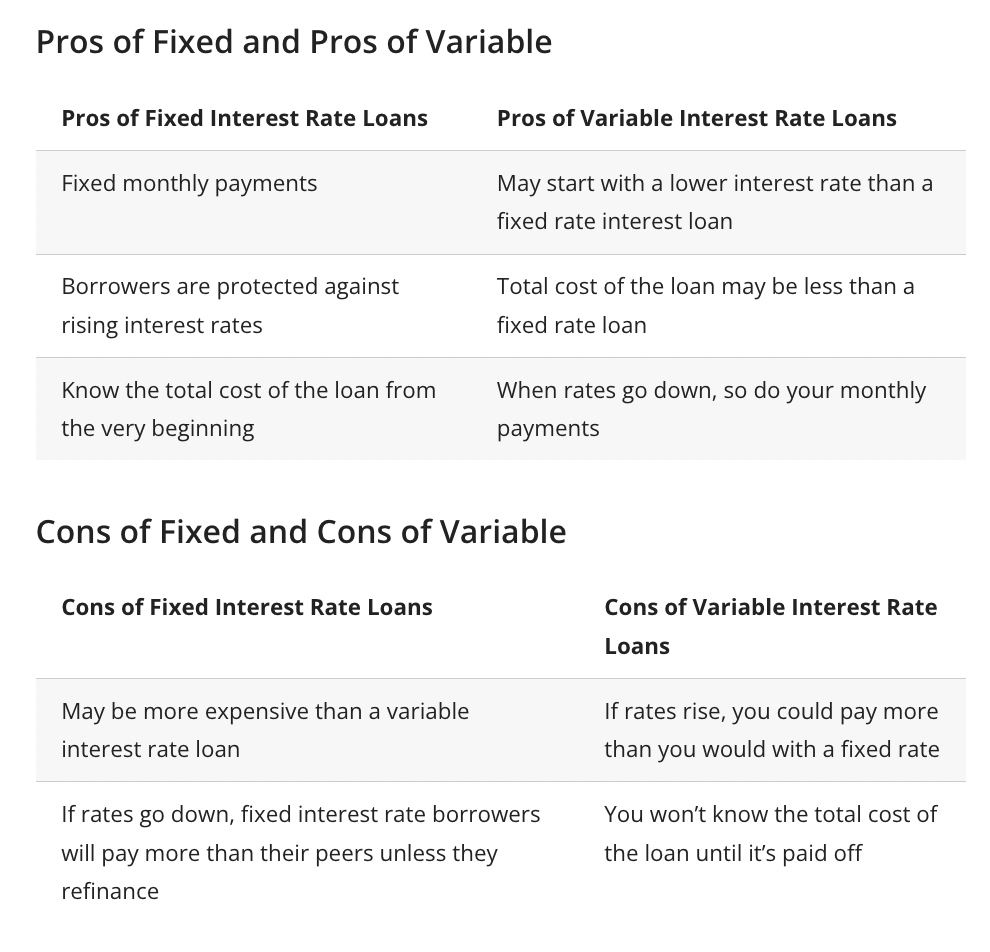

When looking at loans, you may have a choice of getting a fixed or variable interest rate. A fixed interest rate loan has the same interest rate and monthly payment for the life of the loan. This means your first payment will be the same amount as your last payment.

Businesses often choose loans with fixed interest rates so they can easily budget for the payments. In addition, if interest rates are currently low, a fixed interest loan is a way to lock in that rate for the duration of the loan.

A variable interest rate loan may have different payments from one month to the next. If the market fluctuates, the rate you pay could go up or down over the life of the loan. Variable-rate loans tend to have lower rates than fixed loans at the outset. For a short-term loan, a variable interest rate can end up being a good deal for the borrower. But there is some risk involved, as the rate can increase and you need to be prepared to make that higher monthly payment.

How To Compare Business Loan Rates

When comparing small business loans, you’ll want to look at more than just the interest rate. In fact, when lenders advertise only a monthly interest rate, it can be deceiving.

A monthly interest rate is simply how much interest you would be charged in one month. It doesn’t include any other charges associated with the loan, which may include one-time charges like origination and application fees, or recurring fees like a monthly service charge.

To better understand how much money you’ll actually be required to pay over the lifetime of your loan, and to make sure you’re comparing loans accurately, you’ll be better off comparing the annual percentage rate, or APR.

(Learn more: Personal Loan Calculator)

Business Loan Fees

Possible fees for business loans include:

- Application fee

- Processing fee

- Closing fee

- Origination fee

- Prepayment fee

- Late payment fee

- Monthly service fee

How To Calculate Total Business Loan Cost

The easiest way to figure out the total cost of taking out a small business loan is to use one of the many loan calculators available online. In order to use one of these tools, you’ll need a few pieces of information, including:

- The loan amount

- The annual interest rate

- Other fees associated with the loan (origination fees, closing costs, etc.)

- The loan term

From there, you can see what the total cost of the loan would be, including your monthly payment.

The Takeaway

The average small business loan interest rate depends on the overall market rate, the type of loan, the lender, your business’s financials, and the industry your business is in. Overall, SBA and traditional bank loans tend to offer better rates than other loan products. However, they may not be the best fit for your business if it’s new, doesn’t yet have a strong or well-established credit profile, or needs financing relatively quickly.

This article originally appeared on SoFi.com and was syndicated by MediaFeed.org.

Lantern By

SoFiSoFi receives compensation in the event you obtain a loan, financial product, or service through the Lantern marketplace. This Lantern website is owned by SoFi Lending Corp., a lender licensed by the Department of Financial Protection and Innovation under the California Financing Law, license number 6054612; NMLS number 1121636. (www.nmlsconsumeraccess.org). This site is NOT owned and operated by SoFi Bank. Loans, financial products, and services may not be available in all states.

All rates, fees, and terms are presented without guarantee and are subject to change pursuant to each provider’s discretion. There is no guarantee you will be approved or qualify for the advertised rates, fees, or terms presented. The actual terms you may receive depends on the things like benefits requested, your credit score, usage, history and other factors.

*Check your rate: To check the rates and terms you may qualify for, Lantern and/or its network lenders conducts a soft credit pull that will not affect your credit score. However, if you choose a product and continue your application, the lender(s) you choose will request your full credit report from one or more consumer reporting agencies, which is considered a hard credit pull and may affect your credit.

All loan terms, including interest rate, and Annual Percentage Rate (APR), and monthly payments shown on this website are from lenders and are estimates based upon the limited information you provided and are for information purposes only. Estimated APR includes all applicable fees as required under the Truth in Lending Act. The actual loan terms you receive, including APR, will depend on the lender you select, their underwriting criteria, and your personal financial factors. The loan terms and rates presented are provided by the lenders and not by SoFi Lending Corp. or Lantern. Please review each lender’s Terms and Conditions for additional details.

Many factors affect your credit scores and the interest rates you may receive. SoFi is not a Credit Repair Organization as defined under federal or state law, including the Credit Repair Organizations Act. SoFi does not provide “credit repair” services or advice or assistance regarding “rebuilding” or “improving” your credit record, credit history, or credit rating. For details, see the FTC’s website on credit (consumer.ftc.gov)

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.¹

SoFi’s Insights tool offers users the ability to connect both SoFi accounts and external accounts using Plaid, Inc.’s service. When you use the service to connect an account, you authorize SoFi to obtain account information from any external accounts as set forth in SoFi’s Terms of Use. SoFi assumes no responsibility for the timeliness, accuracy, deletion, non-delivery or failure to store any user data, loss of user data, communications, or personalization settings. You shall confirm the accuracy of Plaid data through sources independent of SoFi. The credit score provided to you is a VantageScore® based on TransUnion® (the “Processing Agent”) data.

Personal Loan

SoFi Lending Corp. (“SoFi”) operates this Personal Loan product in cooperation with Engine by MoneyLion. If you submit a loan inquiry, SoFi will deliver your information to Engine by MoneyLion, and Engine by MoneyLion will deliver to its network of lenders/partners to review to determine if you are eligible for pre-qualified or pre-approved offers. The lenders/partners receiving your information will also obtain your credit information from a credit reporting agency. If you meet one or more lender’s and/or partner’s conditions for eligibility, pre-qualified and pre-approved offers from one or more lenders/partners will be presented to you here on the Lantern website. More information about Engine by MoneyLion, the process, and its lenders/partners is described on the loan inquiry form you will reach by visiting our Personal Loans page as well as our Student Loan Refinance page. Click to learn more about Engine’s Licenses and Disclosures, Terms of Service, and Privacy Policy.Personal loan offers provided to customers on Lantern do not exceed 35.99% APR. An example of total amount paid on a personal loan of $10,000 for a term of 36 months at a rate of 10% would be equivalent to $11,616.12 over the 36 month life of the loan.

Student Loan RefinanceSoFi Lending Corp. (“SoFi”) operates this Student Loan Refinance product in cooperation with Engine by MoneyLion. If you submit a loan inquiry, SoFi will deliver your information to Engine by MoneyLion, and Engine by MoneyLion will deliver to its network of lenders/partners to review to determine if you are eligible for pre-qualified or pre-approved offers. The lenders receiving your information will also obtain your credit information from a credit reporting agency. If you meet one or more lender’s and/or partner’s conditions for eligibility, pre-qualified and pre-approved offers from one or more lenders/partners will be presented to you here on the Lantern website. More information about Engine by MoneyLion, the process, and its lenders/partners is described on the loan inquiry form you will reach by visiting our Personal Loans page as well as our Student Loan Refinance page. Click to learn more about Engine’s Licenses and Disclosures, Terms of Service, and Privacy Policy.

NOTICE: The debt ceiling legislation passed on June 2, 2023, codifies into law that federal student loan borrowers will be reentering repayment. The US Department of Education or your student loan servicer, or lender if you have FFEL loans, will notify you directly when your payments will resume For more information, please go to https://docs.house.gov/billsthisweek/20230529/BILLS-118hrPIH-fiscalresponsibility.pdf https://studentaid.gov/announcements-events/covid-19

If you are a federal student loan borrower considering refinancing, you should take into account the new income-driven payment plan, SAVE, which replaces REPAYE, seeks to make monthly payments more affordable, and offers forgiveness of balances that were originally $12,000 or lower after 120 payments, among other improvements. Also, please note that once you refinance federal student loans you will no longer be eligible for current or future flexible payment options available to federal loan borrowers, including but not limited to income-based repayment plans, such as SAVE, or extended repayment plans.

Auto Loan RefinanceAutomobile refinancing loan information presented on this Lantern website is from Caribou, AUTOPAY, Engine by MoneyLion, and each of Engine’s partners (along with their affiliated companies). Caribou, AUTOPAY, and Engine by MoneyLion pay SoFi compensation for marketing their products and services on the Lantern site.

Auto loan refinance information presented on this Lantern site is indicative and subject to you fulfilling the lender’s requirements, including but not limited to: credit standards, loan size, vehicle condition, and odometer reading. Loan rates and terms as presented on this Lantern site are subject to change when you reach the lender and may depend on your creditworthiness, consult with the lender for more details. Additional terms and conditions may apply and all terms may vary by your state of residence.

Secured Lending DisclosureTerms, conditions, state restrictions, and minimum loan amounts apply. Before you apply for a secured loan, we encourage you to carefully consider whether this loan type is the right choice for you. If you can’t make your payments on a secured personal loan, you could end up losing the assets you provided for collateral. Not all applicants will qualify for larger loan amounts or most favorable loan terms. Loan approval and actual loan terms depend on the ability to meet underwriting requirements (including, but not limited to, a responsible credit history, sufficient income after monthly expenses, and availability of collateral) that will vary by lender.

BankingSoFi Lending Corp. (“SoFi”) operates this website in cooperation with Engine by MoneyLion presenting promotions for products and services offered by other banks, lenders, and financial institutions. If you select a promotion above, you will be connected to the website of the company offering the product. The promotions presented on this site are from companies that pay SoFi and Engine by MoneyLion compensation for marketing their products and services. This may affect whether a provider is featured on this site and could affect the order of presentation. Lantern and Engine by MoneyLion do not include all providers in the market or all of their available offerings. Click to learn more about Engine’s Licenses and Disclosures, Terms of Service, and Privacy Policy.

More from MediaFeed:

The average American debt by age

You may hear this term being batted around in conversations surrounding billionaires, but in reality, everyone has a net worth. It’s simply a total of all your assets minus any debts you have.

Those assets can include cash, real estate, intellectual property, and other items like jewelry, stocks, insurance policies, and bonds. The cash may come from a job you have or from unearned income, such as your Social Security payment

Having a lot of assets does not necessarily mean you have a high net worth, particularly if you also carry a lot of debt. For example, you may have a million-dollar mansion, but if you have debts of $500,000, your net worth dwindles rapidly.

Jinda Noipho/istockphoto

There are many personal net worth calculators available online, though you don’t need one to calculate your net worth. Just take the total amount of all your assets and subtract the total amount of your liabilities:

Assets – liabilities = net worth

Some calculators will also factor in future growth so you can understand what your net worth will be in the future, as the value of your assets grows.

(Learn more: Personal Loan Calculator)

SARINYAPINNGAM/istockphoto

As you can see, it’s fairly easy to calculate your net worth, though it may take time to gather the values of all your assets, such as the current value of a piece of high-end jewelry. But once you do, you can add up all your assets and then subtract your liabilities to calculate your net worth.

wutwhanfoto/istockphoto

Knowing your own net worth is one thing, but where does it stand against other people in your age bracket? Generally, people see an increase in their net worth the older they get, and it can be helpful to use a net worth percentile calculator by age to see your percentile rank.

For example, if your net worth was $100,000, you would be in the 46.92 percentile for people between the ages of 18 to 100. The median net worth for this age bracket is $121,760.

Here’s the average net worth by different age groups, according to the most recent data available from the Federal Reserve.

PeopleImages/istockphoto

Average Net Worth: $112, 104

svetikd/istockphoto

Average Net Worth: $120,183

PeopleImages/istockphoto

Average Net Worth: $258,075

PeopleImages/istockphoto

Average Net Worth: $501,295

Drazen Zigic/istockphoto

Average Net Worth: $590,710

PonyWang/istockphoto

Average Net Worth: $781,936

Solovyova/istockphoto

Average Net Worth: $1,132,497

monkeybusinessimages/istockphoto

Average Net Worth: $1,441,987

PeopleImages/istockphoto

Average Net Worth: $1,675,294

kate_sept2004/istockphoto

Average Net Worth: $1,836,884

Jacob Wackerhausen/istockphoto

Average Net Worth: $1,714,085

nortonrsx/istockphoto

Average Net Worth: $1,629,275

jacoblund/istockphoto

Average Net Worth: $1,611,984

PeopleImages/istockphoto

Calculating your net worth is smart because it can help you understand where you’re strong financially (maybe you have little debt) and where you’re weak (maybe you’ve overextended your credit to buy your home).

It may also help you make plans for the future. For example, if your net worth is high, you might explore strategies for reducing taxable income, such as contributing more to a tax-deductible retirement account. And if your net worth isn’t where you’d like it, you can take steps to improve it.

Diversity Studio/istockphoto

If you’ve used a liquid net worth calculator, or compared your net worth to the table above and don’t feel like your numbers are as high as you’d like them to be, you can do a few things to increase your net worth.

If your debt levels are high, you can increase your net worth by decreasing that debt. Get a plan for paying off credit cards, student loans, car loans, and home mortgages. Consider increasing the amount you pay on each slightly to shorten your repayment period and decrease the amount of interest you pay on these loans and credit cards.

Creating a budget is one way to keep tabs on your finances as you’re paying off debt. A money tracker app can help make the job easier.

If you don’t have an abnormally high amount of debt but want to increase your assets, you might explore making more money. If you’re still in the workforce and have the ability to make a career change, you might consider cultivating potential high-income skills that could help you command a higher salary.

If you’re retired, you could take on part-time flexible work.

Evheniia Vasylenko/istockphoto

Not that you need to compare yourself to celebrities when it comes to net worth, but it can be fun to see how the other half lives. Keep in mind that while A-list celebrities often command millions of dollars for their work, they’re usually also smart with their money. They don’t typically blow their money on sports cars and mansions (though certainly some do). Many are financially responsible, investing in multiple income streams and spending responsibly.

Let’s look at the net worth of a few celebrities.

Reese Witherspoon

Reese Witherspoon didn’t limit her career to acting. She also founded a lifestyle brand called Draper James and a media brand called Hello Sunshine. Today her net worth is about $300 million.

J.K. Rowling

The well-known author of the Harry Potter books has an estimated net worth of $1 billion, and she’s the first author in history to reach this height. Before she was published, however, she struggled financially, which makes hers a true rags-to-riches story.

Jay-Z and Beyoncé

Superstar artists Jay-Z and Beyoncé reign supreme when it comes to net worth. Thanks to touring, albums, clothing lines, movies, endorsements, merchandise, and more, the couple’s combined net worth is $3 billion.

You may not be able to match the likes of Jay-Z and Beyoncé when it comes to net worth, but knowing yours can help you make smart financial decisions for the future. To figure out your net worth, you can subtract the total amount of your liabilities from the total amount of your assets. You can also use a personal net worth calculator; some will even factor in future growth.

This article originally appeared on SoFi.comand was syndicated byMediaFeed.org.

SoFi Relay offers users the ability to connect both SoFi accounts and external accounts using Plaid, Inc.’s service. When you use the service to connect an account, you authorize SoFi to obtain account information from any external accounts as set forth in SoFi’s Terms of Use. Based on your consent SoFi will also automatically provide some financial data received from the credit bureau for your visibility, without the need of you connecting additional accounts. SoFi assumes no responsibility for the timeliness, accuracy, deletion, non-delivery or failure to store any user data, loss of user data, communications, or personalization settings. You shall confirm the accuracy of Plaid data through sources independent of SoFi. The credit score is a VantageScore® based on TransUnion® (the “Processing Agent”) data.

*Terms and conditions apply. (Must click on the link to be eligible.) This offer is only available to new SoFi users without existing SoFi accounts. It is non-transferable. One offer per person. To receive the Rewards points offer, you must successfully complete setting up Credit Score Monitoring. Rewards points may only be redeemed into SoFi accounts such as cash in SoFi Checking and Savings, SoFi credit cards or loan balances, and fractional shares subject to program terms that may be found here: SoFi Member Rewards Terms and Conditions. PDF File. SoFi reserves the right to modify or discontinue this offer at any time without notice.

Third-Party Brand Mentions: No brands, products, or companies mentioned are affiliated with SoFi, nor do they endorse or sponsor this article. Third-party trademarks referenced herein are property of their respective owners.

Non affiliation: SoFi isn’t affiliated with any of the companies highlighted in this article.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

jacoblund/istockphoto

bernie_photo/istockphoto

Featured Image Credit: ijeab/istockphoto.